|

1.

Equilibrium

(MKM C7/160-2;

149-51;

156-161;

142-146)

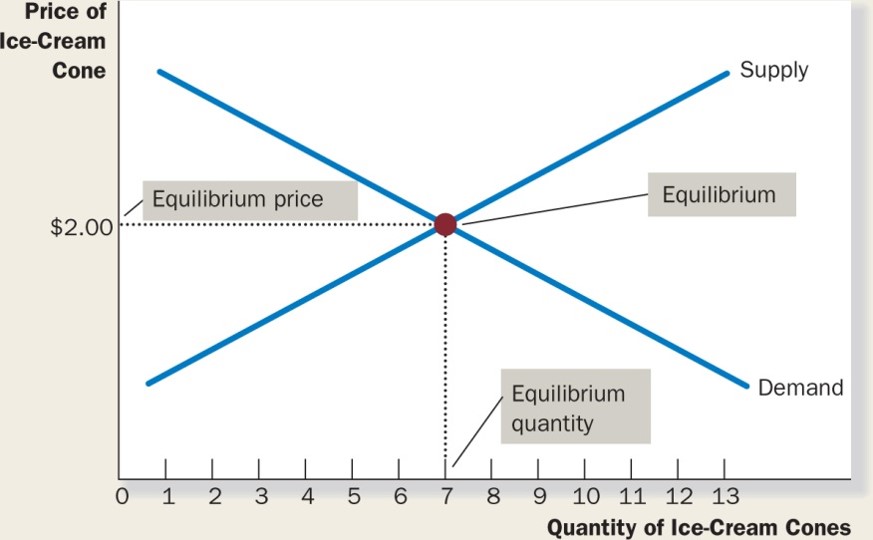

Equilibrium is a condition which once achieved will

continue indefinitely unless one of the variables is

altered (PB

7th Ed Fig. 3.7;

MKM

Fig. 4.8). In the case of

markets, the equilibrium price 'clears' the market, that is the quantity

demanded by consumers equals the quantity supplied by producers. More generally, economic theory recognizes

four general types

of equilibrium:

i -

general equilibrium: a condition that

exists in an entire economy given perfect competition in all industries.

It is a static state where all

prices are at their lowest long run average cost per unit, individuals spend

maximizing their satisfaction, demand for and supply of factors of production

(Capital, Labour, Natural Resources) is also in equilibrium with all factors

earning their opportunity cost;

ii

- stable equilibrium:

a condition once achieved continues indefinitely

with changes

in a variable followed by reestablishment of the equilibrium. Example: ball resting at the bottom of a cup; shake it,

stop and the ball

returns to the bottom;

iii

- unstable equilibrium:

a condition once achieved continues indefinitely with changes

in a variable not followed by reestablishment of the equilibrium.

Example: ball resting on the top of an overturned cup - shake it and the ball

falls off never to return; and,

iv - multiple equilibria: a condition that exists in an entire

economy with several points of stable equilibria but only one being

optimal with respect to growth of the economy.

For purposes of

this course only (ii) stable equilibrium will be examined.

2.

Elasticity

(MKM C5/98-118;

90-110;

98-117;

87-105)

