Some argue that Basic

Conditions lead to Structure; Structure leads to Conduct; and,

Conduct leads to Performance. Others, however, including Joe

Bain, argue that Structure leads to Performance. In either case

the question remains: How well does an industry perform –

internally and externally?

Internal Performance is

reflected by, among other things, how efficiently an industry

utilizes its resources, accounts for its opportunity costs and

benefits and the profit that it earns. External Performance is

reflected by, among other things, the external costs and

benefits an industry generates in the natural environment or

biosphere and in society. This last point is critical.

Performance accounts not just for costs and benefits internal

but also external to the industry such as environmental impact

and economic equity. Put another way: the economy is a means to

satisfy human ends; it is not an end in and of itself.

4.1

Allocative Efficiency & Profitability

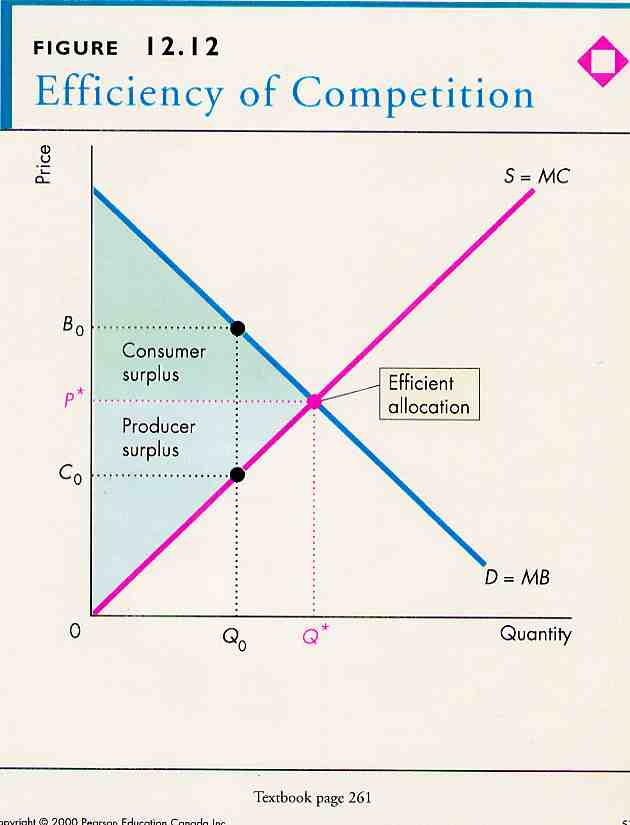

Allocative efficiency implies

all factors of production and all commodities demanded by

consumers are in their best use and receive their opportunity

cost. Further, it is assumed that there are no external cost or

benefits, i.e. all external costs and benefits have been

‘internalized’. Three conditions must hold:

(i) Consumer

Efficiency: when consumer cannot increase utility by

reallocating budget;

(ii) Producer

Efficiency: when firm cannot reduce cost by shifting input

mix;

(iii)

Exchange Efficiency: when all gains from trade have been

exhausted. Gains from trade to consumer is called consumer

surplus which measures difference between what consumer are

willing to pay and what they actually pay for a total quantity

of a good or service at market price. Gains from trade to

producers are called producer surplus which measures the

difference between what producer are willing to accept and what

they actually receive for providing a market equilibrium level

of supply (P&B 4th Ed.

Fig. 12.12;

5th Ed. Fig. 11.12;

7th Ed Fig.

12.12; R&L 13th Ed not displayed).

I will now examine allocative efficiency and profitability of

the four forms of market competition.

Perfect

Competition

To determine profit-maximizing output of a firm under perfect

competition, one can use two methods:

(i)

total revenue less total cost; and,

(ii)

marginal analysis.

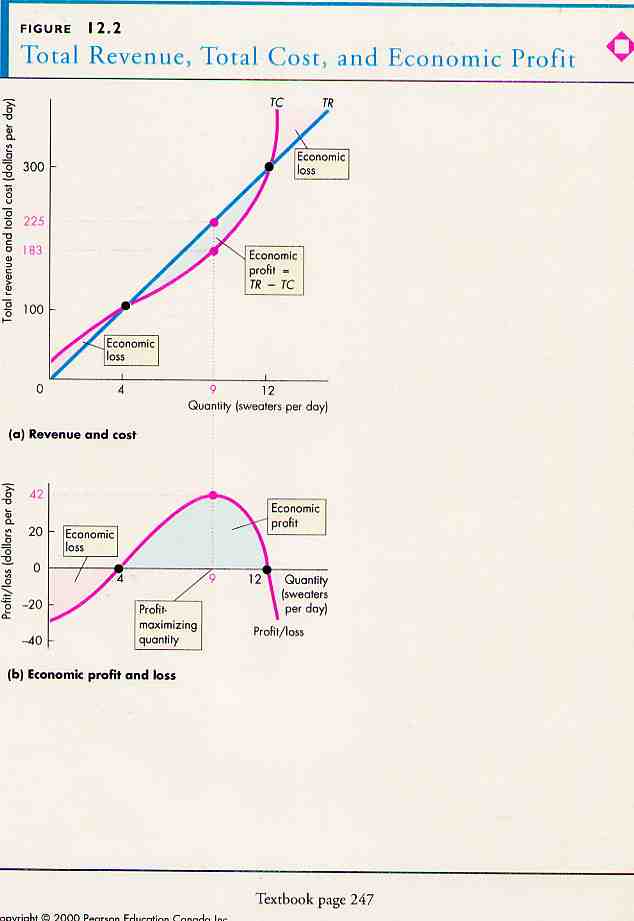

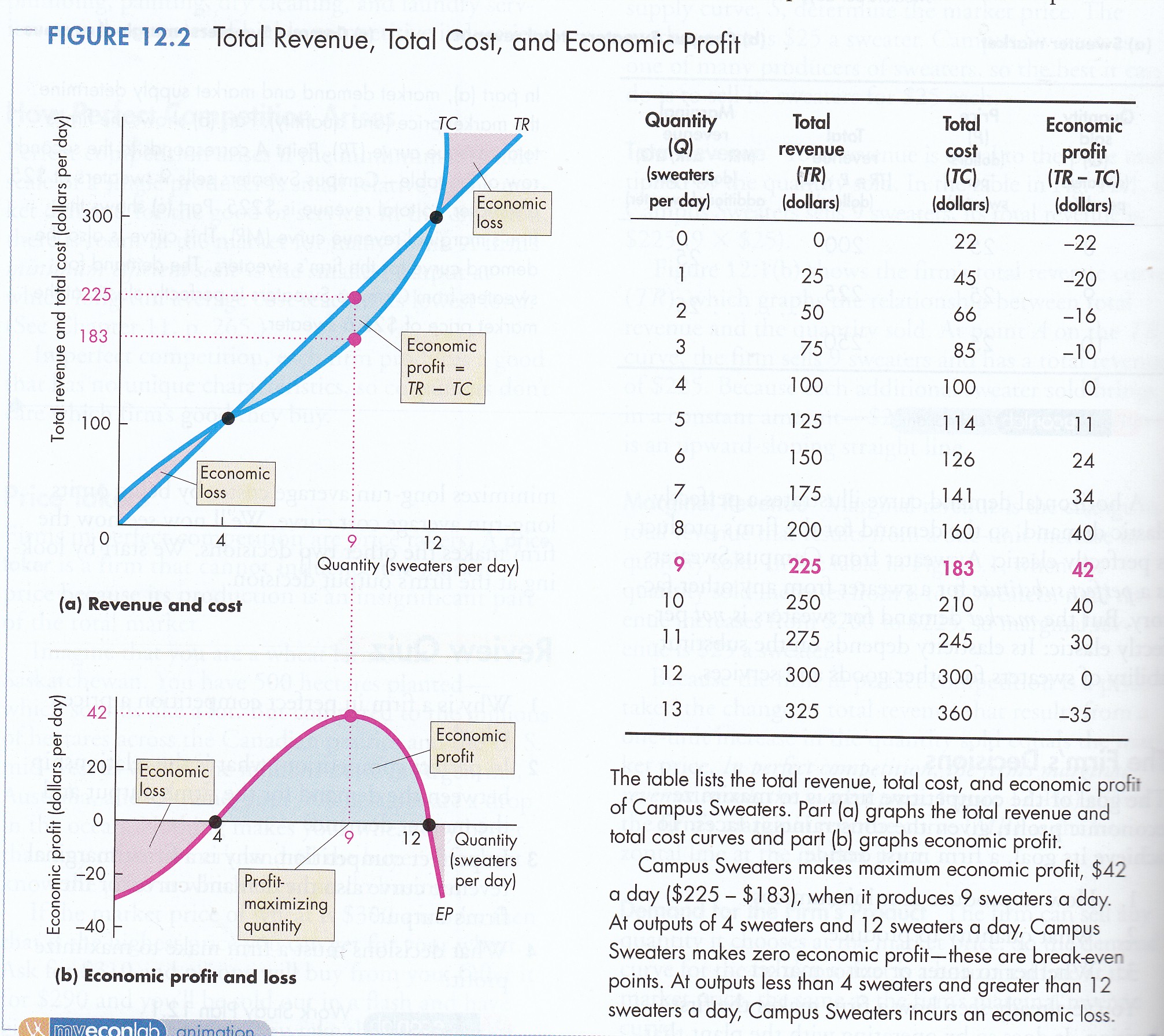

(i) Total Revenue

less Total Cost

Profit equals TR – TC. By plotting TR and TC curves one can see the

changing relationship: initially there is a section of economic

loss followed by economic profit followed by economic loss with

two points of ‘normal’ profit points (P&B 4th Ed.

