|

Industrial Organization

begins with Basic Conditions of Demand and Supply. Demand comes

from consumers (final and intermediary) while Supply is generated by

producers using factors of production and technology. Supply and

Demand are the two side of the economic equation.

Demand in economics refers

to the willingness of a consumer to pay a given price for a given

quantity of a good or service. This reflects the taste of the

consumer, i.e., one’s wants, needs and desires subject to a

budget constraint – income and prices – assuming the price of other

goods and services remain fixed.

Modern economics began with

Demand or consumer theory which was then extended to Supply or

producer theory and finally to their interaction in different types

of Markets. Or as the great American criminal entrepreneur Al

Capone said: If there is a Demand there will be a Supply! In this

section we will examine the Consumption/Utility Function of the

individual consumer. We will then derive the Income Consumption

Curve from which the Engels Curve (income demand curve) will be

derived. We will then derive the Price Consumption Curve from which

we will then derive the Demand Curve itself.

Utility Function

The standard model of market

economics rests on the philosophical base laid down by Jeremy

Bentham (1748 -1832). His was the last great philosophy of the

European Enlightenment (Schumpeter 1954). All is sensation; there

is no god. Human beings seek pleasure and avoid pain. Bentham, in

his felicitous calculus’ or the calculus of human happiness,

proposed a unit measure of pleasure and pain –the utile – the

sovereign ruler of the state. Utilitarianism is the generic term

but Bentham’s brand is ethical hedonism –ethical pursuit of

pleasure. It was in the 1870s that Bentham’s felicitous calculus

was married to Newton’s calculus of motion permitting erection of

the standard model of market economics.

Utility

This atom-like unit, the

utile, exhibits distinct characteristics. First, and for

Economics most important, the willingness of a person to pay a money

price for a good or service measures how many utiles of happiness

they expect to receive in exchange. This is reification –

making concrete (money) something that is abstract (happiness).

Furthermore, it is assumed that goods are infinitely divisible.

Second,

total utility is the satisfaction of consuming a total quantity of a

good or service.

Third,

marginal utility is the additional utility yielded by consuming one

more unit of that good or service.

Fourth,

diminishing utility means that at some level of consumption an

additional unit yields less satisfaction than the preceding unit,

i.e. total utility increases but eventually at a decreasing

rate. Furthermore, diminishing marginal utility eventually turns

negative becoming pain not pleasure, too much of a good thing;

Fifth,

diminishing marginal utility means a person does not consume just one

good. One does not live by bread alone. Assuming rationality, a

person chooses that combination of two or more goods and services

that maximizes total utility. This is calculatory rationality

meaning every choice is a calculation of the number and nature of

utiles, a.k.a., happiness or pleasure.

Furthermore, in theory, the

consumer is assumed rational, i.e., one chooses between

alternative commodity combinations to maximize utility assuming:

i - perfect knowledge, that

is, the consumer is aware of all alternative commodity combinations,

their prices and resulting utility;

ii - competence, that is, a

consumer is capable of evaluating the alternatives; and,

iii – taste of a consumer is

transitive or consistent, that is, if a consumer likes A as much as

B and B as much as C then one likes C as much as A.

It is also assumed that the

consumer is only able to order commodity combinations by level of

utility, 1st, 2nd, 3rd etc. This is called ordinal measurement or

rank ordering. Thus in consumption one does not specify the actual

numeric level or utility known as cardinal measurement.

Putting all these

definitions and assumptions together we generate the consumption

function as:

(1)

U = f (x, y) where:

U is the utility derived

from consuming combinations of x and y;

f

is the unique taste function

of a consumer;

U is continuous meaning

there are infinite combinations yielding the same level of utility.

Put another way, U is a dense set;

a number assigned to

commodity combinations such as U5 indicates only that it is

preferable to combinations with a lower number, e.g., U4 and

inferior to U6. In other words, we can rank order preferences but

any U# has no cardinal meaning; and,

U is defined for a specified

timeframe that is long enough to allow substitution between

commodity combinations but short enough to insure constancy of taste

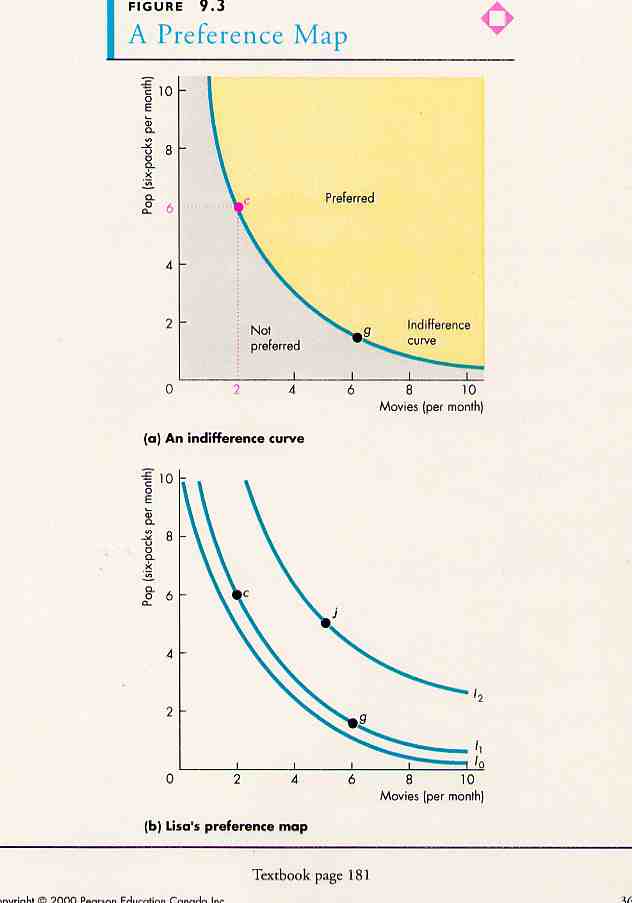

Indifference Curves

For any level of utility say

U’ = f (x, y) there is a locus of commodity combinations

which graphically form an indifference curve. All combinations on

that curve have the same level of utility meaning the consumer is

‘indifferent’ to any point on the curve. The indifference curve is

also called a preference or utility curve.

Usually an indifference

curve is ‘convex’ in shape reflecting that an increase in x can only

be obtained by a reduction in y, and vice versa

(B&P 4th Ed

Fig. 9.3; 5th ED Fig.

