|

0.

Introduction

Scholar's say national income accounting dates back to either: William

the Conqueror's 11th century 'Doomsday

Book' of England or

William Petty's 17th century

Political Arithmetick,

arguably the later

result of his initial survey of Ireland after Cromwell's' conquest or

Francois

Quesnay's

18th

century

Tableau économique

(Economic Table or what today is called the

input-output table

of an economy).

In fact, it was not until 1944 that the concept became an

accounting

reality.

Discussions during

World War II between the United States, the United Kingdom and Canada

resulted in the framework and rules for what

became the System of National Accounts. Discussions drew on

extensive statistical development in the United States by:

W. C.

Mitchell

who established the

National

Bureau of Economic Research and was a member of the American Institutional School of Economics;

Joseph

Schumpeter's

statistical work on business cycles; and,

especially,

Simon Kuznets

work on national income.

Such

statistical evidence and analytic tools were used to erect the most

extensive accounting system in human history. The dream of

Physiocrat

Frenchman

Francois

Quesnay

was finally realized.

From these

streams of thought the

System

of National Accounts (SNA) was born with

Canadian statisticians as

midwife. In 1947, the

United

Nations issued standards for national SNAs together with

associated sub-sets such as the

Standard

Industrial Classification,

Standard Commodity Classification,

et al. They are used by all Member States

today including the

European Union. In addition the

Census of Population and the

Business Enterprise are consistent with these definitional

standards.

A parallel U.N. system

of

'material balances'

(SMB) was adopted for Second World countries, i.e. the

'command economies' of Communist Nation-States.

Without the

price system and its information richness the system failed. The U.N. no longer publishes the 'material balances' manual.

Having studied the Soviet economy I will offer some additional insights

in my lecture.

With respect to the

Standard Industrial Classification there are three major sectors to the

economy: Primary, Secondary & Tertiary.

The Primary or the Extractive Sector

includes farming, fishing, forestry and mining accounting for 5% of

Canadian GDP. The Secondary or Manufacturing Sector accounts for

about 25%. The Tertiary or Service Sector accounts for about 70% of

Canadian GDP. Essentially the Service Sector involves intangibles

including financial transactions, e.g., fees for 'wealth

management' as well as virtual goods, i.e., software programs.

As the Covid Pandemic and

NATO/Russian War demonstrates, increasing GDP through the Tertiary or

Service Sector cannot buy PPE (personal protection equipment including

pharmaceuticals) or 155mm artillery shells without the necessary

Secondary Manufacturing infrastructure. This should lead to

a refocusing on the ‘Real Economy’ involving tangible outputs of Primary

and Secondary Industries. It should be noted that Western economies

have suppressed Primary Industries and off-shored manufacturing

in pursuit of the so-called 'Green Dream'.

1. Gross Domestic

Product

(MKM C 5 - all editions)

GDP is the aggregate total of all final goods and services

produced within a country measured in dollars and cents per

unit time. It is generally considered the best available

measure of the productive capacity of a Nation-State, and, in turn,

GDP per capita (per person) is commonly accepted as a primary measure of the overall well-being of a

Nation-State's citizens.

In the Standard Model it is

assumed:

-

first, all

factors of production are ultimately owned by households including share

ownership of all firms;

-

second, only

'final goods & services' are included

to avoid double

counting, i.e., it excludes

goods & services

firms buy from

one another and used as 'intermediate' inputs to their own production

process;

-

third,

Government buys

goods & services from firms. Government produce nothing itself,

everything is privatized; and,

-

fourth, GDP

always equals Gross Domestic Income

(GDI) - the aggregate earnings of domestic factors

of production such as capital, labour and natural resources. GDP

≡

GDI is thus an accounting

identity.