Fig. 12.2;

5th Ed Fig. 11.2;

7th Ed Fig.

12.2; R&L 13th Ed

Fig. 9-4i).

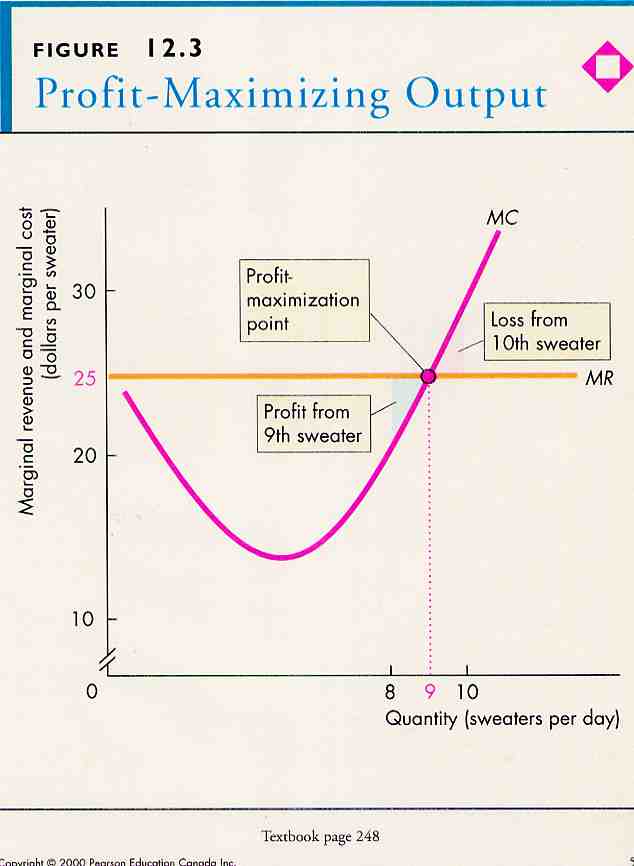

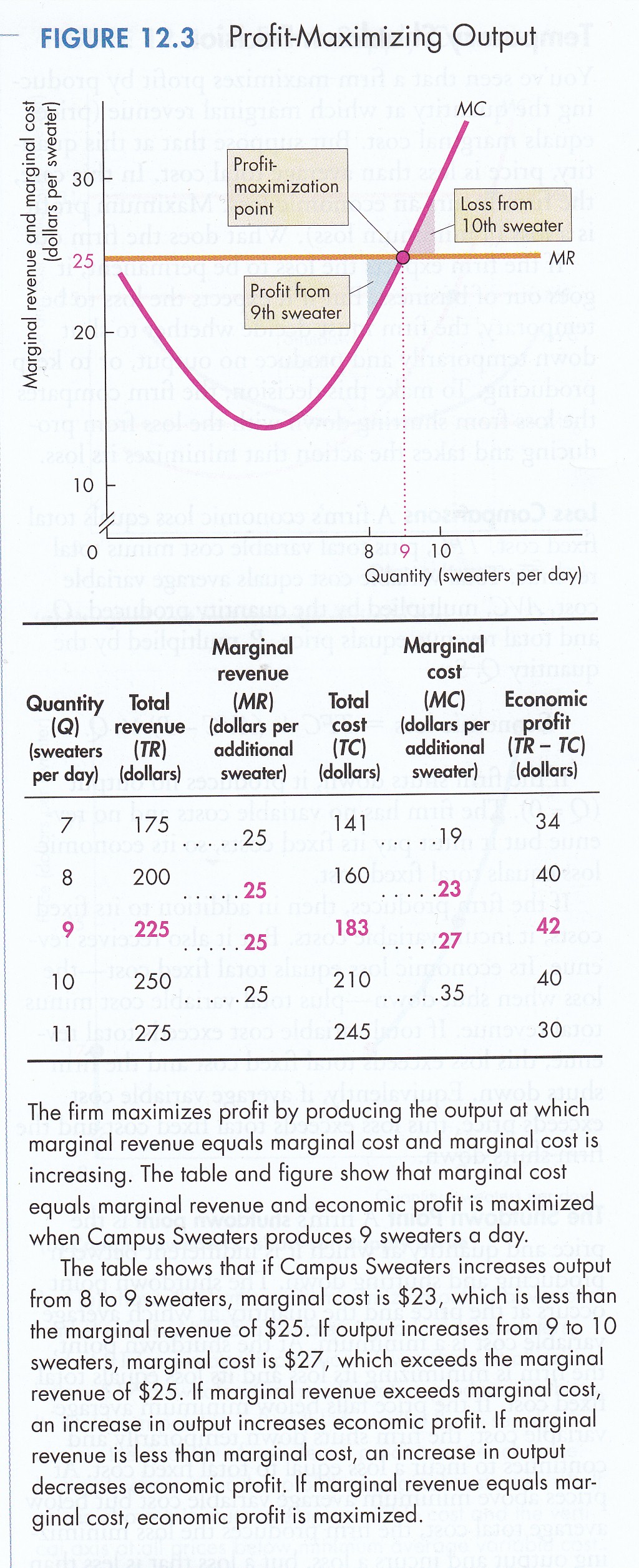

(ii) Marginal Analysis

Marginal revenue (MR) can be compared with average cost (AC). To

maximize profit a firm must sell at MR = P = MC. But if MR >

AC producing an additional unit output will add more revenue

than cost, i.e. economic profit earned in the SR. If MR

= AC then ‘normal profit’ is earned, i.e. all factors of

production paid their opportunity cost value. If MR < AC

producing another unit with result in a loss (P&B 4th Ed.

Fig. 12.3;

5th Ed. Fig. 11.3; P&B

7th Ed Fig.

12.3; R&L 13th Ed

Fig. 9-4ii).