8.3;

7th Ed. Fig. 9.3; R&L

13th Ed Fig.

6A-1 &

A2).

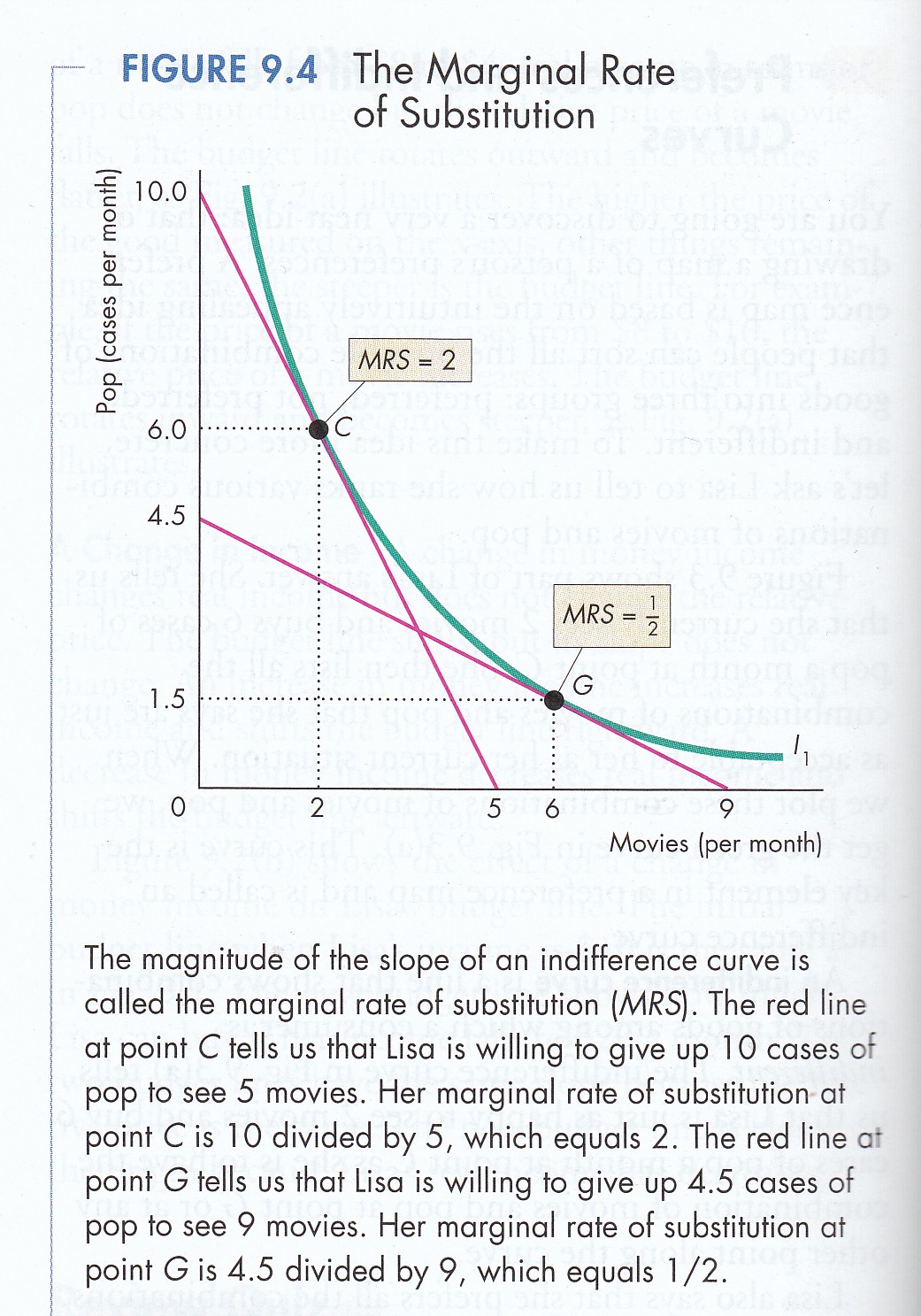

The amount of Y that must be given up to get more X while

maintaining the same level of utility is called the marginal rate

of substitution, i.e.,

(2)

MRS = MUy/MUx where:

MRS = marginal rate of

substitution

MUy = marginal utility of y

MUx = marginal utility of x

(P&B 4th Ed

Fig. 9.4; 5th Ed 8.4;

7th Ed Fig. 9.4; R&L

13th Ed Fig.

6A-1).

As noted above ‘f’ in

the equation U = f (x, y) is the taste function which is

different for each consumer. Thus each consumer will have a

uniquely shaped indifference curve and different MRS. When we plot

all possible levels of U we get a set of curves forming a consumer’s

indifference map. The transitivity assumption ensures the

curves do not intersect but rather rise higher and higher.

Budget Constraint

Before considering the

Budget Constraint it is appropriate to consider the nature of goods

purchased by a consumer and how they are able to pay their prices.

Commodities are called ‘goods’ because they satisfy human want,

needs and desires.

Goods

Goods can be classified in

different ways. First, there are complementary and

substitute goods. Complementary goods are one that are consumed

together, e.g., hamburgers and French fries or IPods and IPod

docking stations. Substitute goods are alternatives to one another,

e.g., a bicycle is a substitute for a car in transportation.

There are near and distant substitutes for most goods, e.g.,

a car or a truck are near substitutes while a car and a bicycle are

distant substitutes.

Second,

there are normal and inferior goods. A normal good is one the

consumption of which increases as income increases. An inferior

good is one the consumption of which decreases as income increases.

An example of an inferior good is cheap wine. As one’s income

increases consumption of cheap wine tends to decline.

Third,

there are conspicuous consumption or Veblen goods (named after

economist Thorstein Veblen) and normal consumption goods. Veblen

goods are rare and their consumption goes up as price goes up in

distinction from normal goods whose consumption goes down as price

goes up. Conspicuous consumption goods are bought to demonstrate to

others that one can afford such luxuries.

Prices

To buy a good a consumer must pay its price. Further to Bentham’s

assumption, the money price one is willing to pay for a good or

service equals the satisfaction or utility one believes can be

extracted from that good.

Income/Work

To pay a price, however, one must have income. Income is earned

through work which in the standard model is disutility, i.e.,

pain. One does not work for enjoyment (if one does one earns

‘psychic’ income) but rather for the monetary income used to buy

goods and thereby derived satisfaction.