Alternatively, Gross National

Product (GNP) is the aggregate total of all final goods and services

consumed within a country measured in dollars and cents. The

essential difference with GDP is imports, i.e., goods and services not

employing domestic factors in their production. Most economists accept GDP

but Adam Smith, among others, believed

GNP more accurately measures the well being of a nation.

i - Concepts

To track GDP requires

three basic concepts: Stocks, Flows and Equality of GDP & GDI.

a) Stocks

& Flows (measured in dollars and cents per unit time)

A

stock is a quantity that exists

at a moment in time. A flow is a quantity added to or subtracted from a

stock.

i - Capital &

Investment

With respect to GDP:

Capital

(K) refers to the stock of plant, equipment,

buildings, inventories of raw materials, semi-finished goods and housing

stock;

Depreciation (D)

refers to the decrease in the capital stock resulting from

wear and tear; and,

Investment

(I) refers to the flow of new capital where gross investment is the total flow of

new capital and net is the flow of new capital less depreciation

ii -

Wealth & Income

With respect to GDP:

Wealth

refers to the stock of all

property - moveable and immoveable, tangible and intangible - including financial assets;

Income (Y)

refers to the flow of money

earned by supplying factors

of production; and,

Disposable Income (Yd)

refers to

gross income less net taxes (total

taxes minus transfers from Government to households)

iii - Consumption & Saving

With respect to GDP:

Consumption

(C):

refers to disposable income spent on

final goods & services, and,

Savings

(S)

refers to disposable income minus consumption

equalling an addition to wealth.

b) Equality of

Gross National Income

(GNI) & Expenditure (GNE)

(measured in dollars and

cents per unit time)

In an open economy

the Standard Model engages 4

actors: households, firms, government

and the rest of world operating in three markets – factor, goods & services and

financial markets (P&B

Fig. 22.2;

R&L

13th Ed

Fig. 1-4). The flows

involved include:

i -

Households

With respect to GDI:

GDI (Yi)

refers to total

earnings of households for supplying factors of production to firms

and other countries including profits & dividends, and,

Disposable Income (Yd)

refers to Y -

Net Taxes (NT: taxes minus transfers from Government to households).

With respect to GDE:

Consumption (C)

refers to total

spending

by households for goods and services

produced by firms, and,

Savings (S)

refers to Yd - C used by firms to finance Investment.

ii - Firms

With respect to GDI:

Revenue

refers to earning of firms from sale of

goods &

services and financial transactions

to households, Government and other

countries

With respect to GDE:

Investment

(I) refers to expenditures by firms for depreciation, new plant & equipment, buildings and additions to

inventories paid out of

savings and foreign investment.

iii -

Government

With respect to GDI:

Net Taxes (NT) = Total taxes

from minus Transfers from Government to households

With respect to GDE:

Government Expenditures (G)

refers to goods & services purchased from firms, foreign and

domestic.

Balance = NT - G =

0

Surplus = NT - G >

0 finances new programs, debt and/or deficit reduction

Deficit = NT - G <

0 financed by borrowing

Debt = accumulated deficits

minus

surpluses

iv - Rest of

World

With respect to GDE:

Exports (X)

refers to sales of

goods &

services and financial transactions

to other

countries;

Imports (M) from all other

countries

including goods & services

and financial transactions, and,

Net Exports (NE) = X – M

NE > 0 = trade surplus

NE < 0 = trade deficit

c) Accounting Identity (measured in dollars and cents per unit time)

GNE (Ye) = C + I + G + NE

GDI (Yi) =

household earnings from supplying factors of production to firms including

profits & dividends spent on C + S + T

Identity: Yi = C + S + T

≡

Ye

= C + I + G + NE

where

I + G + X

(injections)

≡

S +

T + M (leakages)

Leakage = income not spent on domestically produce goods

& services including

savings, taxes and imports

Injection = expenditure by firms,

government and exports

iii - Measuring GDP

GDP can be measured in 3 ways by: Expenditure,

Factor Income

or Value Added

(all measured in dollars and cents per unit time)

a) Expenditure

(Statistics Canada)

Personal expenditure on consumer goods and services

(not include

new residential housing part of investment)

Business investment: plant & equipment including new

residential housing, inventories of raw materials,

semi-finished products,

unsold final product

Government expenditures on goods and services

excluding transfer

payments

Export of goods and services

Imports of goods and services

Exclusions include:

intermediate goods & services

(to avoid double

counting goods & services firms buy from each other as

'intermediate' inputs to

their production process)

used goods

(already counted when new)

financial products

b)

Factor Income

(Revenue Canada)

Wages, salaries and supplementary labour income including

take-home pay, taxes withheld plus fringe benefits

Corporate profits

including dividends paid and retained or

undistributed profits

Interest and misc. investment income

including net interest

payments by households, land rent

and imputed rent for owner-occupied housing

Farmers’ income & income from non-farm unincorporated businesses

c) Value Added

As noted above,

certain expenditures are excluded from GDP. These include, among

others, intermediate

or 'producer' goods & services, used or second-hand goods and financial

products. In the case of intermediate inputs

this

is done to avoid double counting when firms buy inputs from each other

for their

production process.

