|

5.2.5 Monetary Policy

a) Objectives

The central bank is a relatively new institution.

For those interested in its hstory, please see

Observation #6: A

Brief History of the Central Bank - UK, USA & Canada. Today the primary objective of every central bank is

preservation of the value of the currency – internally with respect to

domestic inflation and externally with respect to the exchange rate.

Secondary objectives include acting as the government’s banker and debt

manager (particularly internationally), moderating the business cycle as

well as fostering economic growth and full employment.

The primary objective goes to the heart of economic

expectations. The expected price level is the basis of aggregate

expenditure including consumption, investment, government and

export/import decisions. The uncertainty created by inflation

affects the present value of future 'real' earnings, i.e., how

much one is willing to pay today for a future stream of earnings

tomorrow. Change the expectation and a different outcome

will be reached. If prices rise or fall too fast choices must be

hastily re-calculated. Uncertainty increases and uncertainty is the

great and costly enemy of investment.

Rising prices also affect asset values and

hence wealth with a corresponding 'wealth effect'. In a capitalist society or plutocracy wealth is the

measure of one’s worth. Wealth owners – large and small - have a vested

interest in price stability and the value of their assets. The central

bank serves their interests. In a sense, the Central Bank is a

fourth order of government beyond the executive, legislative and

judicial. It represents an institutional marriage of the political

and financial worlds in a capitalist society. The Great Depression

taught that the animal spirits of the investment community could not be

trusted to operate in society's best interest; long history had already

taught that letting the State control the printing press leads to

similarly bad outcomes. A balance was struck: the modern Central

Bank, a post-Great Depression institution.

The logic of control goes like this: by manipulating the

money supply the Central Bank changes interest rates; by changing

interest rates the central bank can control investment; by controlling

investment the central bank can manipulate aggregate demand; and,

thereby, the central bank controls the aggregate price level, i.e.,

inflation. Similarly, control of interest rates allows the Bank to

raise or lower the exchange rate to encourage or discourage foreign

investment. Discretionary change in monetary policy suffers from

policy lag - is there an emerging problem - recession/inflation?

Recognition then requires decision-making - what tools should we use?

Having the tools in hand how long will it take to nudge the system to a

low inflation, full employment AD/AS equilibrium?

Control of interest rates, of course, allows the

Central Bank to achieve both its primary objective of stabilizing the

value of the currency and, in some jurisdictions, secondary objectives including moderating

the business cycle and fostering economic growth and full

employment.

b) Tools

The question arises: How does the central bank manipulate

the money supply and thereby interest rates and thereby investment and

thereby aggregate demand? It uses five principal tools.

i - Required Reserve Ratio (C10/230-33:

215-18; 224-225;

206-207)

First, there are reserve

ratio requirements. By law or moral suasion chartered banks and other

deposit taking institutions may be required to increase or decrease a

percentage of their deposits held in reserve in case of a ‘run’,

i.e., many if not all depositors asking for their money back at the

same time. If the reserve ratio is 10% then 90% of deposits may be

loaned to earn interest and thereby increase the money supply, i.e.,

banks make money by making money. If the ratio is lowered more loans

are made, interest rates fall and investment increases, etc. If

the ratio is raised loans are called in (so-called demand loans first)

and the money supply shrinks, interest rates go up and investment falls,

etc.

This describes the situation at the retail level which

was the subject of post-Great Depression banking reforms. At the

wholesale level, however, the shadow banking system is not currently

subject to reserve requirements as such. Leverage of some investment

banks leading to the Great Recession was in some cases as high as

300:1. In effect reserve requirements act as tax on lending

institutions by imposing an opportunity cost measured by interest income

foregone on reserves. How reserve requirements may be applied to the

wholesale or shadow banking system in the post-Great Recession period

remains to be seen.

ii - Bank Rate and Banker’s Deposit Rate (229;

211)

Second, like all businesses

deposit taking institutions experience short-run cash flow problems.

The central bank acts as “the banker’s bank”. When an institution

borrows from the central bank the rate is the ‘bank rate’. As lender

the central bank can charge more or less than last time indicating the

direction it wishes interest rates to go and thereby add or subtract

from reserves of lending institutions. In Canada, the Bank of

Canada also uses the 'over night' rate to commercial banks for short

term borrowing.