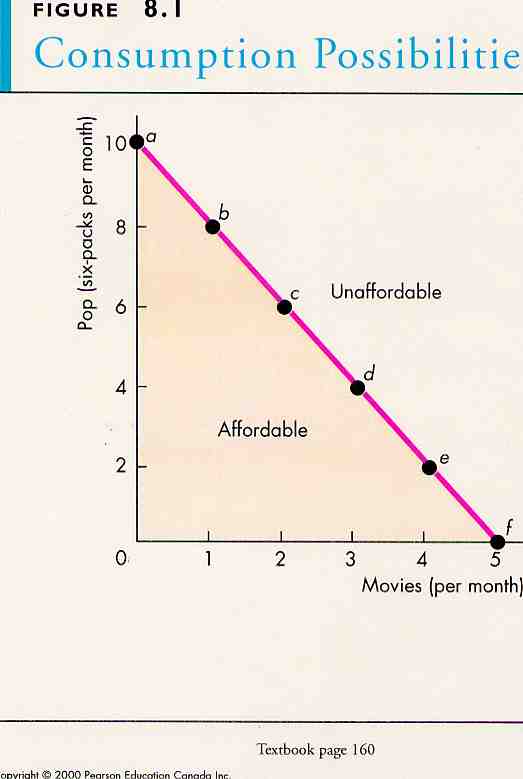

Constraint

While a consumer wants to

rise as high up the indifference map as possible, one is constrained

by income (I) and the price of x and y. Thus for a given level of

income and prices a budget line or constraint can be drawn. This

constraint shows all combinations that can be purchased that exhaust

income, i.e.,

(3)

I = PxX + PyY where:

I = income

P = prices

X & Y = goods

(P&B 4th Ed

Fig. 8.1 or 9.1; 5th

Ed Fig 7.1 or 8.1;

7th Ed Fig. 9.1; R&L

13th Ed

Fig. 6A-3).

One cannot consume above the

constraint and, in this model, it is irrational to consume below

(keeping cash on hand) because utility is derived only from

consuming goods & services.

The maximum amount of X or Y

one can afford (with a given income and prices) is shown by the

intercepts of the budget line and respective axes. The slope of the

budget line (rise over run) is the inverse of the price ratio,

i.e.,

(4)

Price Ratio = Px/Py

The slope itself is Py/Px

expressed as 1/(Px/Py). This formulation is a ‘convention’ or

tradition in economics. It represents the relative price of X and

Y, i.e., how many units of X can be bought with one unit of Y

at current prices, e.g., $2/$1= a relative price of 2.

If income varies while

prices remain fixed then a new higher budget line becomes available

to the consumer parallel to the original. In other words higher

income relaxes the constraint on one’s happiness. If, on the other

hand, the price of X (or Y) decreases the slope of the budget line

and therefore the price ratio changes. For

example if Px goes down then the intercept which measures

the maximum amount of x a consumer can afford increases even if income

remains constant.

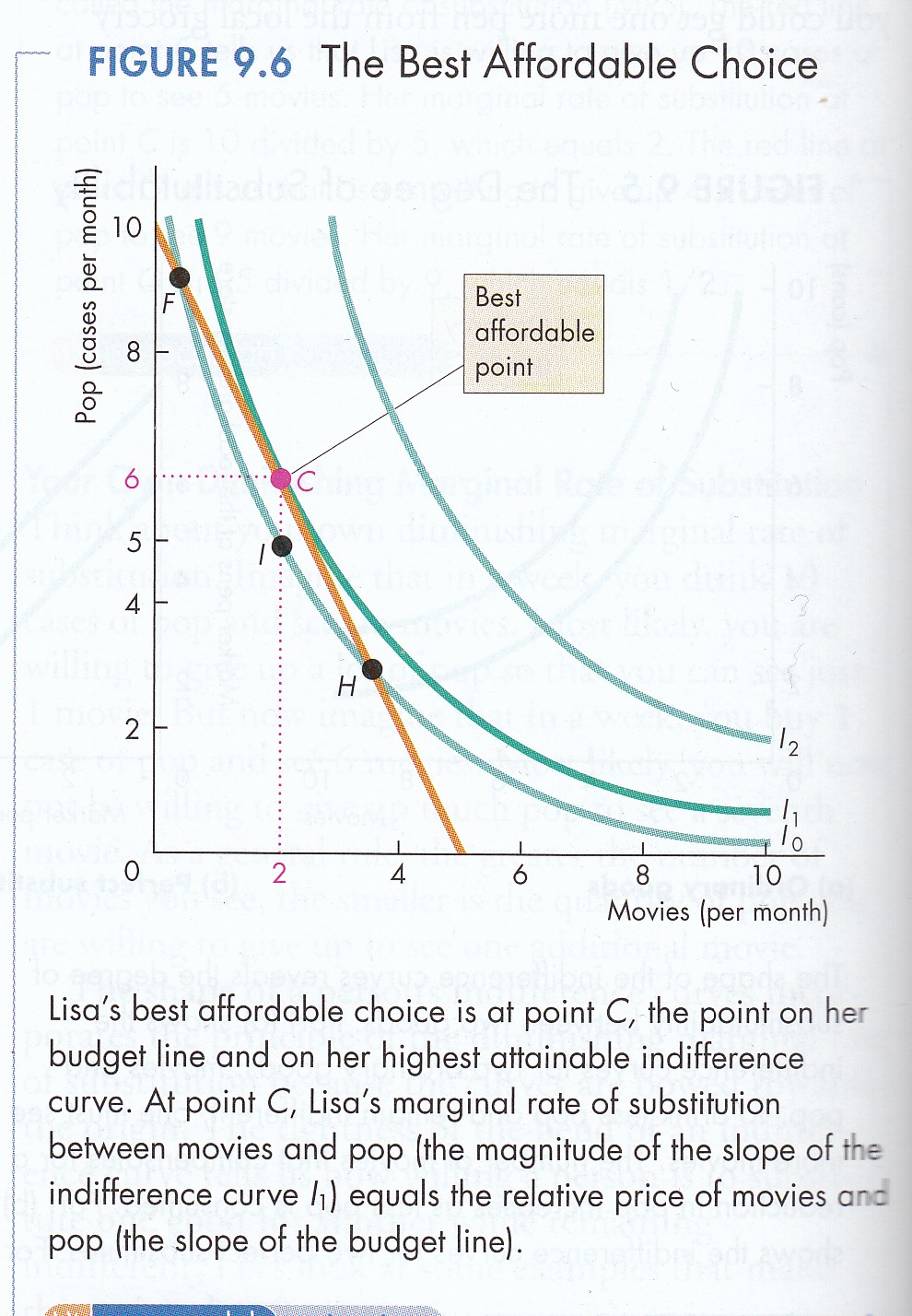

Equilibrium

The combination of x and y

that maximizes a consumer’s utility is the one on the budget line

tangent or just touching the highest attainable indifference curve

(P&B 4th

Fig. 9.4; 5th 8.4;

7th Ed Fig. 9.4; R&L

13th Ed Fig.