GDP

is calculated by summing up the value added by each agent that excludes

the cost of inputs.

Consider the following

simplified table:

|

Agent |

Output |

Value Added |

Market Price |

|

|

Farmer's Input * |

$100 |

$100 |

|

Farmer |

Wheat |

$100 |

$200 |

|

Miller |

Flour |

$100 |

$300 |

|

Baker |

Bread |

$100 |

$400 |

|

Store |

Retail |

$100 |

$500 |

|

Total |

|

$500 |

$1500 |

* Imputed cost of land,

equipment, seed, fertilizer, pesticide, labour & profit

In the case of used

goods, no new inputs are employed, no value is added, no factor income

is generated. Their sale is a transfer of ownership not the result

of production. Financial products like stocks and bonds are not

included because they are Savings (S).

d) Net vs. Gross

Domestic Product

Gross Domestic

Product (GDP) = NDP + depreciation or capital consumption

Net Domestic

Product (NDP)

= gross domestic product minus depreciation of capital

goods.

e)

Why Expenditure & Income Approach to GDP?

While GDP and GDI must be equal

they are calculated using different sources. Expenditure

data are collected by Statistics

Canada using the Census and

surveys while income numbers are collected by

Revenue Canada using tax data. This allows Stats Canada to check one

against the other and introduce (and explain) any error term to ensure the

identity.

iii - Price Level and Inflation

(MKM C6 - all editions)

As will be seen (5.2.1

Money) dollars and

cents are the most useful measure of economic activity. For

example, you can't compare apples and oranges but you can compare their

prices. Nonetheless dollars and cents measurement has its

problems. These include price inflation and deflation.

For example, if the price of a

chocolate bar goes up you still get only one at the new price. For

purposes of GDP, measured in dollars and cents, there has been an

increase but there is no corresponding increase in the number of

chocolate bars. Overtime the discrepancy between

monetary

or nominal

GDP and real GDP measured by the number of chocolate bars

plus of all other goods & services grows ever wider. This makes knowing

if the economy is growing, shrinking or stagnating difficult.

2. Nominal vs. Real GDP (MKM C 6 -

all editions)