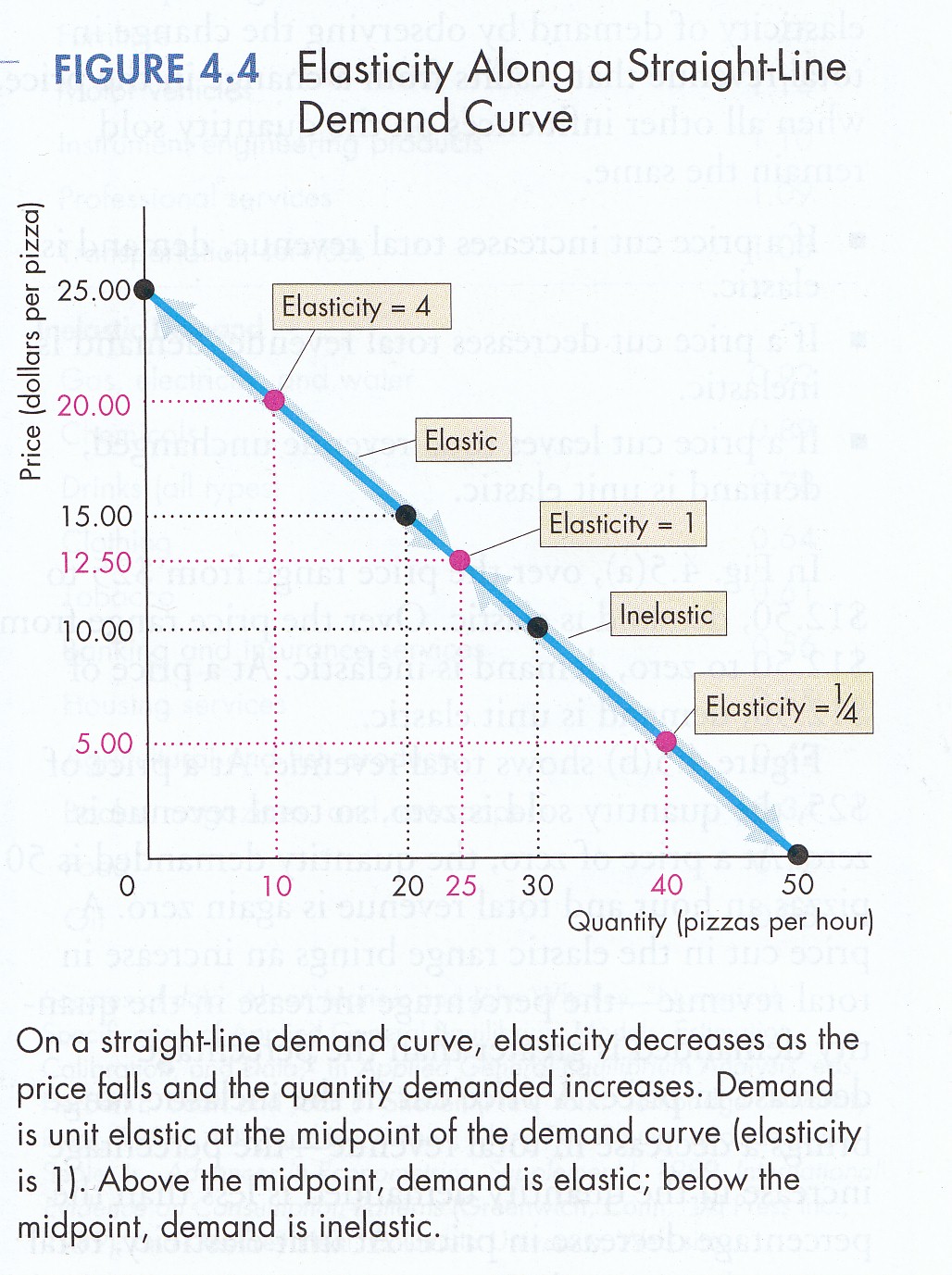

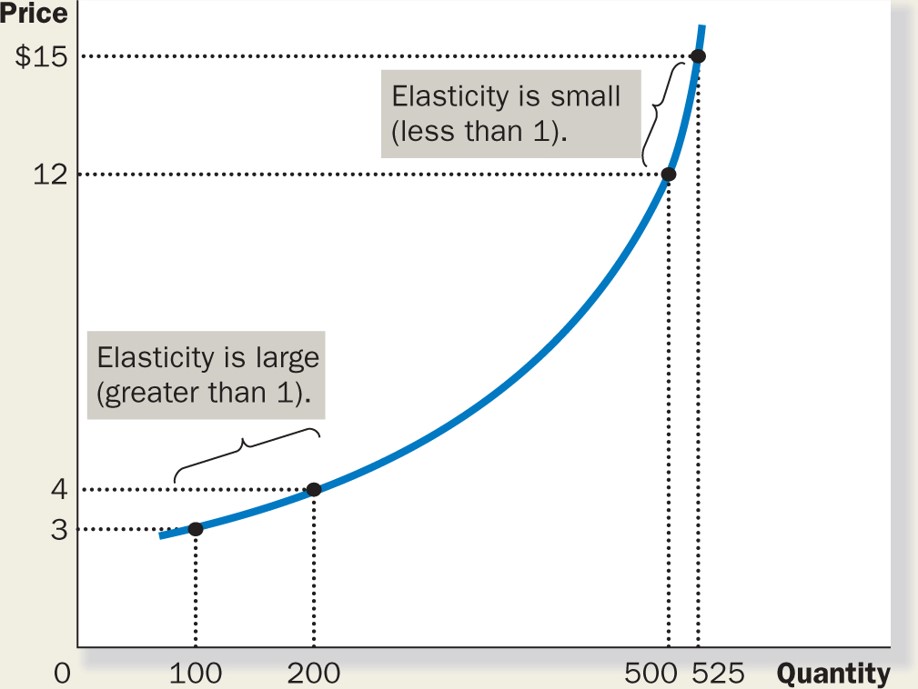

Elasticity

is the sensitivity of

one variable to a change in another variable.