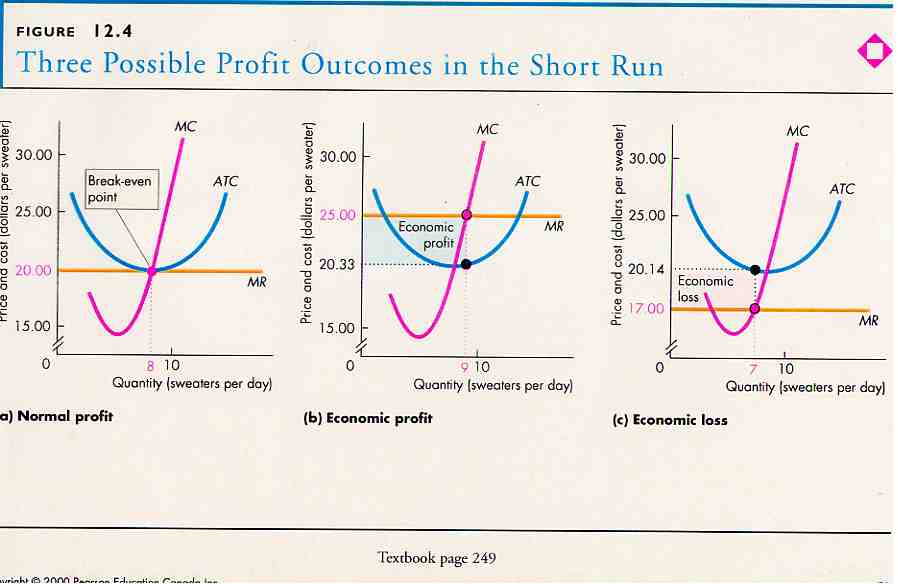

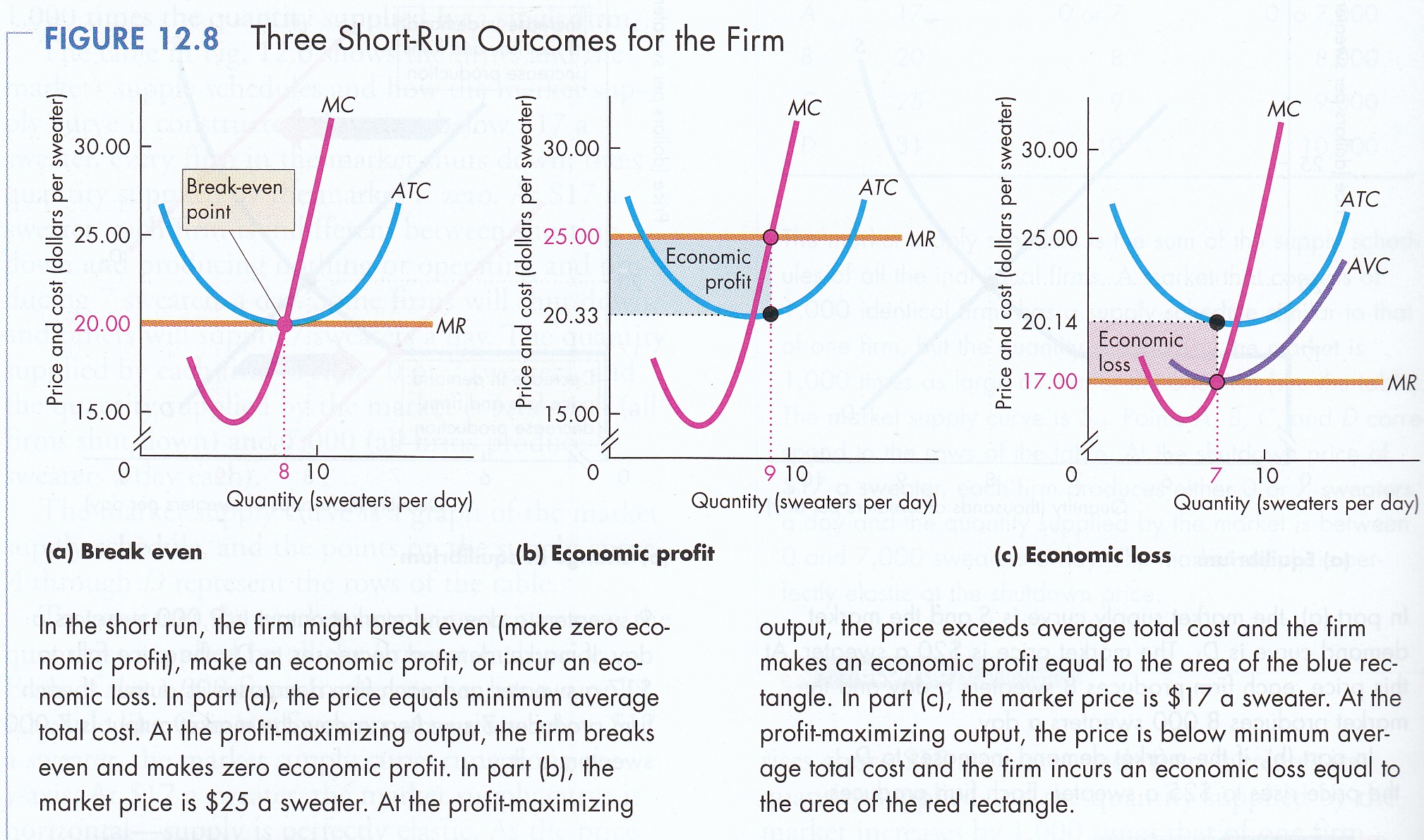

Three possible outcomes are possible for the firm in the

short-run: normal profit, economic profit or economic loss (P&B

4th Ed.

Fig. 12.4;

5th Ed. Fig. 11.4;

7th Ed Fig.

12.8; R&L 13th Ed

Fig. 9-8).

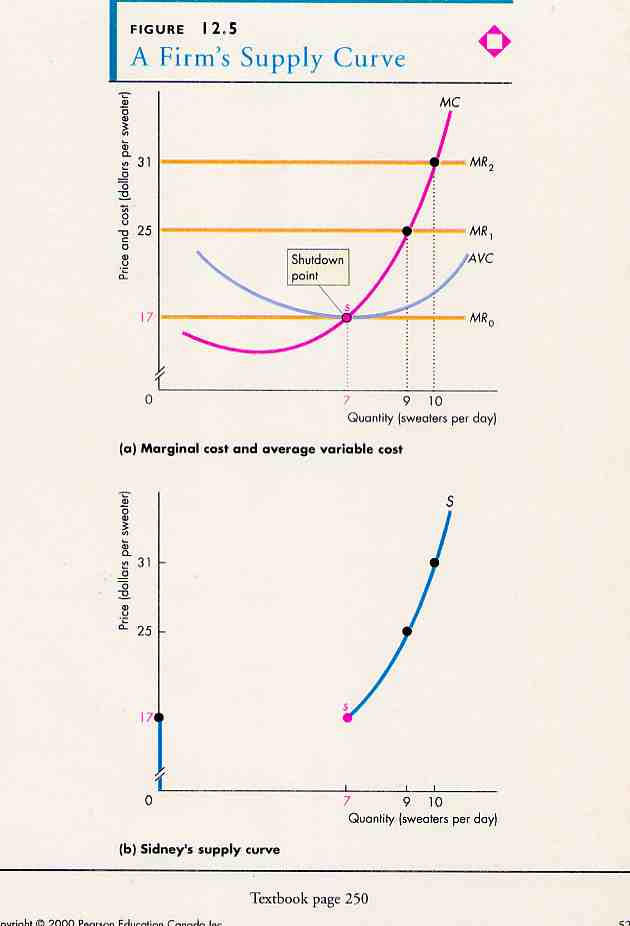

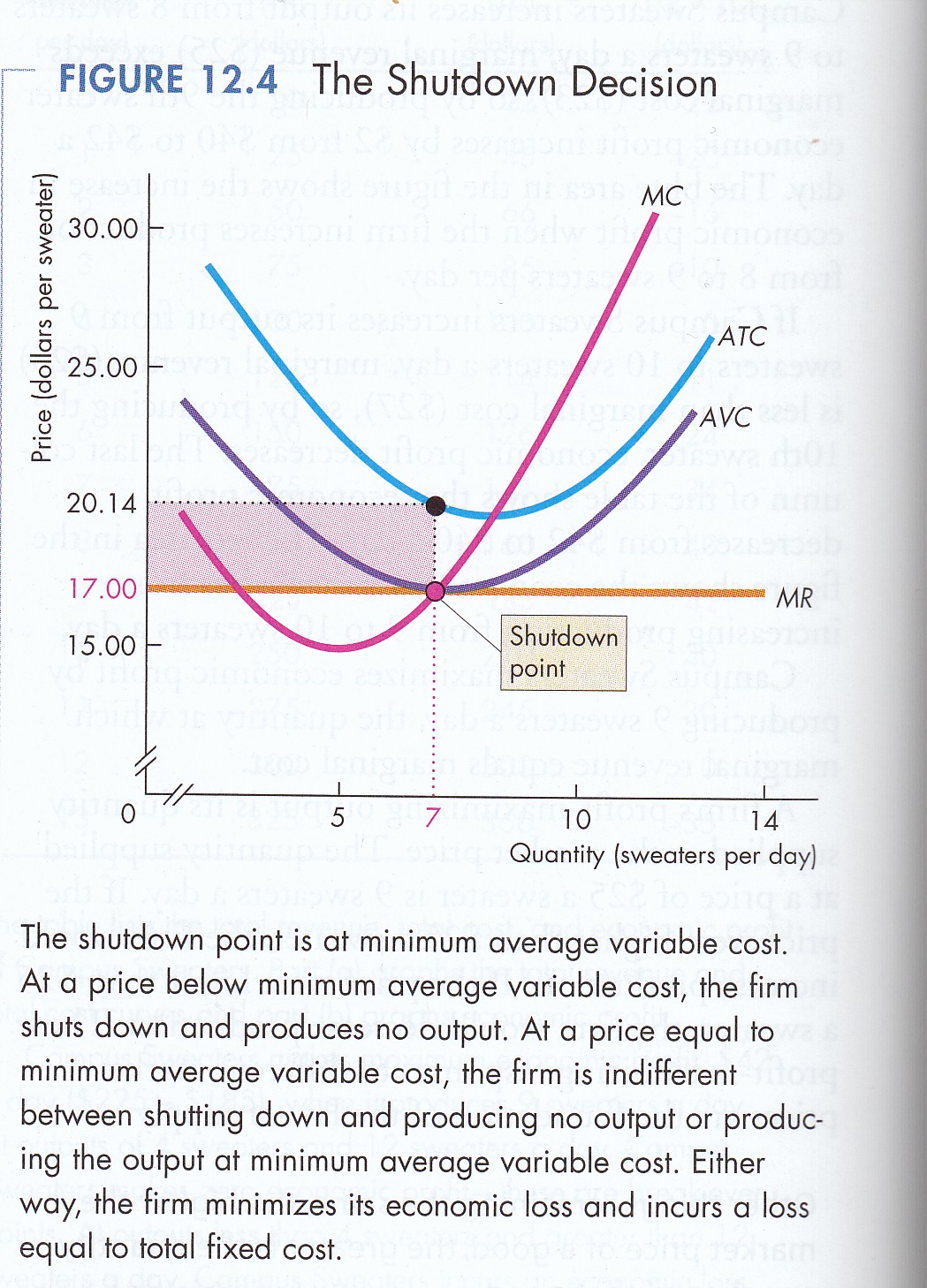

In short-run firm will continue producing if at least all

variable costs are covered even if the firm suffers a loss

because it is not covering all of its fixed costs. If all

variable cost cannot be covered, the firm will shutdown (P&B 4th

Ed.

Fig. 12.5;

5th Ed. Fig. 11.5;

7th Ed Fig.