To measure real GDP the

aggregate price level is calculated. This is the average for the

prices of all goods and services included in GDP. This is done

using a price index. The

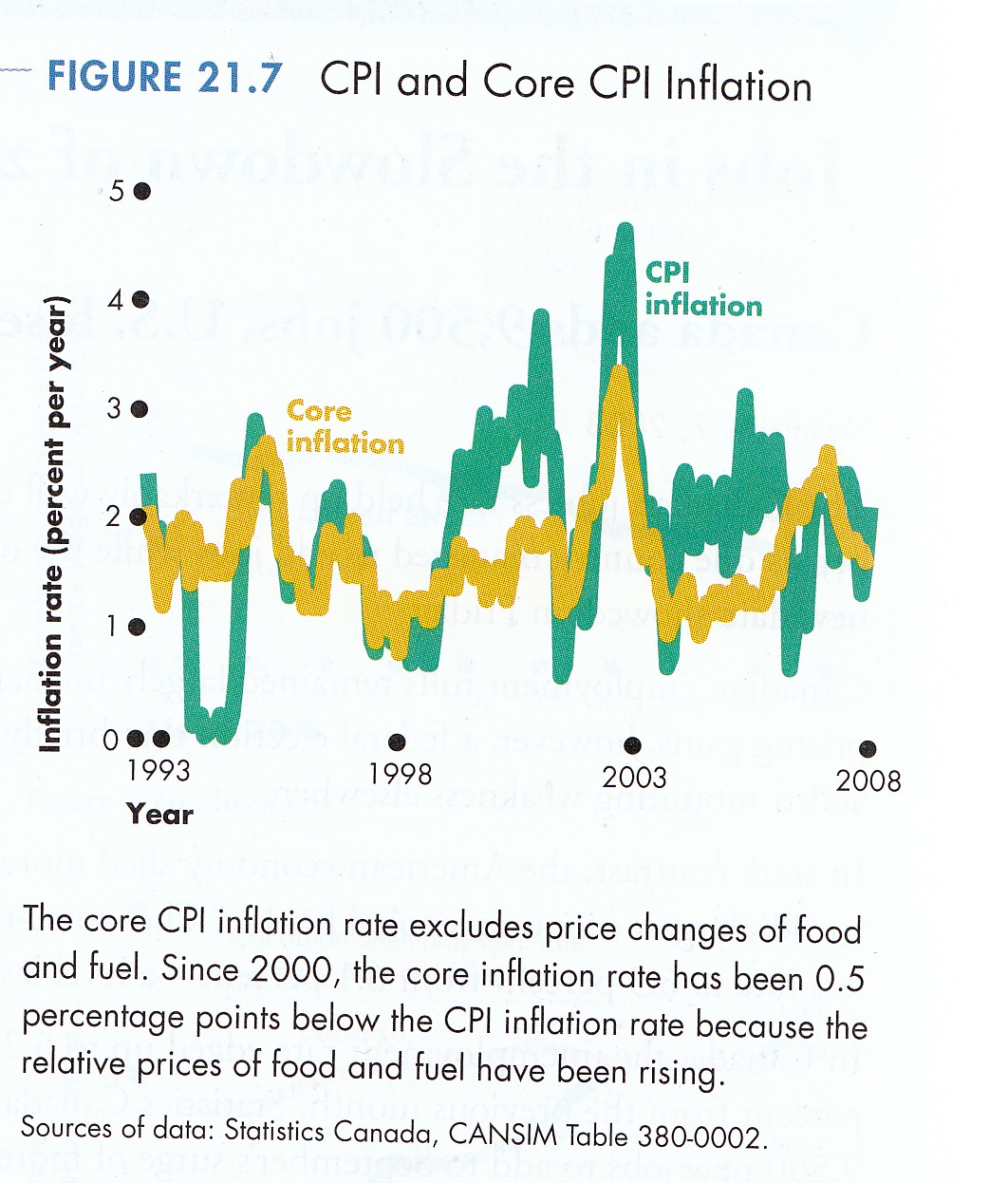

two major indices are the Consumer Price Index (CPI) and the GDP

Deflator (P&B 7th Ed CPI & Core Inflation

Fig. 21.7; R&L 13th Ed

Fig. 29-5). It should be noted that there are special price

indexes for all major industries due to their different mixes of inputs

in production.

a)

Consumer Price Index

(CPI) (MKM C6/124-127)

The

CPI measures

the average level of prices of goods and services purchased by

typical Canadian family. It uses a base year to calculate cost of the typical ‘basket’ of goods

and services then calculates cost of same basket in subsequent years to determine

change in price level where:

CPI = current cost of basic/base period cost x 100

b) GDP Deflator

The GDP Deflator

measures the average level of prices of all goods & services in GDP.

Nominal GDP is valued in current year prices while real GDP is valued

in base year prices, or:

GDP Deflator =

Nominal/Real GDP x 100

Because the

GDP Deflator

isn't based on a fixed

basket of goods & services, it has an advantage over

the

Consumer Price Index. Changes in consumption patterns or the

introduction of new goods and services are automatically reflected.

c) Meaning of Inflation Numbers

The CPI is often used for cost of living adjustments showing changes in

the purchasing power of money and allowing measurement of how much

income must increase in nominal terms to purchase the same basket of

goods in subsequent years.

The GDP Deflator is used to measure the real growth of the overall

economy. Like a balloon nominal GDP swells the balloon simply

because of increased prices rather than growth in the real quantity of

goods & services produced. The deflator shrinks the balloon back

to measure the real increase in output of an economy.

It should be noted

that there are separate

price indices for major industries, e.g., the health industry

employs a very different basket of goods than the typical Canadian

household. Similarly, the auto or construction industries have

very different typical baskets of goods & services and hence different

rates of inflation.

However, the CPI suffers from technical biases:

substitution (substitute less for more expensive goods and services

not reflected in base basket);

new goods

not reflected

in base basket;

and,

quality

change in goods & services.

In addition, non-market activity such as household production and the

underground economy (illicit goods & services) are not reflected in

nominal or real GDP.