The central bank also holds deposits by chartered banks

and other lending institutions on which it pays interest. Again it can

raise or lower that rate signally its policy. The rate paid is “the

banker’s deposit rate”.

iii - Open Market Operations

(C10/237-38: 222-23;

230-232; 212-214)

Third, there is an array of

government securities that can be bought and sold on financial markets

as income earning assets, e.g., Treasury Bills and Canada Savings

Bonds. By varying their rates, terms and conditions deposit taking

institutions are encouraged to buy or sell them thereby increasing or

decreasing reserves. The money supply increases or decreases, interest

rates move, investment changes, etc.

Treasury Bill auctions are a favoured instrument.

Usually 90 days in duration they are backed by the sovereign power of

the State. Treasury Bills are the safest investment and command no risk

premium. The central bank requests bids for a certain amount usually

offered to meet the government’s short-term cash flow needs. The

central bank then decides which bids to accept. If it wants rates to

rise it accepts higher bids; to fall, lower bids; if stable, the

existing market rate. If rates go up, investment goes down, etc.

and vice versa.

iv - Government Deposit Shifting

Fourth, the government

maintains deposit accounts with the Bank of Canada and other lending

institutions. These accounts are managed by the central bank. By

shuffling government accounts it can increase or decrease deposit taking

institutions’ reserves. The money supply expands or contracts; interest

rates fall or rise; investment grows or declines,

etc.

v - Moral Suasion

Just as animal spirits capture the emotional depths of

investment, moral suasion captures the emotive power of the central

banker. What and the way a chairman of the Federal Reserve, or Governor

of the Banks of Canada or England say or how they raise their eyebrows

in public is intensely studied. This is similar to back in the USSR

when photos of who stood next to whom on Lenin’s tomb during the May Day

parade became an academic career, a.k.a., the dark art of

Kremlinology.

Kenneth Boulding captured the mystery and magic of the

central bank when he wrote in his 1972 article “Towards

a Cultural Economics”:

I have argued for years that bankers were a savage tribe

who should be studied by the anthropologists rather than by the

economists, and I once tried to persuade Margaret Mead to do a book on

“Coming of Age in the Federal Reserve,” with, I regret to say, no

response at all! The culture of bankers, indeed, is more mysterious

than that of the Dobuans or the Chuk-Chuks. The Navaho indeed may have

a Harvard anthropologist in every family, but the Federal Reserve Board

has, to my knowledge, never allowed a single one to attend the

ceremonials in its marble hogan. Nobody really knows what bankers are

like, what kinds of images of the world they have, what they talk about,

what kind of gossip they follow, what taboos they have, and how their

decisions are made. The economics of money and banking is almost

entirely a matter of the analysis of published statistics and the

attempt to find correlations among them. It is pure “black box”

analysis with practically no attempt to pry off the lid to see what are

the actual processes which produce the often very peculiar outputs.

Arguably, moral suasion is the most efficient tool of the

central bank. At the top of the financial food chain, a simple nod or a

wink is usually sufficient to elicit an appropriate response from the

chartered banks and other financial intermediaries.

It is important to note that with deregulation of much of

the US banking system during the 1990s a new 'shadow banking' system

arose outside the direct control of the central bank. For those

interested, please see

Observation #7:

Shadow Banking & the Great Recession of 2008.

c) Interaction with Fiscal Policy

Before considering monetary policy’s application in

lowering unemployment or inflation respectively in a recessionary or

inflationary gap it is important to note that a central bank may pursue

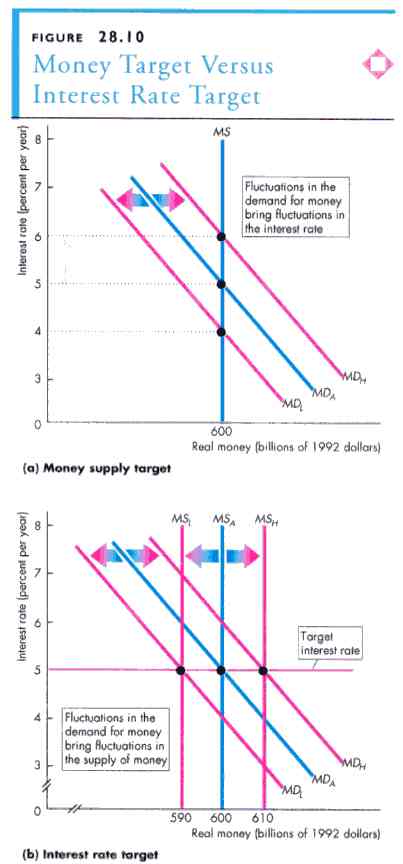

one of two alternative ‘target’ strategies. The first is a

money supply target

that remains fixed while the shifting demand for money curve increases

or decreases interest rates. Monetarist policy publicly promises to

increase the money supply only to match real growth in the

economy and thereby avoid price inflation. What happens to investment

is left to the market.