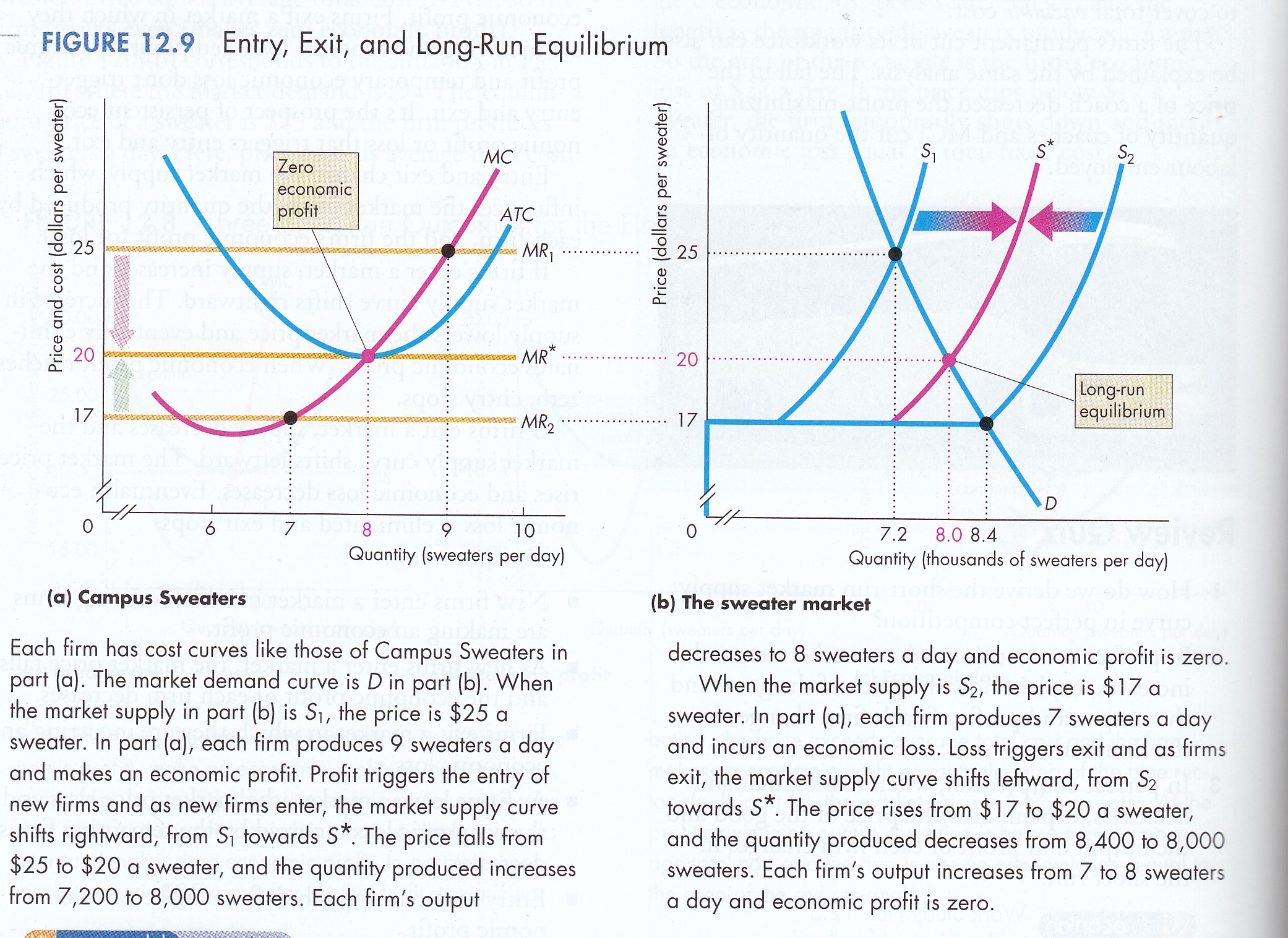

12.4). In the LR, firms suffering short-run

losses either adjust their scale of production (assuming

economies of scale are available) or they exit the industry.

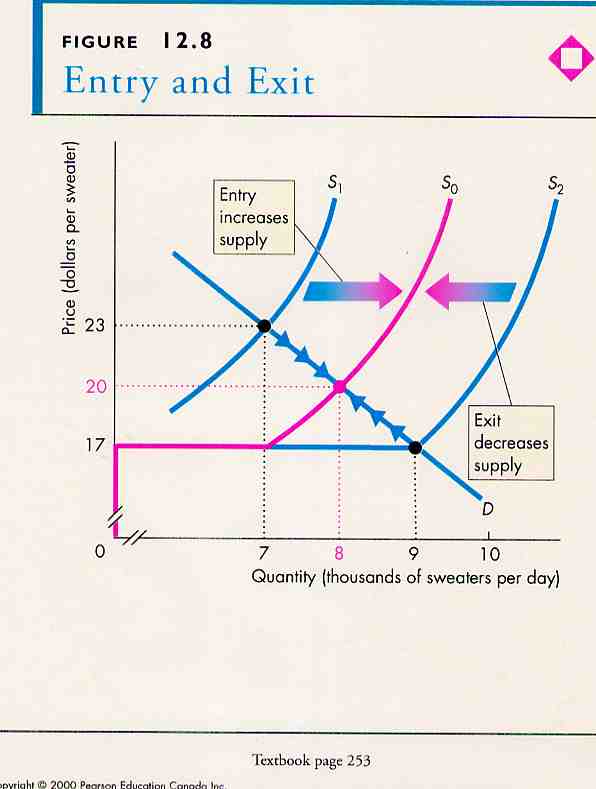

Exit reduces supply (shifts SC to left) and raises price (R&L

13th Ed

Fig. 9-10).

The LRAC curve is the envelop of minimum points of sequence of

SRACs reflecting scale increases.

If some firms enjoy SR economic profits, new firms will enter

increasing supply (shifting SC to right) and reducing price (P&B

4th Ed.

Fig. 12.8;

5th Ed. Fig. 11.8;

7th Ed Fig.

12.9; R&L 13th Ed

Fig. 9-9).

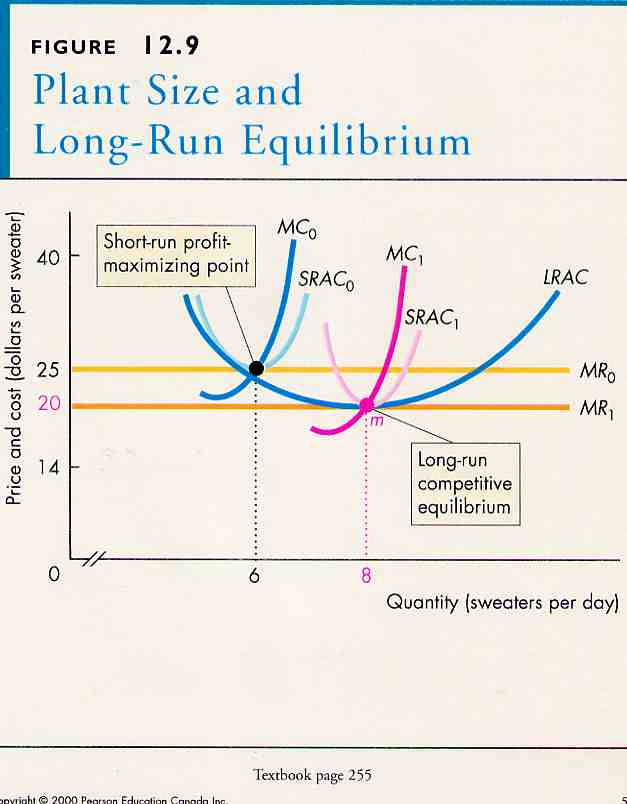

In the long-run, firms can adjust the size of their plants

creating a series of short-run average and marginal cost

curves. The long-run average cost curve is made up of an

envelope of the minimum points of the short-run average cost

curves where SR average cost equals SR marginal cost. At some

point the most efficient plant size is achieved where LR average

cost is lowest for a particular short-run situation. At this

size the short-run marginal cost curves, in effect, becomes, the

long-run marginal cost curve (P&B 4th Ed.

Fig. 12.9;

5th Ed. 11.9; 7th Ed not displayed; R&L 13th Ed

Fig. 9-12).