Unlike

the constant slope of a straight line is measured ΔY/ΔX or rise over run,

Elasticity varies even along a straight line (P&B 7th Ed

Fig. 4.4;

R&L

13th Ed

Fig. 4-2;

MKM

Fig. 5.4).

It is measured (ΔY2-Y1/Y1)/(ΔX2-X1/X1)

i.e., the change in Y divided by the change in X.

Economic theory recognizes three principal types of elasticity:

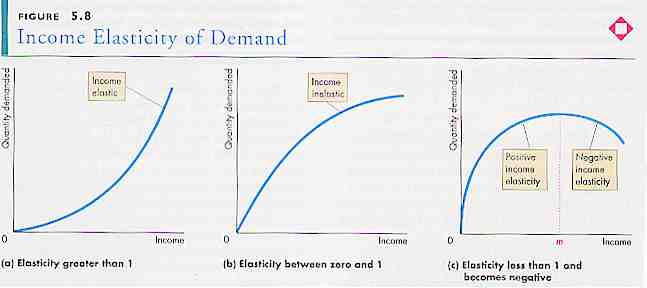

i - income elasticity

-

with price constant, the change in demand caused by a change in income

(P&B

4th Ed.

Fig. 5.8);

ii

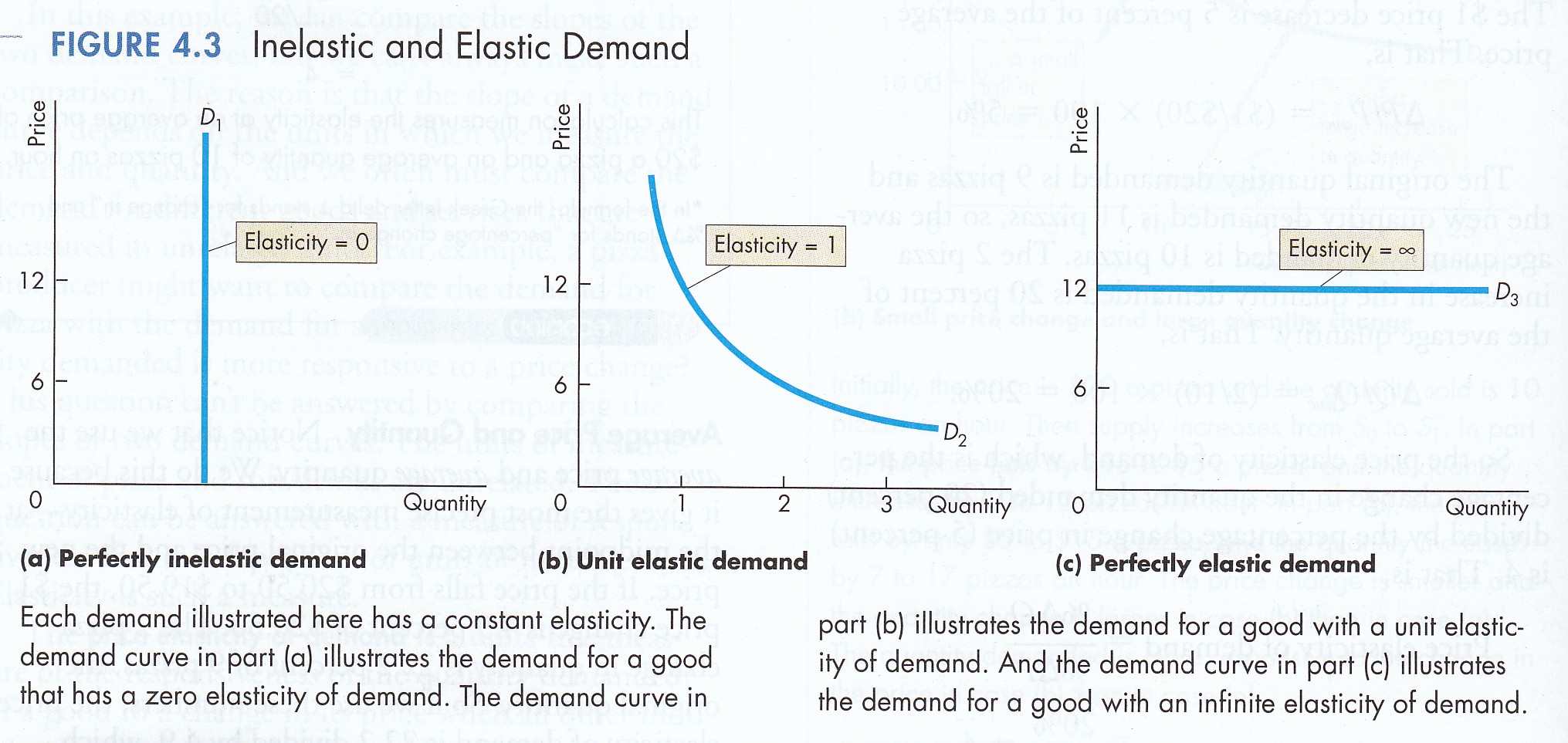

- price elasticity -

the change in demand or supply caused by a change in price (P&B

4th Ed.

Fig. 5.8; 7th Ed

Fig 4.3; R&L

13th ED.

Fig. 4-2 &

4-3,

MKM Fig's 5.1

a,

b,

c &

d) or

supply (P&B

7th Ed

Fig.4.8; R&L

13th Ed

Fig. 4-6,

MKM Fig. 5.5

a,

b,

c,

d &

e,

MKM Fig. 5.6).

