|

1.

Opportunity Cost & Profit

(MKM

C13/277-8; 258-9;

282-284;

262-264)

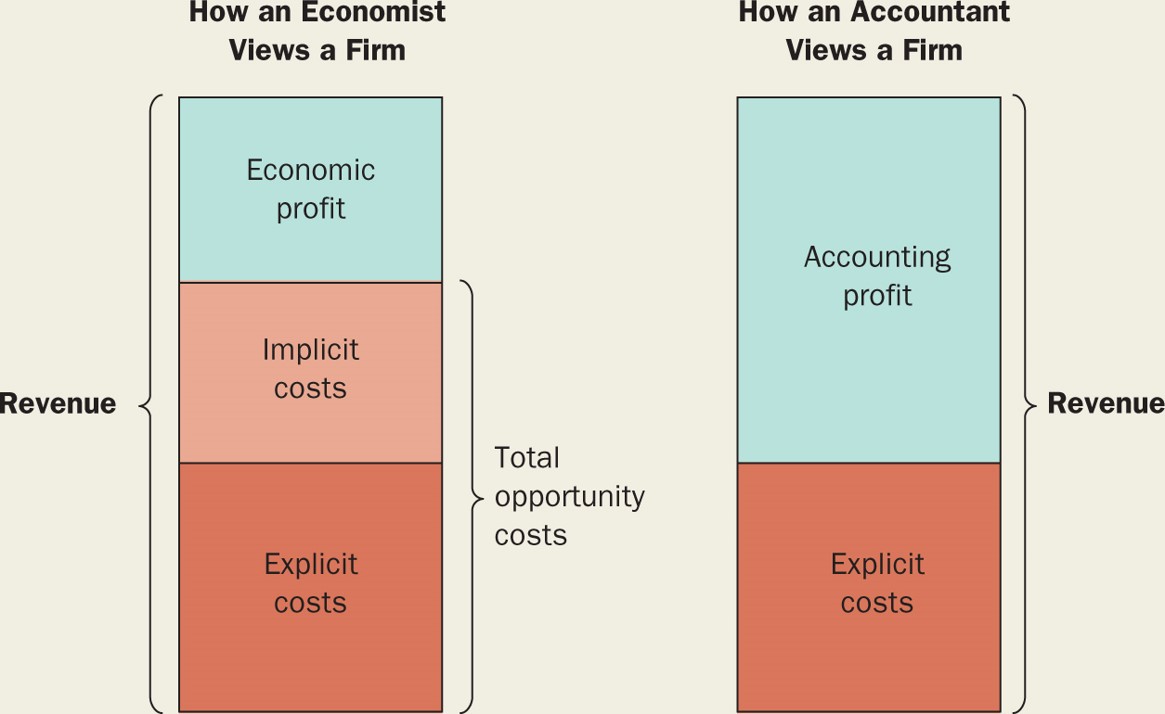

While for convenience one usually measures opportunity cost in dollars

it actually

involves real alternatives foregone. Thus for a firm, the opportunity cost of producing

(OCP) a good (and therefore opportunity

cost of employing factors of production) is the next best alternative action.

There are two components to a firm’s OCP : explicit and implicit costs.

Explicit costs are paid directly in money; implicit costs or opportunities foregone

are not paid directly in money (even though

measured that way).

Explicit costs include direct payment for factors of

production, e.g. in the case of labour,

money cost or wages are generally equal to their OC. Implicit costs include

the implicit cost of physical capital, inventories and the owner’s resources. (MKM Figure 13.1)

i - Capital

The first

form of implicit cost faced by a firm is the opportunity cost of its physical

capital. The OC of capital plant and equipment are usually implicit because

they are generally

bought outright, There are two forms of implicit costs

associated with physical capital: depreciation and interest:

a) economic depreciation is the change in market price of capital asset over a

given time period. Depreciation occurs for various reasons such as: older equipment has

shorter life than new equipment and requires

more maintenance. It is, however, important to distinguish between technical

and functional obsolescence. Equipment becomes technically obsolete when

newer equipment can do the job more efficiently, e.g. the Pentium CPU made the

486 and 386 technically obsolete. Functional obsolescence occurs when old

equipment can simply not do the job;

b) interest could have been earned on capital used to purchase

equipment. If a firm borrows money to buy it then it pays the explicit cost as interest on

the borrowed money but if uses its own cash it foregoes interest earned e.g. in bank deposit,

and becomes an implicit cost.

The combination of depreciation and interest constitutes the 'implicit rental

rate' of physical capital. All thing being equal, market forces should bring about

the equality of

implicit and explicit rental rates for given type of capital equipment

There are some costs, however, that are not treated as economic costs. For

example, sunk cost or past economic depreciation are not counted as an economic

cost. Once capital equipment has been bought any alternative opportunity

is foregone and cannot be retrieved except by selling. Similarly, once equipment has

been depreciated the cost is sunk and cannot be recovered.