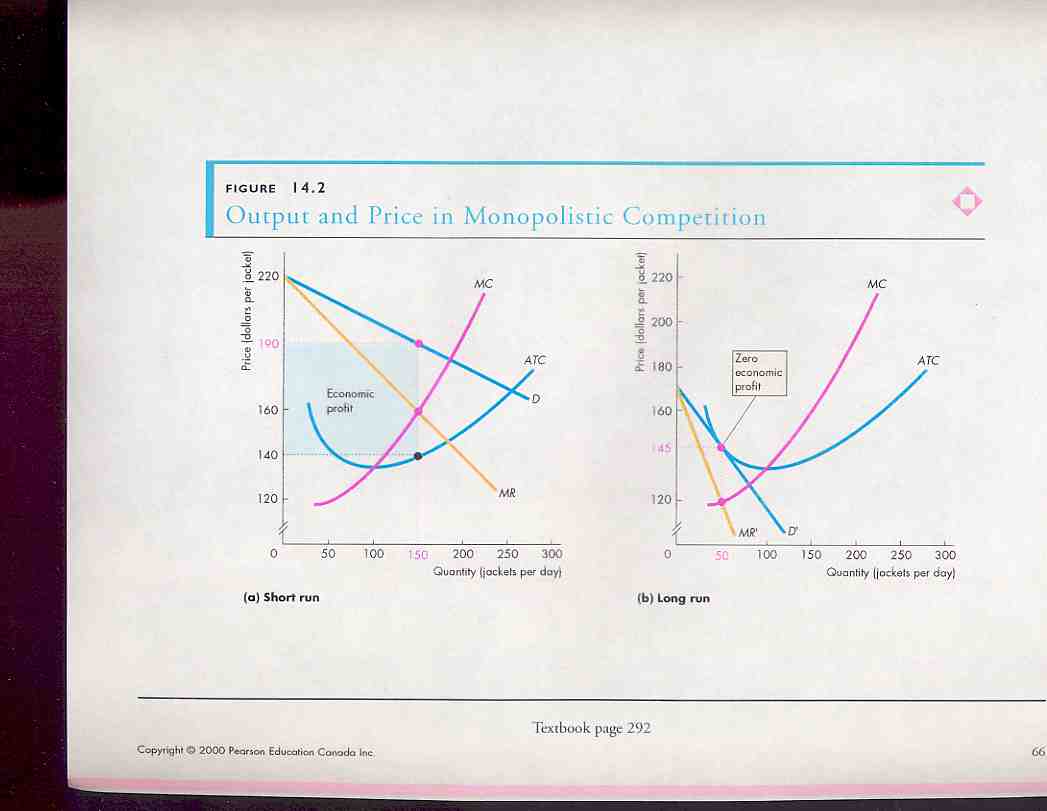

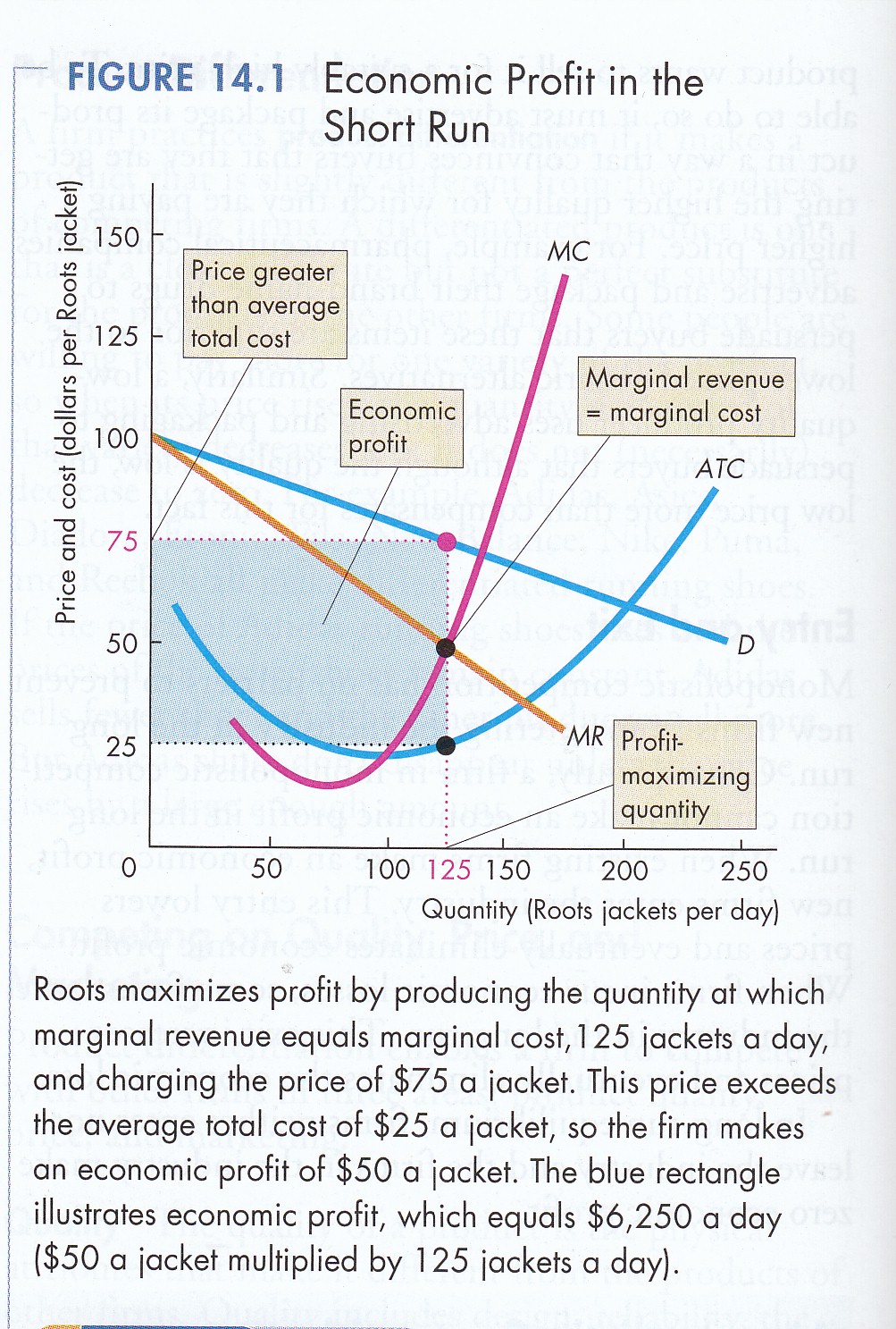

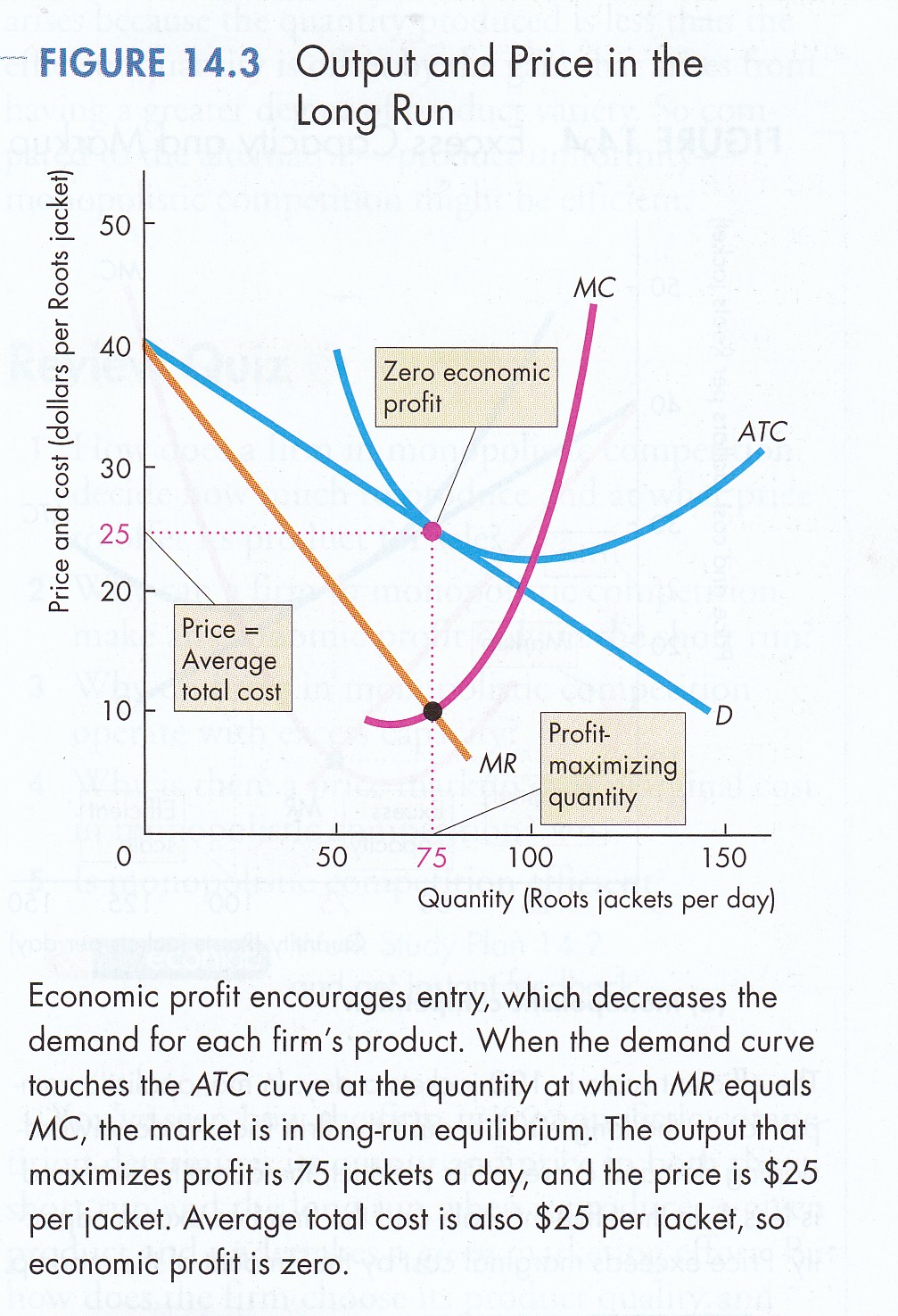

Monopolistic Competition

Given that each firm’s product is slightly

different it faces a negatively sloped demand curve or rather a

‘market niche’. In effect, the industry demand curve is

disaggregated into market segments. The position of the demand

curve depends, however, on the price of other firm’s output.

Thus an increase in the prices of rivals will shift the firm’s

demand curve up to the right; a decrease would cause a shift to

the left. In the short-run equilibrium will be reached where

marginal cost equals marginal revenue, i.e. profit

maximizing. In the long-run, however, firms are able to change

the scale of product and enter or leave the industry. Therefore

long-run equilibrium is reached where long-run average cost is

tangent to the demand curve and where marginal cost is equal to

marginal revenue, i.e., firms are maximizing profits.