The second is an

interest rate target

that shifts the vertical inelastic money supply curve to match increases

in the demand for money in order to maintain a targeted interest rate.

This publicly announced strategy increases investment confidence.

While a secondary objective the central bank can use its

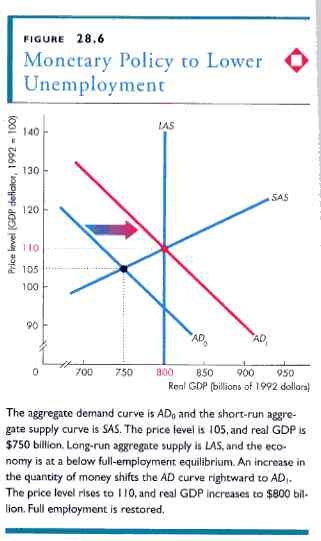

powers to increase employment and shift the economy

from a recessionary

gap into full employment. By

increasing the money supply it lowers interest rate. By lowering

interest rates it increases investment. By increasing investment it

shifts the aggregate demand curve up to the right into full employment

equilibrium between aggregate demand, short-run aggregate supply and

potential – the Keynesian Double Cross.

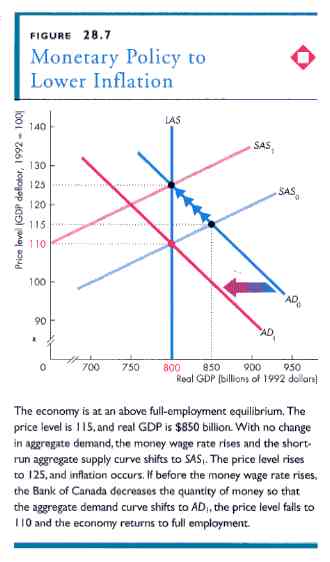

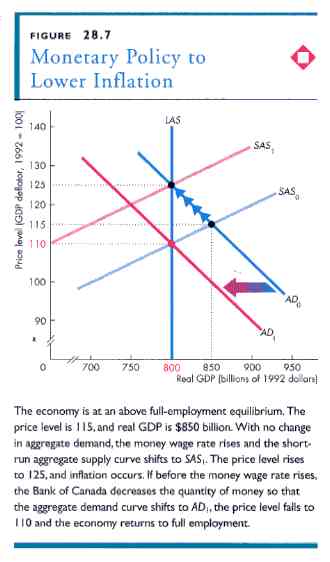

Fighting inflation and maintaining the value of the

currency is the primary objective of the central bank. When the economy

enters an inflationary gap market forces will eventually raise factor

prices and shift the short-run aggregate supply curve up to the left

until equilibrium between aggregate demand, short-run aggregate supply

and potential is achieved. This will, however, include a significant

increase in the aggregate price level, a.k.a., inflation. If,

however, the central bank

tightens the money

supply thereby raising interest rates

and decreasing investment before factor prices can increase then it can

shift the aggregate demand curve down to the left until equilibrium is

achieved at a lower price level.

5.2.6 AD-AS Model

4. Influencing Interest and Exchange Rates

a) Interest Rate (P&B

Fig

28.10; R&L 13th Ed

Fig. 28-3,

Fig. 29-1)

b) Exchange Rate

5. Ripple Effects of Monetary Policy

a) Interest Rate Fluctuations

b) Exchange Rate Fluctuations

6. Money in the AD-AS Model

a) Unemployment (P&B Fig.

28.6)

b) Inflation (P&B

Fig.

28.7)

c) Real GDP

4.2.8 Quantity Theory of Money

- GDP = PY

- V = PY/M

- MV = PY

- P = (V/Y)M

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}