6A-1).

This is the ‘best affordable point’ (P&B

4th

Fig. 9.6; 5th 8.6;

7th Ed Fig. 9.6; R&L

13th Ed

Fig. 6A-4)

and satisfies the following conditions:

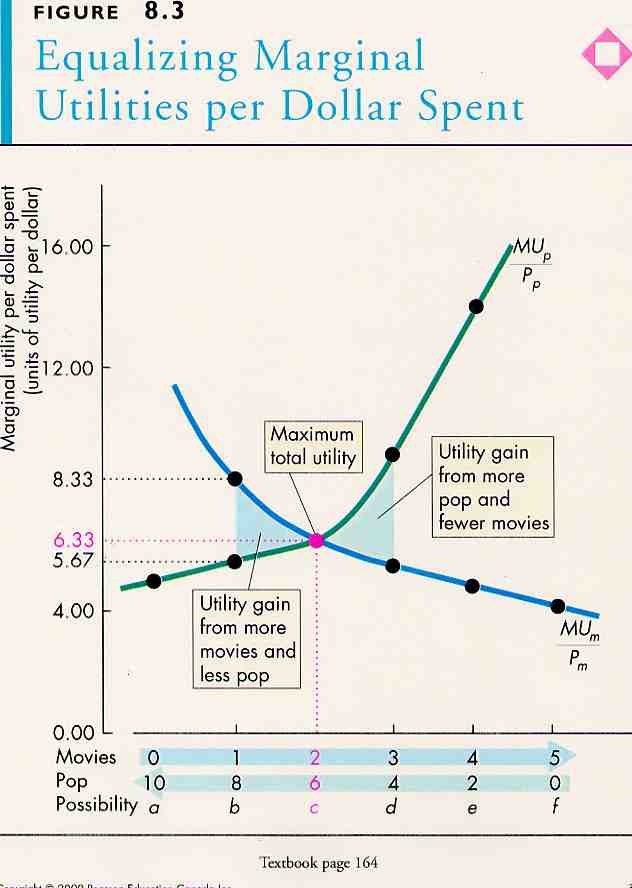

(5)

MRS = MUy/MUx = 1/(Px/Py)

that is the slope of the

indifference curve or Marginal Rate of Substitution equals the slope

of the Budget Line or the inverse of the price ratio (Px/Py) and at

this point the ‘rationale’ consumer equates the MU per dollar of

each commodity consumed or

(6)

MUx/Px = MUy/Py where

dollar-for dollar the

additional utility from an additional unit of X is equal

dollar-for-dollar to the additional satisfaction from one more unit

of Y (P&B 4th

Fig. 8.3; 5th Fig.

7.3; 7th Ed not displayed; R&L 13th Ed not displayed).

Consumers will remain at

this point, i.e., be in equilibrium, as long as taste, income

and prices remain fixed. This is the initial equilibrium. It is a

condition which once achieved continues indefinitely unless one of

the variables is altered (P&B 4th Ed

Fig. 4.8; 7th Ed

Fig. 3.7; R&L 13th Ed

not displayed).

For our purposes there are two types:

a) stable equilibrium: which

refers to a condition which once achieved continues indefinitely

unless there is a change in some underlying conditions. Changes in

economic conditions will be followed by reestablishment of the

original equilibrium. Example: a ball resting at the bottom of a

cup; shake it and the ball moves; stop shaking and it returns to the

bottom of the cup; and,

b) unstable equilibrium:

which refers to a condition which once achieved will continue

indefinitely unless one of the variables changes but the system will

not return to the original equilibrium. Example: a ball resting on

the top of an overturned cup - shake it and the ball falls off never

to return to the same place.

We will now change

assumptions one by one and see what happens to equilibrium.