But because price is equal to average cost, economic profits

are zero. At this point there is no incentive to entry and

equilibrium is established (P&B 4th Ed.

Fig. 14.2; 5th

Ed. Fig. 13.2; 7th Ed

Fig. 14.1 &

Fig. 14.3; R&L

13th Ed

Fig. 11-2).

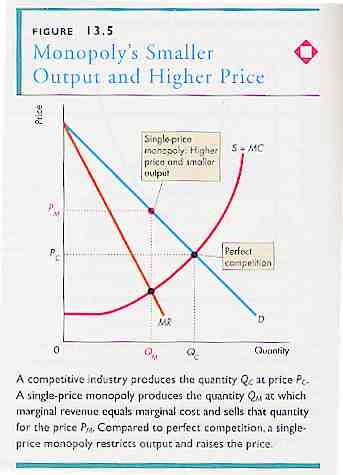

Monopoly/Monopsony

The monopolist faces the same demand curve as the industry. As

in perfect competition, the market demand curve is constructed

from the horizontal summation of individual consumer demand

curves and is usually negatively sloped, i.e. if price

goes up, demand goes down. In perfect competition, however, if

the market price (over which the perfect competitor has no

control facing a horizontal demand curve) goes up the quantity

supplied by firms will increase. In monopoly, however, an

increase in price will cause a decrease in the quantity supplied

by the monopolist. Thus unlike the perfect competitor, a

monopolist can choose which price to charge and thereby what

quantity will be demanded. The monopolist can thereby charge a

price that supplies a quantity that maximizes profits but cannot

adjust both independently. This can be seen by reference to

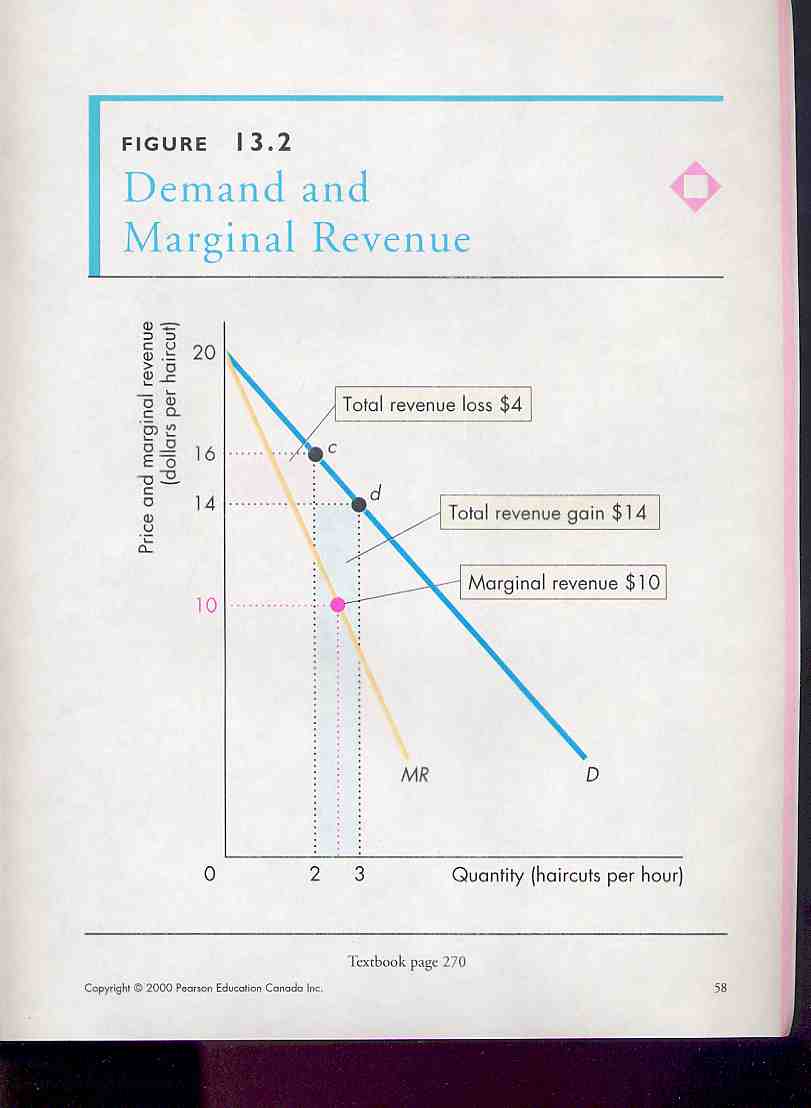

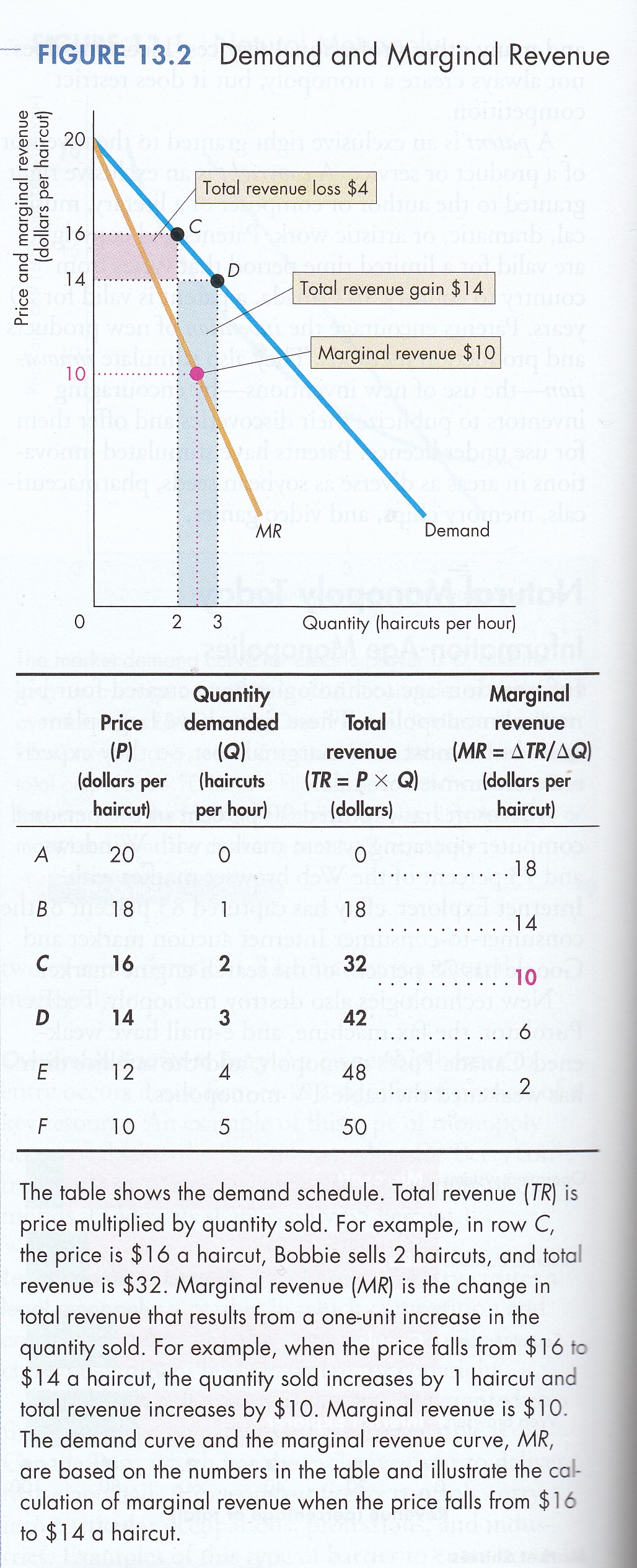

marginal revenue in perfect competition and monopoly: if

·

R = pq

·

MR = dR/dq

·

in perfect competition, the firm is a price taker

at a given market price facing a horizontal demand curve and

therefore MR = p

·

in monopoly facing a negatively sloping demand

curve, the firm is a price setter and MR does not = p because an

additional unit of q can only be sold at a lower price (P&B 4th

Ed

Fig. 13.2;

5th Ed Fig. 12.2;

7th Ed Fig.