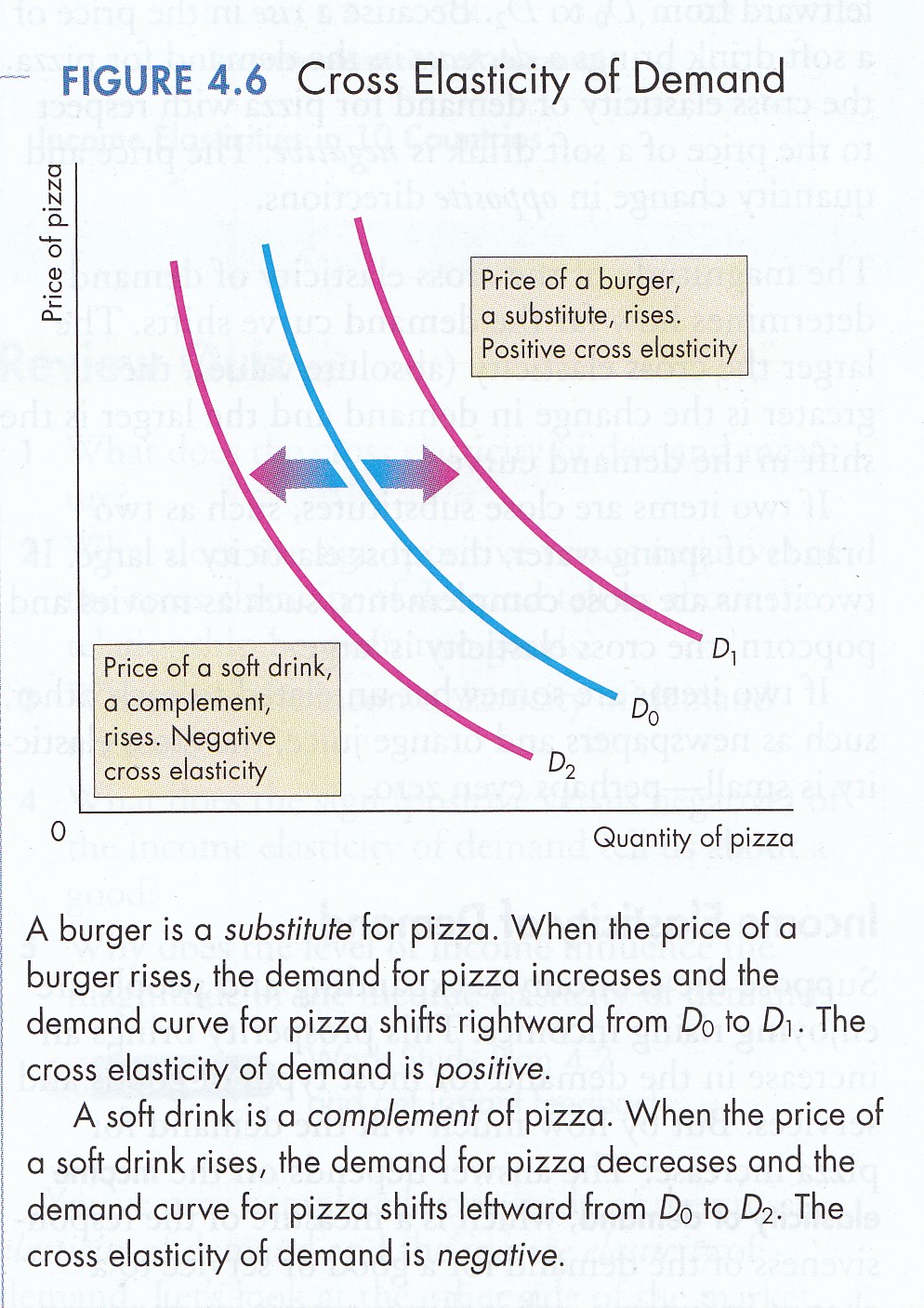

iii

- elasticity of substitution or cross-elasticity

- either (a) the change in demand for a factor of production (Capital) caused by

a change in the price of another factor (Labour); or, (b) the change in the

demand for one commodity (hamburgers) caused by a change in price of a competing

or substitute commodity (pizza)

(P&B

7th Ed Fig.4.6).