It is important to realize that accounting measures of depreciation

differ from economic depreciation. In accounting one often uses

some form of straight line

depreciation, for example, over 20 yrs for buildings or 3 years for cars and

computers. In economics depreciation continues until there is no resale value and interest

to be earned as an opportunity cost no matter generally

accepted accounting principles (GAAP), i.e., 'vintage' equipment

with zero book value may be a productive asset especially if the cost of other

factors of production can be reduced, e.g., worker coop purchase of mills

and mines usually involve a drop in wages & salaries or Third World countries

with 'vintage' plant & equipment but low wage labour. This stage can be associated with

technical obsolescence, i.e., it can continue to do the job but is not at

minimum optimum scale and lowest cost per unit. All usefulness must be exhausted and

then the shell simply thrown away or sold as junk. This is the final stage

called functional obsolescence, i.e., it can no longer perform the job it

was designed to do.

ii -

Inventories

The

second type of implicit cost faced by a firm is the stock of raw materials, semi-finished goods and unsold finished goods,

i.e. inventories. The opportunity cost of inventories can be calculated in

a number of ways including estimating their current market price using the

'first-in-first out' (FIFO) or 'last-in-first out' (LIFO) methods.

iii - Owner’s Resources

The third

form of implicit cost faced by a firm is the opportunity cost of the owner's

resources. This includes the time and effort the owner could have made

employed elsewhere earning a wage or salary. The OC of entrepreneurship is

called ‘normal profit’.

2.

Efficiency:

General, Technical and Economic

In general, efficiency refers to the ratio of outputs to

inputs. To measure efficiency one must therefore be able to calculate

both inputs and outputs. This is most easily done in the production of

goods rather than services, especially in manufacturing, e.g.

cars produced per worker.

Technical efficiency is achieved when it is

not possible to increase output without increasing inputs. Economic efficiency occurs when the cost of production

for a given output is as low as possible. A secondary

consideration is that such output is sold at a price sufficient to

compensate all factors of production at their

normal rates, i.e., no excess or

economic profit or rents are earned. Thus all

economically efficient solutions are technically efficient but not all

technically efficient solutions are economically efficient, that is,

something may be technically possible but uneconomic. It can not pay

its own way, e.g., space exploration and the military.

3.

Why the Firm and not the Market?

The firm is an institution that hires factors of production to produce goods and

services.

Markets are also institutions that can coordinate economic decisions.

Why should some economic activities take place in the one or the other?

The answer is 'cost'.

Firms internalize economic activity because of a number of factors

including: transaction costs, economies or diseconomies of scale and economies of

team production (specialization).

i -

Transaction Costs

(MKM

C10/230; 215-6; 237;

218-219)

Transaction cost include: the costs of finding

someone with whom to do business; the costs of reaching agreement on exchange;

and, the costs of ensuring such agreements are fulfilled.

Markets require that buyers and sellers find each

other, get together and negotiate. They also usually require lawyers

to draw up contracts. Rather than buying a good or service on a market, firm can reduce

such cost by internalizing their production.

It is important to note, however, that while at any given point in time may be cheaper to buy on

a market rather than produce

within the firm (out-sourcing), at another point in time cost may change and it

becomes cheaper to internalize production of necessary factors of production.

ii - Economies & Diseconomies of Scale

(MKM

C13/289-91; 270-2; 296;

274-275)

Economies of scale exist when the

cost per unit output falls as output rises.

Economies of scale are due to specialization and division of

labour. A firm will tend to internalize an economic activity if its scale

of production allows it to enjoy such economies of scale.

On the other hand, diseconomies of scale occur

when

the cost per unit output increases as output rises. Diseconomies of scale

can occur as

a firm grows in size and complexity. Some things are more cheaply

done at a smaller scale of production, e.g. due to congestion. In

fact, some entire industries are based on 'small scale', e.g. creative products like art,

advertising and R&D. These activities are often more efficiently conducted in small rather than

large firms. In entertainment and advertising the same result can

sometimes be achieved by creating special small scale production units while the

main administration of the enterprise handles marketing and other activities

that benefits from economies of scale.

iii - Team Production

Another factor leading firms to internalize certain activities is specialization

in mutually supportive tasks or team production. Putting a designer

together with an engineer and other specialists within the firm may be

cheaper than trying to buy such services on the market and then try and

coordinate their various outputs.

iv -

Technological Change (MKM C4/78;

73;

75;

68)

In the Standard Model

technological change refers to the impact of new knowledge

on the production function of the firm. The nature of

that knowledge whether from the Natural & Engineering

Sciences (NES), Humanities & Social Sciences (HSS) or the

Arts is not identified only its mathematical impact.

Such new knowledge may be endogenous, i.e., a result of the

profit seeking activities of firms. Or it may be

exogneous, i.e., the result of the curiosity of

inventors and the search for knowledge-for-knowledge-sake,

i.e, pure research usually conducted in universities.

For those interested in a fuller description of

technological change please see

Observation #7: Technological Change.

|

{kind=link}