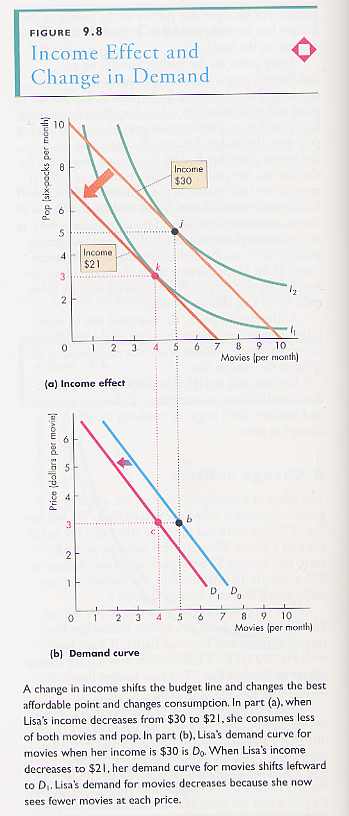

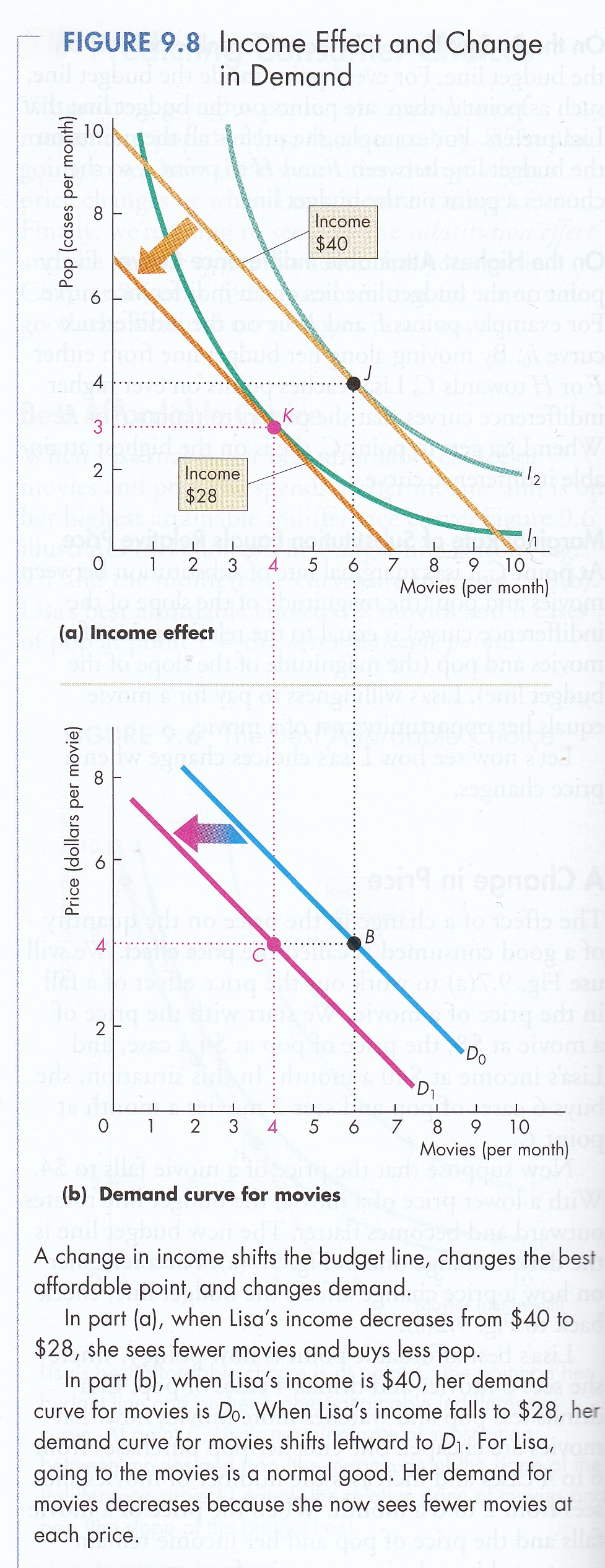

Income Consumption/Engels

Curves

An increase in income shifts

the intercepts of the budget line but leaves its slope constant -

assuming constant prices. The locus of tangents of budget lines

with indifference curves forms the income-consumption curve,

i.e., the set of commodity combinations (x, y) consumed as

income increases - assuming constant prices and taste

(R&L 13th Ed

Fig 6A-5).

From the income-consumption

curve we can derive the amount of a given commodity (x) purchased at

different levels of income. This forms the

Engel Curve

(M&Y

Fig. 4.2; R&L 13th Ed not displayed)

which, in effect, is the

income demand curve for a good or service. The shape of the curve

depends on the type of commodity. A normal good will have a

positively sloped Engel Curve reflecting the fact that as income

rises, consumption rises. An inferior good will have a negatively

sloped Engel Curve reflecting that as income increases consumption

decreases. An example is Kraft Dinner. For a poor student it is a

cheap source of pasta and cheese but when the student becomes a

well-paid junior executive of a Fortune 500 company it is no longer

preferred.

In business it is critical

to know if one’s product is a normal or inferior good. If consumer

income rises then sales of a normal good will increase. In a

recession, however, with falling consumer income sales of a normal

good decrease while sales of an inferior good increase.

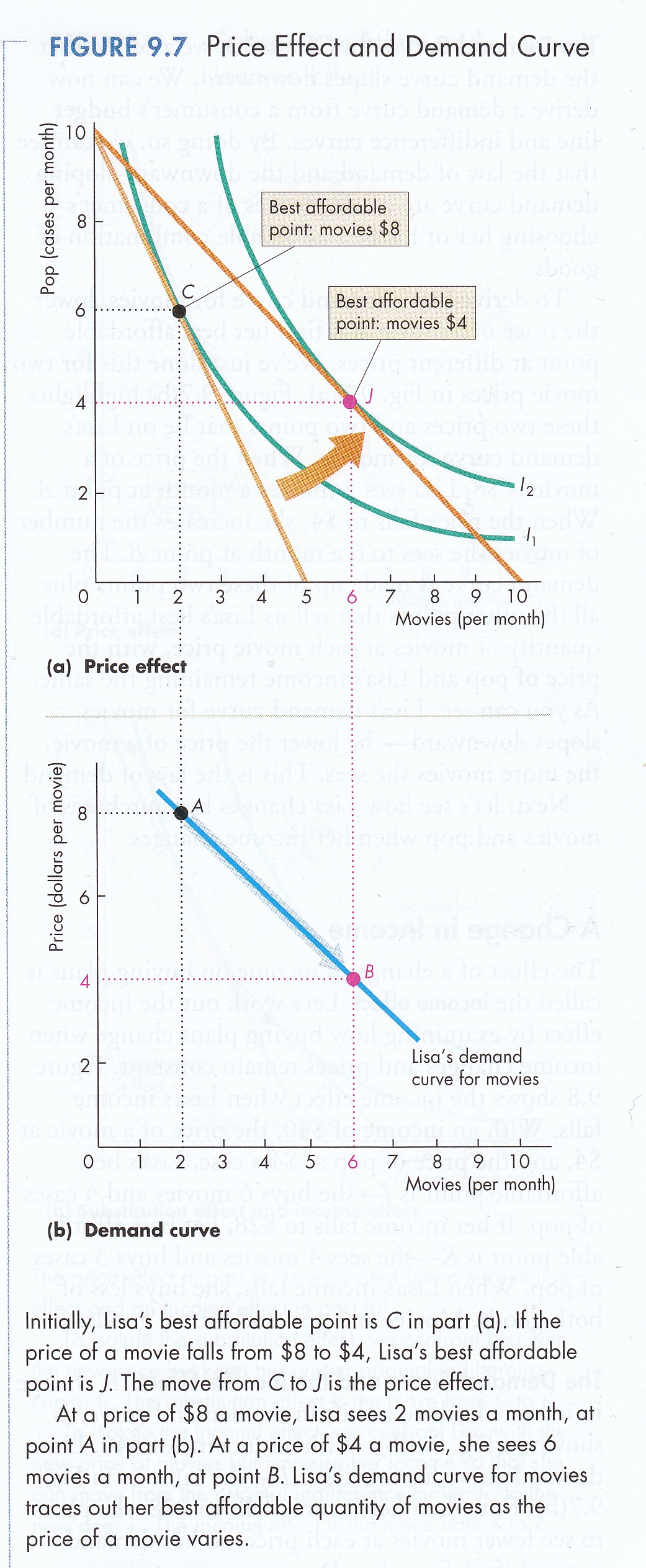

Price Consumption/Demand

Curve

If the price of one

commodity (X) changes a new set of combinations (X, Y) is created

between the changing tangents of the budget line and indifference

curves forming the price-consumption curve for the commodity. The

price-consumption curve shows how much of both commodities are

purchased if its price changes - assuming constant income and prices

for all other goods (R&L 13th Ed

Fig 6A-6).