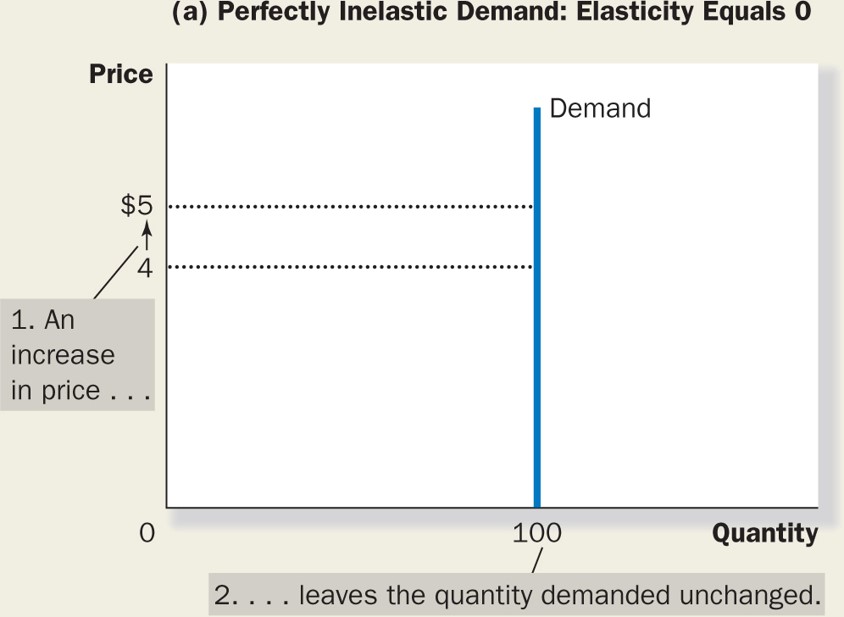

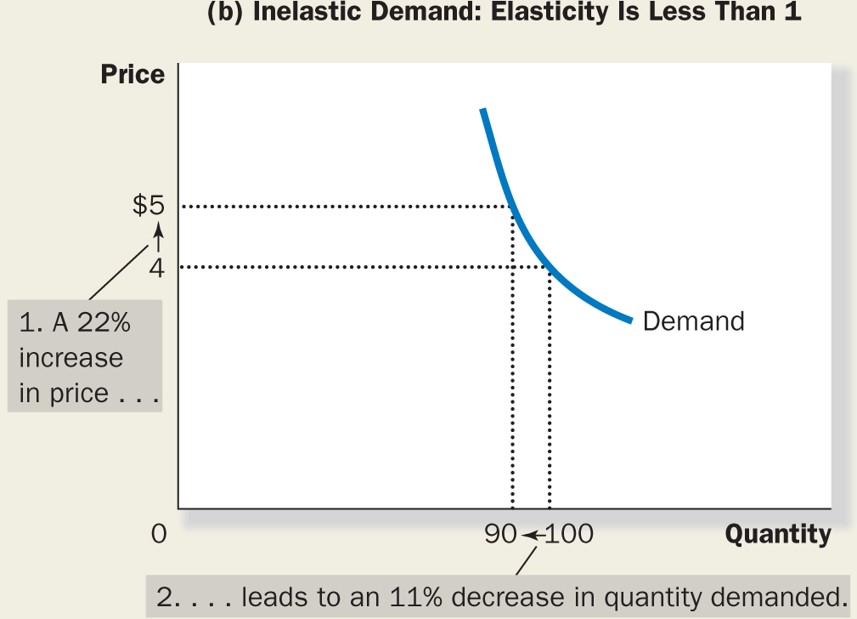

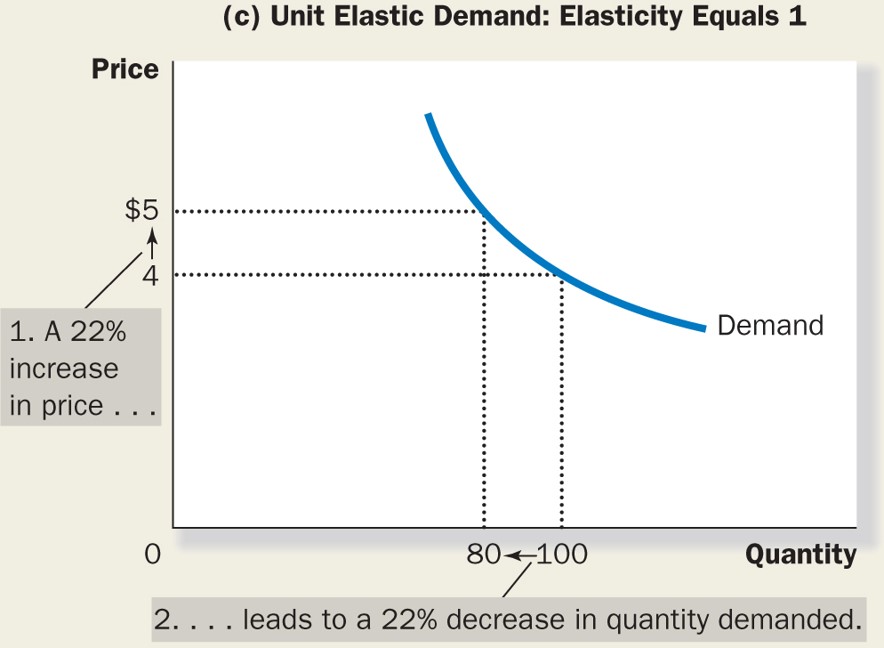

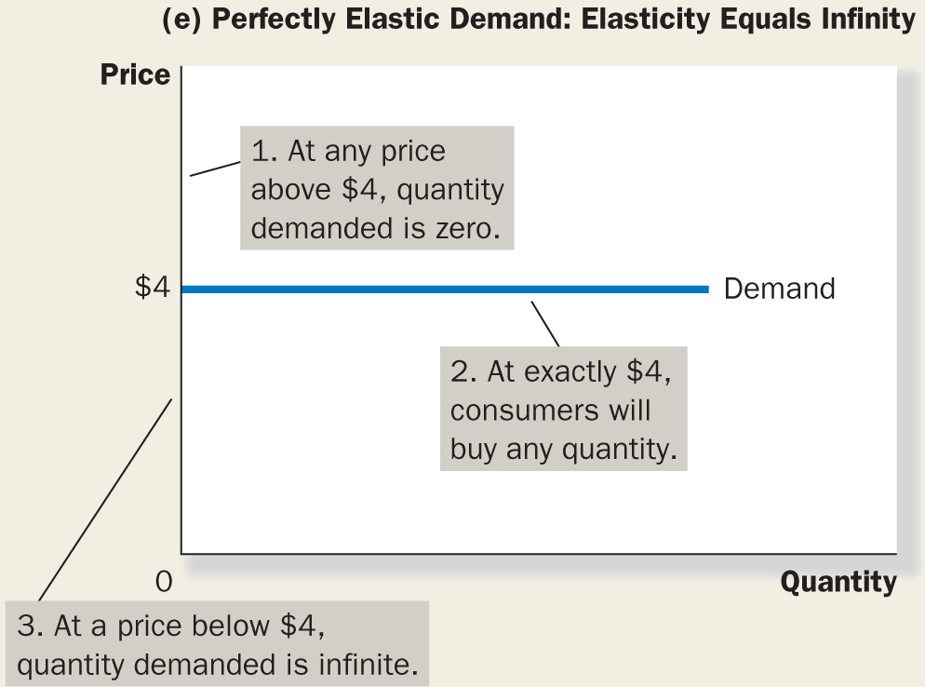

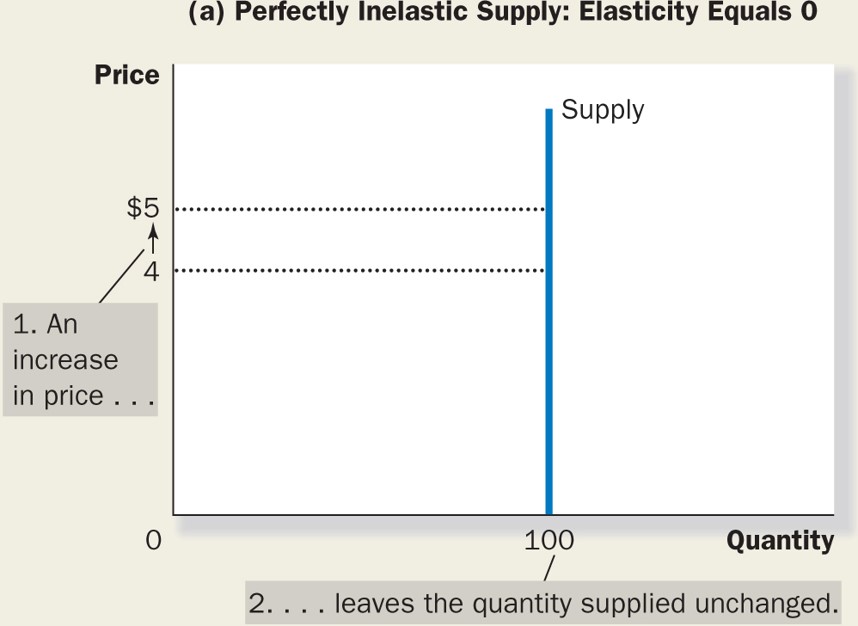