3. Happiness,

Purchasing Power, Intra-Corporate Transfer Pricing & the Knowledge-Based/Digital Economy

Beyond technical

problems associated with measuring GDP there is the question of the

adequacy of GDP per capita as a measure of national well-being or

'happiness'. In

this regard, it is assumed in Economics, following the insights of

Jeremy Bentham (Observation

#8), that the willingness of a consumer to spend $10 on a DVD

means the consumer expects to receive at least $10 worth of utility or

happiness. One necessary adjustment involves making international

comparisons and requires adjustment for

purchasing

power parity index of prices (MKM C12/ 292-4:

273-76; 283-285) including the commonly

used 'Big

Mac Index' :

Purchasing power

parity (PPP) is a theory which states that exchange rates between

currencies are in equilibrium when their purchasing power is the same in

each of the two countries. This means that the exchange rate

between two countries should equal the ratio of the two countries' price

level of a fixed basket of goods and services. When a country's

domestic price level is increasing (i.e., a country experiences

inflation), that country's exchange rate must depreciated in order to

return to PPP. (Werner

Antweiler, University of British Columbia)

Since the 1960s

economist and other scholars have developed supplementary ‘social indicators’

to better measure the true well-being of a country's citizens.

Currently they include

Bhutan's

Gross

National Happiness Index, the

UN

Development Index and the

OECD Life

Index. Such

indices

attempt to

include things like

health, leisure, the environment, freedom and justice (see:

http://www.cbc.ca/news/business/peter-armstrong-economic-indicators-1.3754915.

The problem, of course, is quantifying such life affecting factors.

Compared to counting GDP in dollars and cents such efforts are

problematic.

There is another problem with measuring GDP.

Generally tangible things,

are easy to count, e.g., wheat, coal, cars, etc. These

constitute tangible imports or exports. Other things, generally intangible

things, are more difficult to count, e.g., intellectual property

royalties, management fees, etc. This puts a bias into the final

count. Furthermore, with multi- or trans-national corporations there is

the problem of intra-corporate transfer pricing which involves, among other

things, maximum avoidance of tax given the different jurisdictions in which they

operate.

And there is an emerging problem

affecting calculation of real GDP - the

Knowledge-Based/Digital Economy. As recently

noted by the former CEO of IBM, Sam Palmisano, in his article “The

Global Enterprise” (October 14, 2016, Foreign Affairs), there

has been:

… an

explosion of data, and with it a re-calculation of economic value -

asset values - affiliated with this data-rich environment.

Tangible assets, which are characteristic of the physical world, are

being subjected to the economic headwinds of slow global growth. But

intangible assets, which are characteristic of the digital world, are

finding their value increasing and economic wind at their back.

Consider Google Maps

and other so-called 'free

apps'. The are not sold on the market so they are not included in

calculation of GDP. Yet they arguably have significant economic

impact, e.g., reducing the costs of navigation and delivery of

goods & services. Furthermore, while they are 'free' in the

sense of dollars and cents to the consumer they have a price visible in

the

Big Data voluntarily provided by consumers in exchange for the apps. The scale of the problem is

highlighted in Jacob Weisberg’s “They’ve Got You, Wherever You Are”

(October 27, 2016,

New York Review of Books) where he notes:

Facebook’s vast trove of

voluntarily surrendered personal information would allow it to resell

segmented attention with unparalleled specificity, enabling marketers to

target not just the location and demographic characteristics of its

users, but practically any conceivable taste, interest, or affinity.

And with ad products displayed on smartphones, Facebook has ensured that

targeted advertising travels with its users everywhere.

For those so interested please see my

articles:

Value without Price or Value Theory Redux

Disruptive Solutions to Problems Associated with the Global

Knowledge-Based/Digital Economy.

There is, however, another problem with

public or government statistics. Ongoing austerity and privacy

concerns have limited the ability of Statistics Canada to collect data

on important public policy issues. In addition, unlike in the

United States information collected and analyzed by the Government is in

the public domain. Their reasoning: taxpayers paid for it.

This is not the case in the constitutional monarchies including Canada.

For an analysis of the Canadian situation please see: In the Dark: The

Cost of Canada's Data Deficit:

https://www.theglobeandmail.com/canada/article-in-the-dark-the-cost-of-canadas-data-deficit/

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}