The demand curve for a

commodity (X) can be derived from the price-consumption curve

showing how much of that commodity is purchased at different prices

- assuming constant income and constant prices for the other good

(Y). The shape of the demand curve (X) depends on taste, income and

the type of commodity - assuming constant prices for the other good

(Y) (P&B 4th Ed.

Fig. 9.7; 5th Ed.

Fig. 8.7;

7th Ed Fig. 9.7; R&L

13th Ed

Fig 6A-7).

The Law of Demand generally holds: the higher the price, lower the

demand; lower the price, higher the Demand. Why? The Law of

Diminishing Marginal Utility.

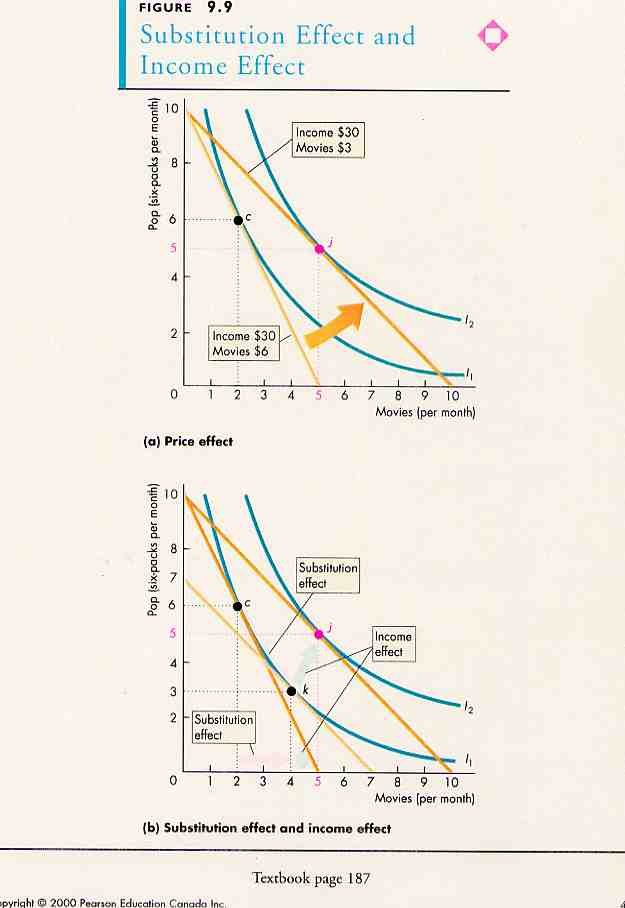

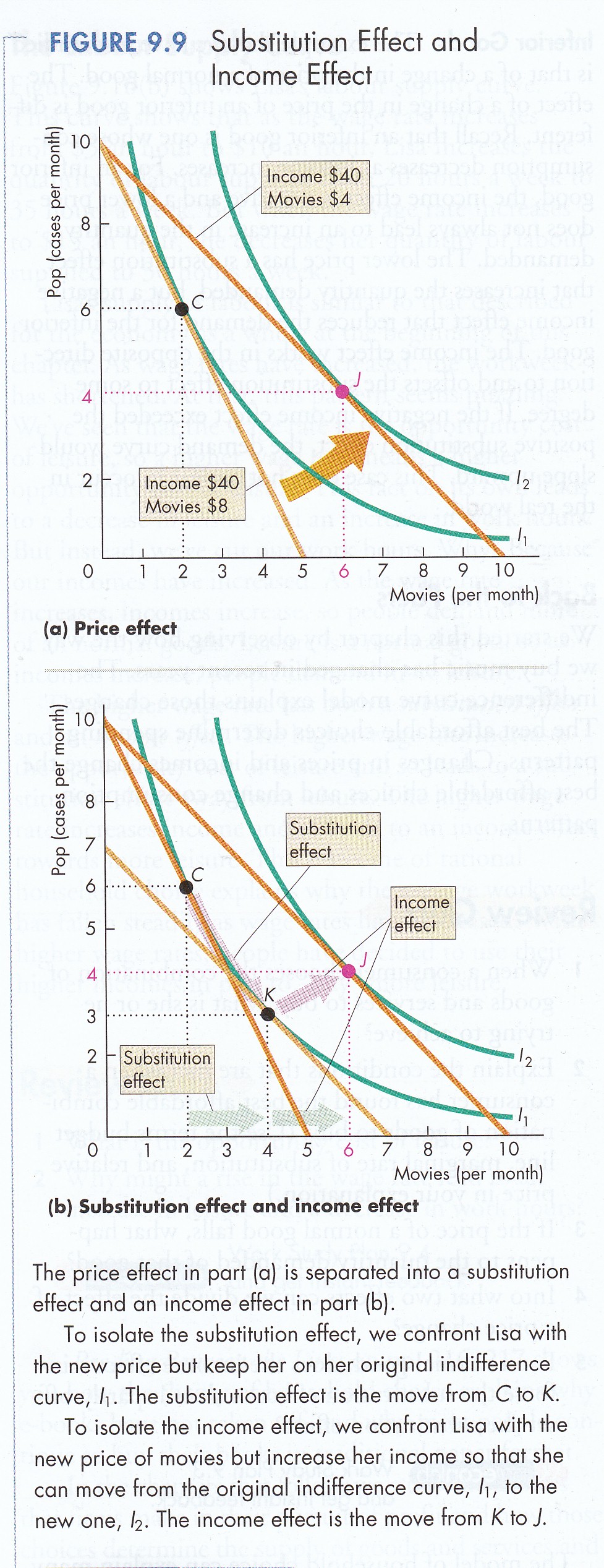

It is important to note that

the change in price of one good or service (assuming income and

prices of other goods remain fixed) has two effects. For example,

as the price of one good (X) declines it becomes cheaper relative to

Y. In equilibrium we have seen that consumers equates the marginal

utility per dollar of each good, i.e., MUx/Px = MUy/Py. If

the price of X goes down while the price of Y remains constant then

dollar for dollar the consumer can get more utility by substituting

x for the now more expensive y. This is called the substitution

effect. This effect holds for both normal and inferior goods.