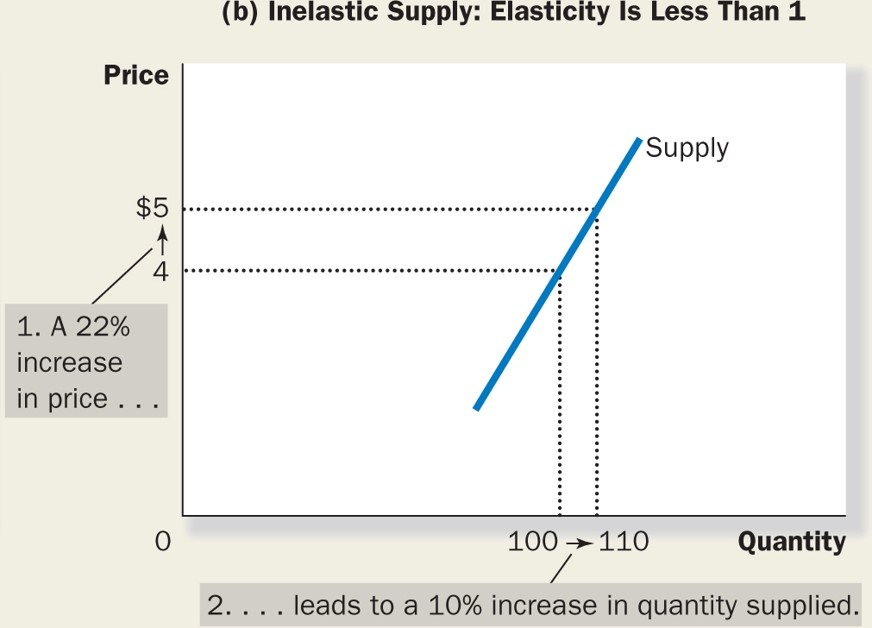

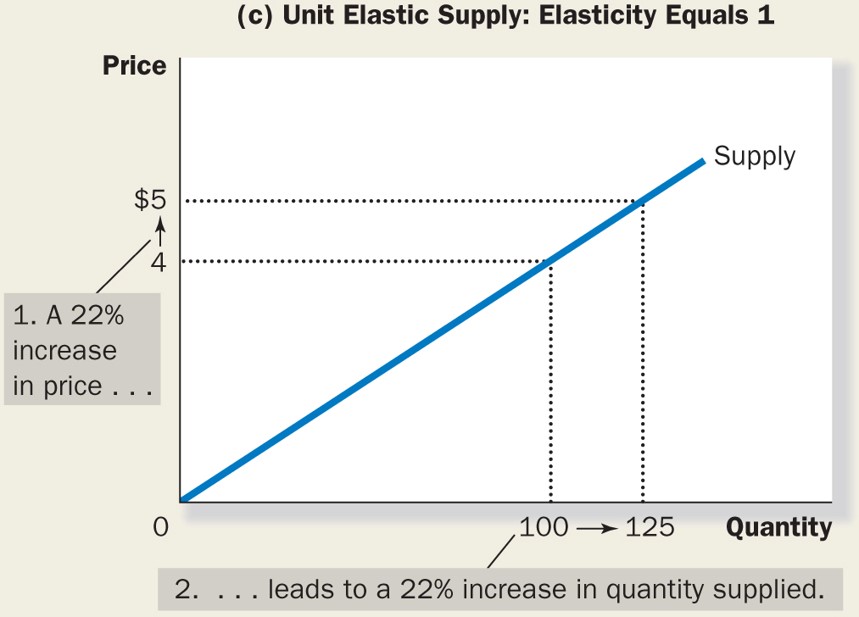

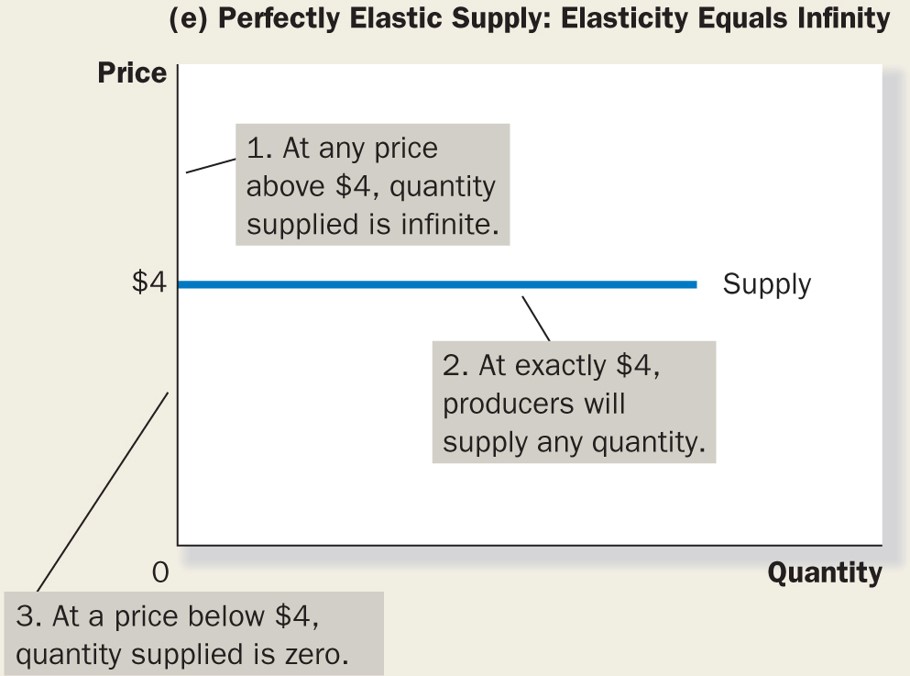

In all three types

elasticity may be:

greater than one

(elastic) - a near horizontal demand or supply curve where a small

increase in price causes a large change in demand or supply;

equal to one

(unitary elasticity); or,

less than one (inelastic) - a near

vertical demand or supply curve where a large change in price causes

little change in

demand or supply.

As will be seen,

Elasticity places a critical part in choices of consumers and producers.

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}