13.2; R&L 13th Ed

Fig. 10-1)

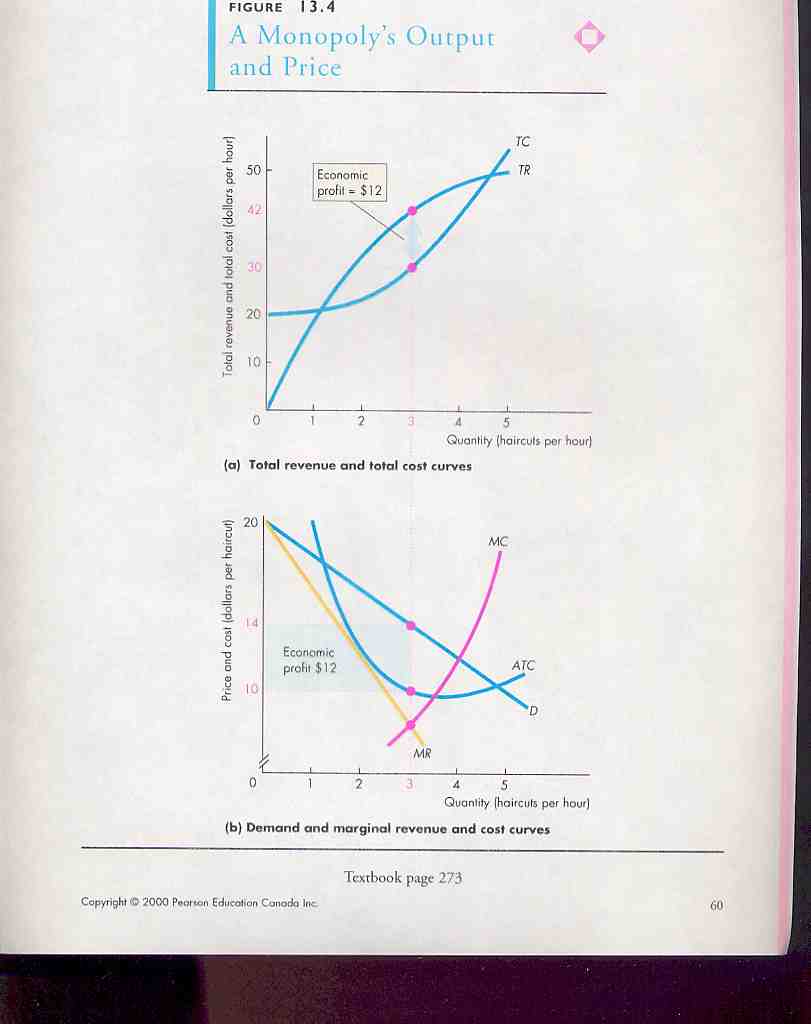

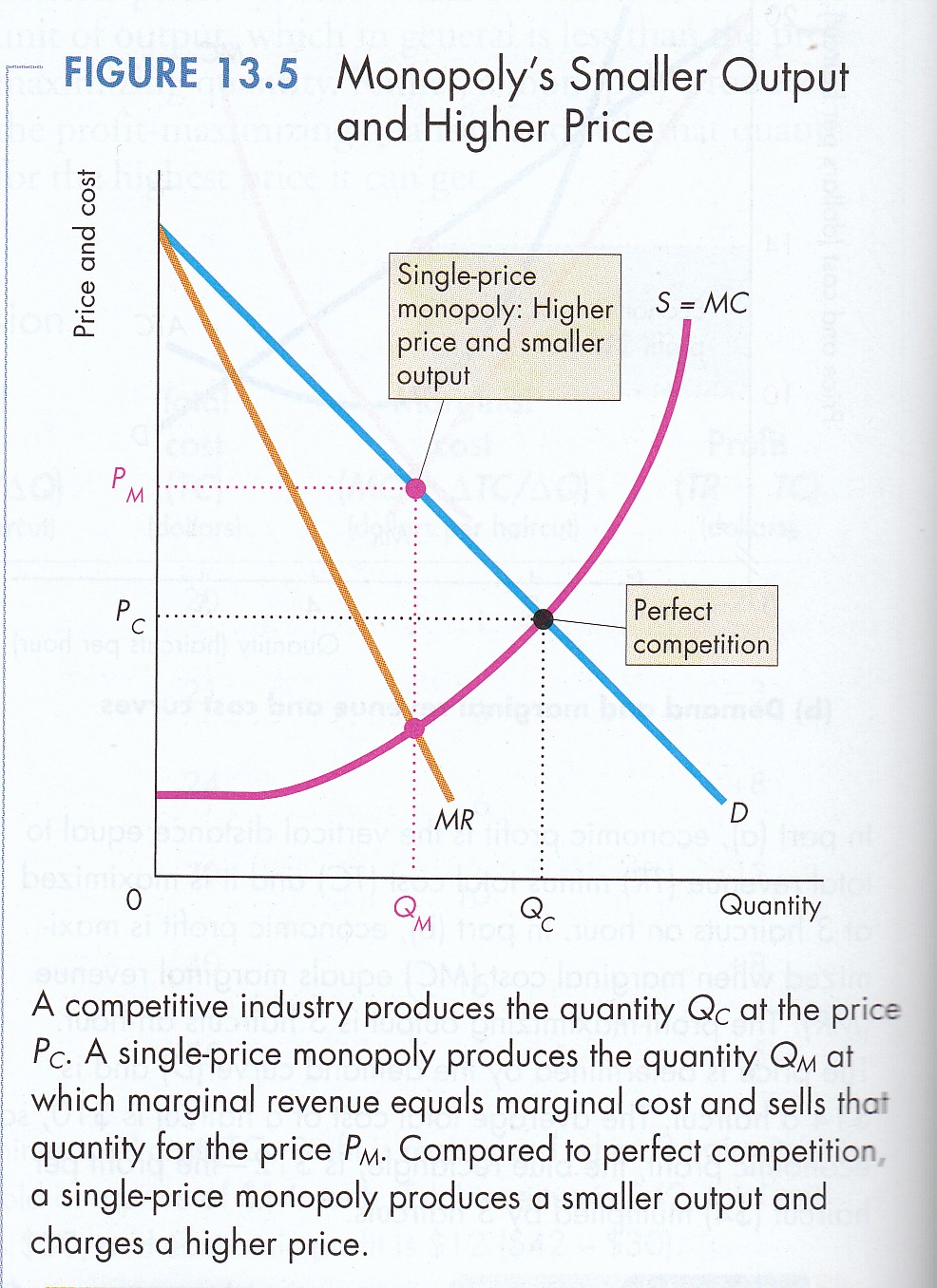

(i) Short-Run Equilibrium

If free from outside interference a monopolist will choose the

price/quantity relationship where the difference between total

revenue and total cost is at a maximum, i.e. maximum

profits. In perfect competition, the maximizing firm will

equate price to marginal cost to maximize profit and the supply

curve is derived from these points. Under monopoly, maximum

profit is obtained when output is at the point where marginal

revenue equals marginal cost. Thus at any output where marginal

revenue exceeds marginal cost, total or accumulated profits can

be increased by more output. When marginal cost exceeds

marginal revenue, accumulated profits decline and can only be

increased by reducing output (P&B 4th Ed.

Fig. 13.4;

5th Ed Fig. 12.4;

7th Ed Fig.

13.4; R&L 13th Ed

Fig. 10.2).

In perfect competition a unique relationship exists between the

price and the output supplied. In monopoly there is not a

unique relationship. This is because variation in marginal

revenue of the monopolist caused by a shift in demand can result

in a different output level but at the same price.

(ii) Long-Run Equilibrium

In perfect competition there can be no long-run economic profits

or losses because firms will enter or leave the market. In

monopoly, there are no long-run competitors unless the industry

ceases to be a monopoly - by definition. Thus long-run

equilibrium in a monopoly will be characterized by economic

profits. If, on the other hand, a monopoly experiences

short-run losses it will adjust the scale and characteristic of

its plant to eliminate such losses in the long-run. If this is

not possible the monopolist will leave the industry.

Assuming short-run profits, in the long-run the monopolist will

adjust its plant to achieve even larger profits. Output will be

provided at the level at which long-run marginal cost equals

long-run marginal revenue.