In addition, if the price of

x goes down the consumer can now afford to buy the same amount but

have money income left over. In effect income goes up allowing the

purchase of more of both X and Y. This is called the income

effect.

The substitution effect is always negative, that

is if the price of a commodity (X) goes up, the quantity consumed

goes down. The income effect can be positive or negative. For

'normal' goods, an increase in income results in an increase in

consumption. If the quantity decreases when income increases the

commodity is an 'inferior' good. In most cases, if the price of an

inferior good decreases consumption will still increase if income

rises.

Taken together the

substitution and income effects are called the price effect

(P&B 4th Ed.

Fig. 9.8 &

Fig. 9.9; 5th Ed.

Fig. 8.8 & 8.9;

7th Ed Fig. 9.8 &

Fig. 9.9; R&L 13th Ed

Fig 6A-5;

M&Y 4.6 &

4.7).

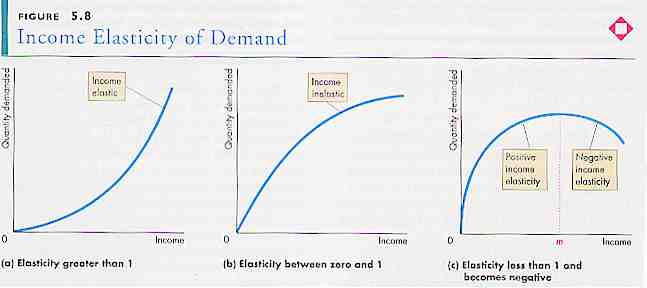

Elasticity

Elasticity refers to the

sensitivity of one variable to a one percentage change in another.

Economic theory recognizes three principal types:

a)

income elasticity of demand

with prices constant refers to the percentage change in the quantity

of a commodity demanded compared to a one percent change in income.

If income goes up 1% what happens to demand? If it too goes up 1%

there is unitary elasticity. If demand goes up more than 1% there

is elastic demand; if it goes up less than 1% then there is

inelastic income demand for the good or service (P&B 4th Ed, Fig

5.8; 7th Ed not displayed; R&L 13th Ed not displayed);

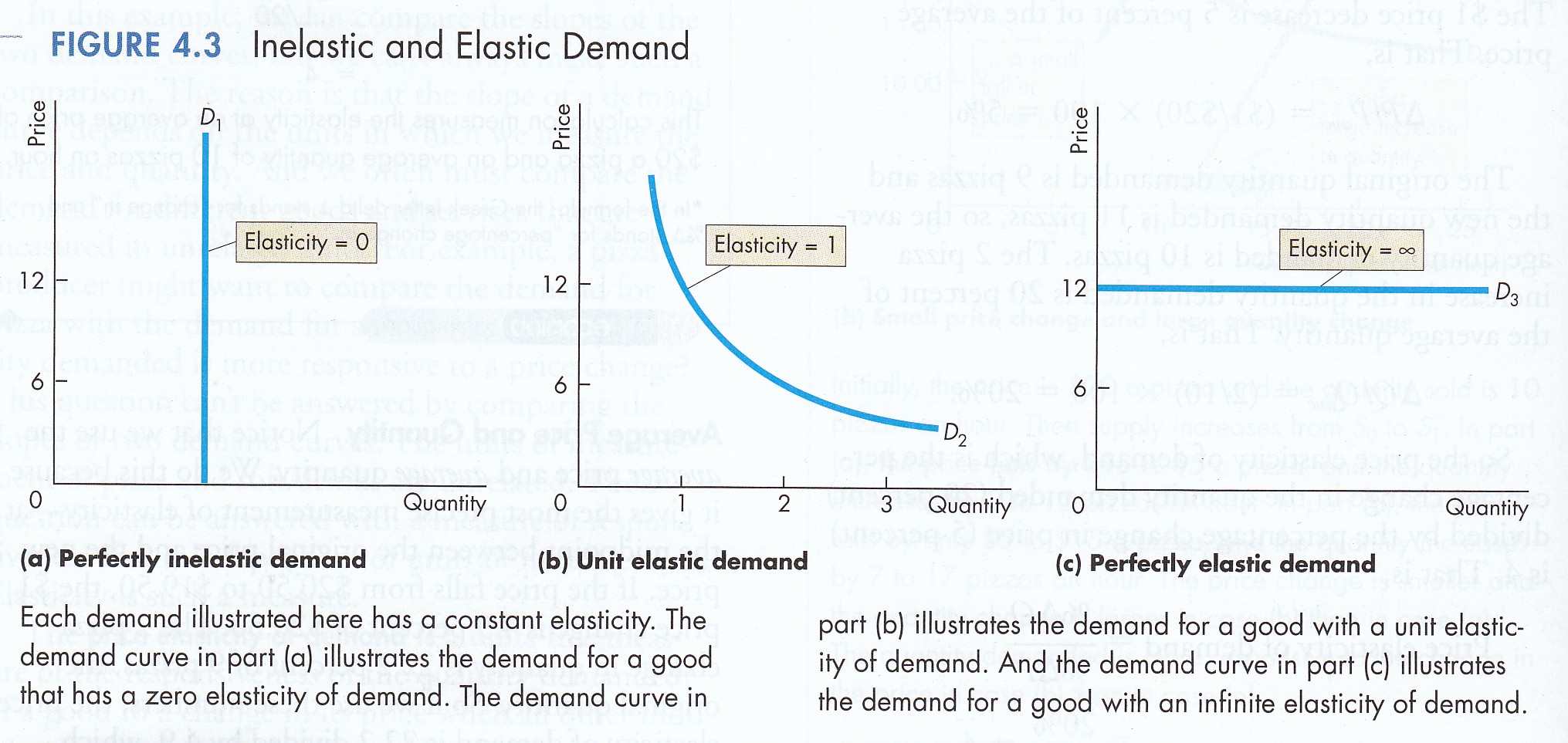

b) price elasticity of

demand

refers to the percentage

change in the quantity of a commodity demanded compared to a one

percentage change in its price. The amount demanded can increase:

i) more than

proportionately, i.e. elasticity is greater than one - at the

extreme a horizontal demand or supply curve is perfectly elastic - a

small increase in price results in a large change in the quantity

demanded or supplied;

ii) proportionately, i.e.

elasticity is equal to one (unitary elasticity); or,

iii less than

proportionately. i.e. elasticity is less than one (inelastic)

- at the extreme, a vertical demand or supply curve is perfectly

inelastic - any change in price results in no change in the amount

of the commodity demanded or supplied (P&B 4th Ed.

Fig. 5.8; 7th Ed

Fig 4.3;

R&L 13th ED.

Fig. 4-2

&

4-3);

and,

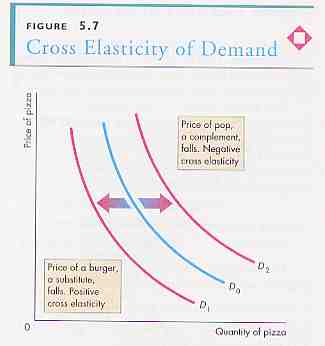

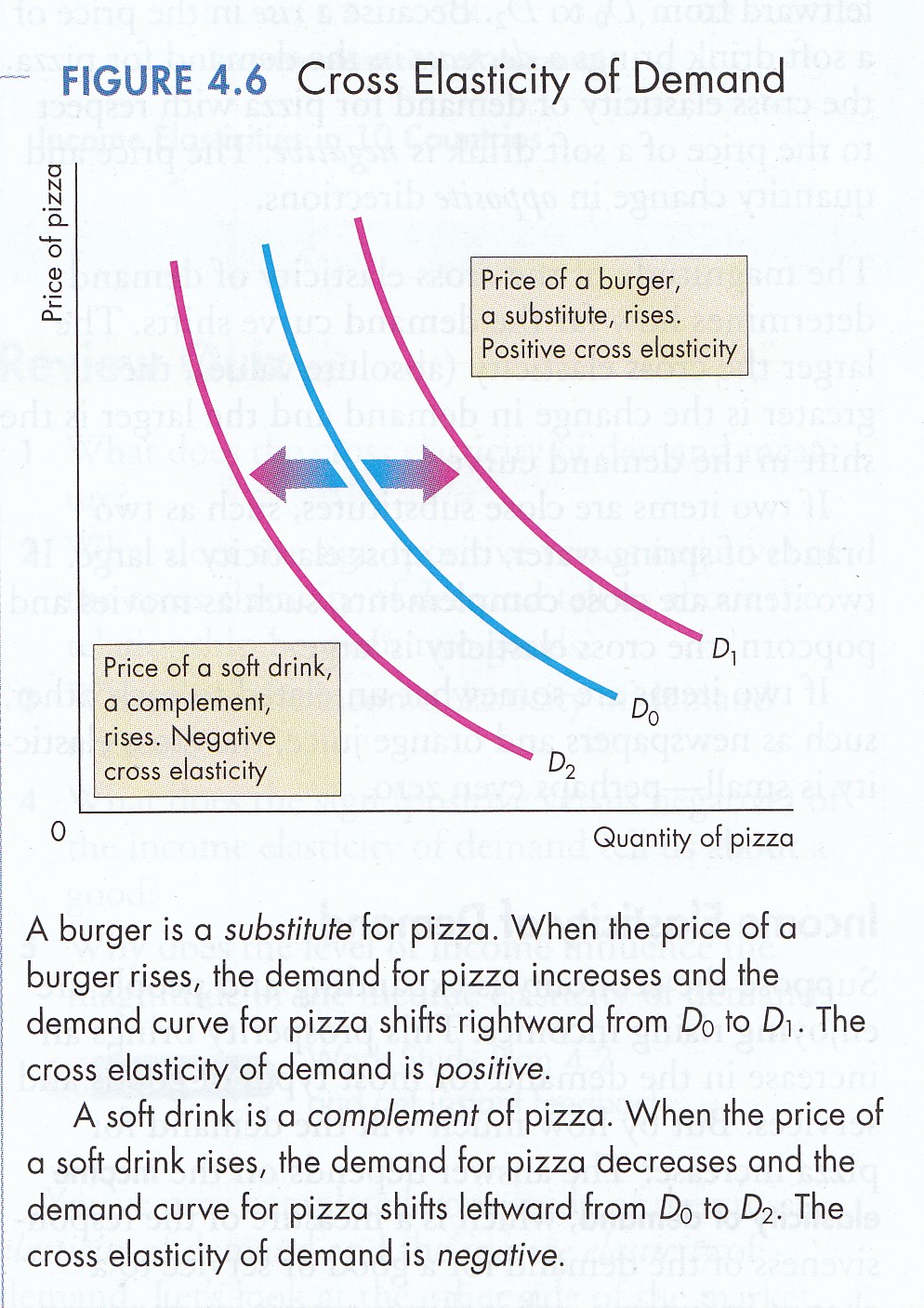

c) elasticity of

substitution or

cross-elasticity

in the consumption of one commodity substituted for another by a

consumer in response to a change in their relative prices (P&B 4th

Ed

Fig. 5.7; 7th Ed

Fig. 4.6;

R&L 13th Ed not displayed).

In conclusion, consumption

is the use of a product whereby utility is destroyed. Put another

way it is ‘negative production’. Producers put utility into a good

or service to satisfy human wants, needs and desires then consumers

extract it. Income is payment for work used to buy goods and

services to obtain utility. Work is the physical or intellectual

effort made to earn income to purchase products and thereby obtain

utility. Price is the dollar and cents cost of a product which is

assumed to represent the utility a consumer can derive from it.

Symbolic Summary of Demand

(1)

U = f (x, y)

Utility Function

(2)

MRS = MUy/MUx

Marginal Rate of Substitution

(3)

I = PxX + PyY

Budget Constraint

(4)

Px/Py

Price Ratio

(5)

MRS = MUy/MUx

= 1/(Px/Py) Consumer Equilibrium

(6)

MUx/Px = MUy/Py

Equilibrium Condition |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}