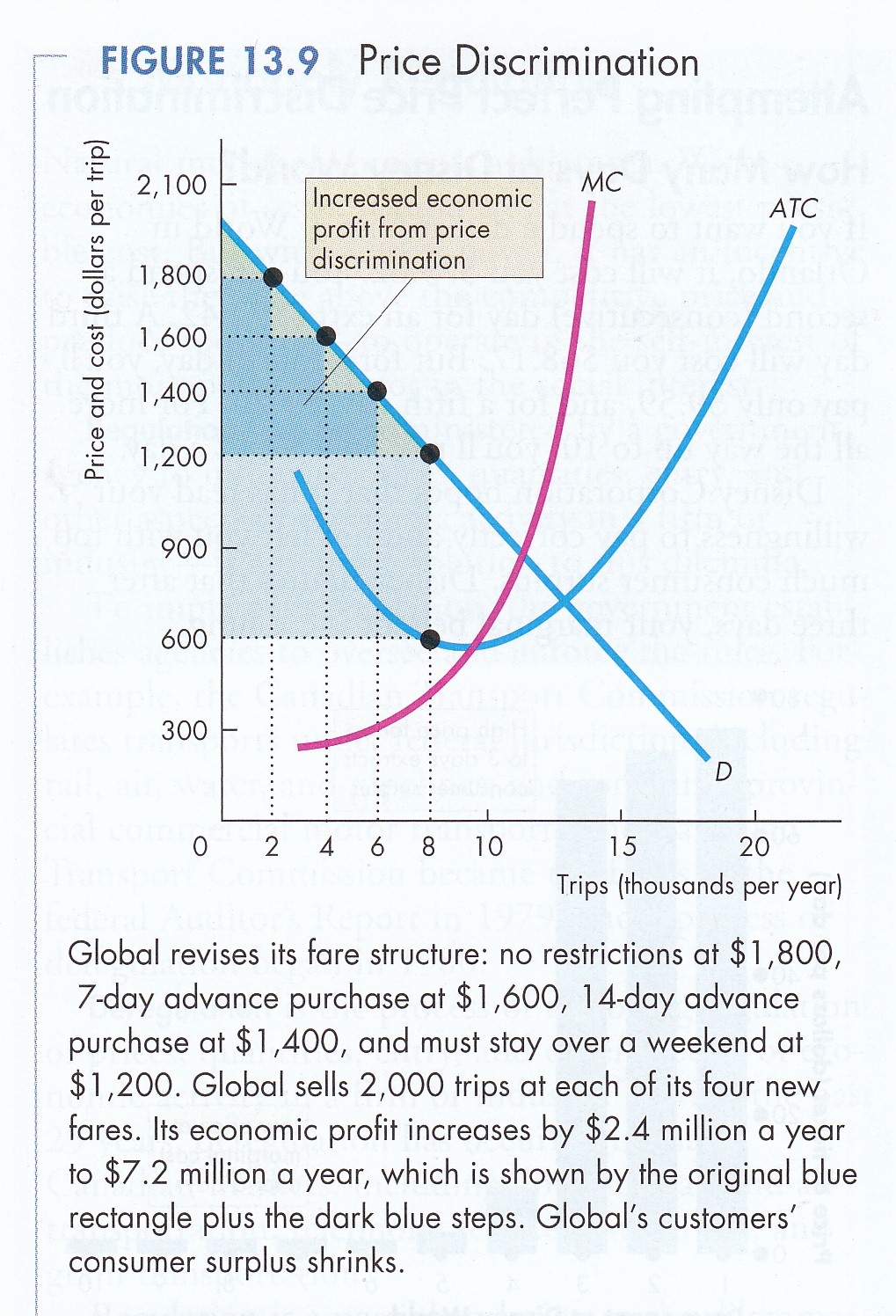

The most profitable form of monopoly is the price discriminating

monopolist who, in effect, is able to disaggregate the market

demand curve into individual consumer demand curves and charge

each consumer a price that maximizes profit on each sale (P&B

7th Ed Fig.

13.9; R&L 13th Ed

Fig. 10-6).

Classic example is the town doctor who charges the farmer a

chicken or sheep for a broken leg but charges the town banker a

much higher price for the same service

Oligopoly/Oligopsony

In perfect competition and monopoly there exists a determinant

solution to a firm’s price and output decision-making. When

there are only a few sellers, however, each firm recognizes that

its best choice depends on choices made by rivals. There are

dozens of alternative oligopoly pricing theories and some

economists claim there is no determinant solution. In an

oligopolistic market there is usually price stability because of

the interdependence of sellers. Interdependence results in

‘game playing’ behavior whereby suppliers act like players in a

game acting and reacting to the moves of their competitors.

Competition tends to take place on a secondary level of:

product differentiation; technological innovation; and,

diversification, i.e. producing more than one commodity.

In theory, oligopoly is considered inefficient because price is

higher and quantity lower than under perfect competition.

(i) Cournot Solution

The Cournot Solution proposes that firms choose an output that

will maximize profits assuming the output of rivals is fixed.

The solution concludes that there is a determinant and stable

price-quantity equilibrium that varies according to the number

of sellers. In effect each firm makes assumptions about its

rival’s output that are tested in the market. Adjustment or

reaction follows reaction until each firm successfully guesses

the correct output of its rivals.

A much more sophisticated and complex solution known as the ‘Nash-Cournot’

equilibrium was proposed by

John Forbes

Nash, the protagonist of the movie ‘A

Beautiful Mind’.

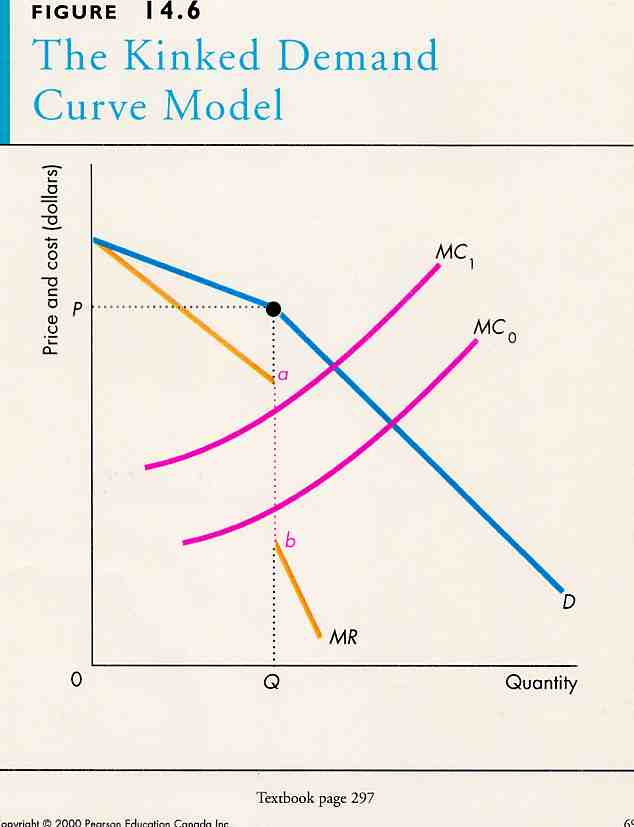

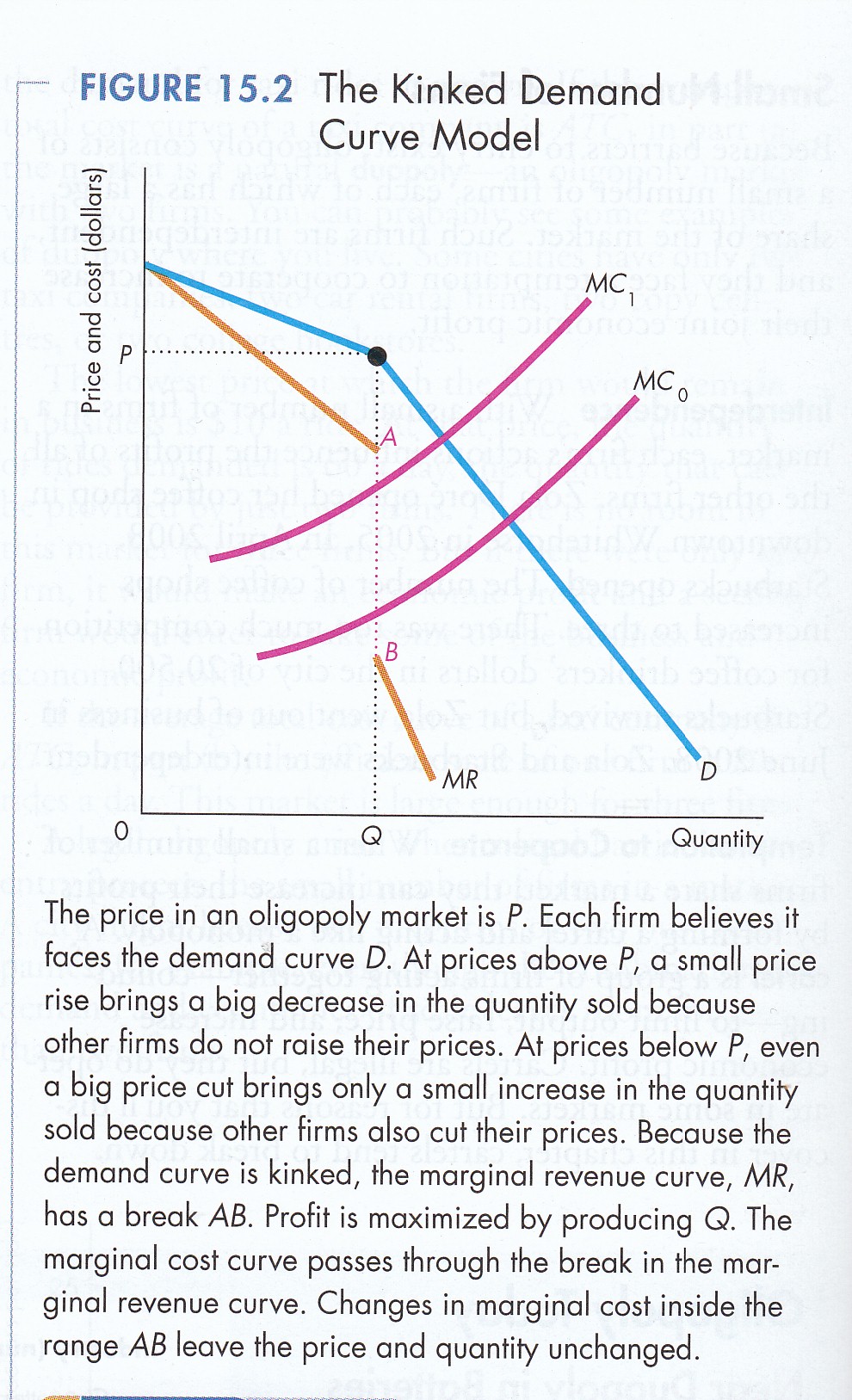

(ii)) Sweezy

Kinked Demand Curve Solution

The Sweezy solution postulates that oligopolists face two subjectively

determined demand curves that assume:

·

rivals will maintain their prices; and,

·

rivals will exactly match any price change.

A key assumption is that rivals will choose the alternative

least favorably to the initiator. If initiator raises p, rivals

will not follow; if lowers price everyone follows. The result is

p will be relative rigid in the face of moderate changes in cost

or demand (P&B 4th Ed.

Fig. 14.6;

5th Ed. Fig. 13.6;

7th Ed Fig.

15.2; R&L 13th Ed not displayed).

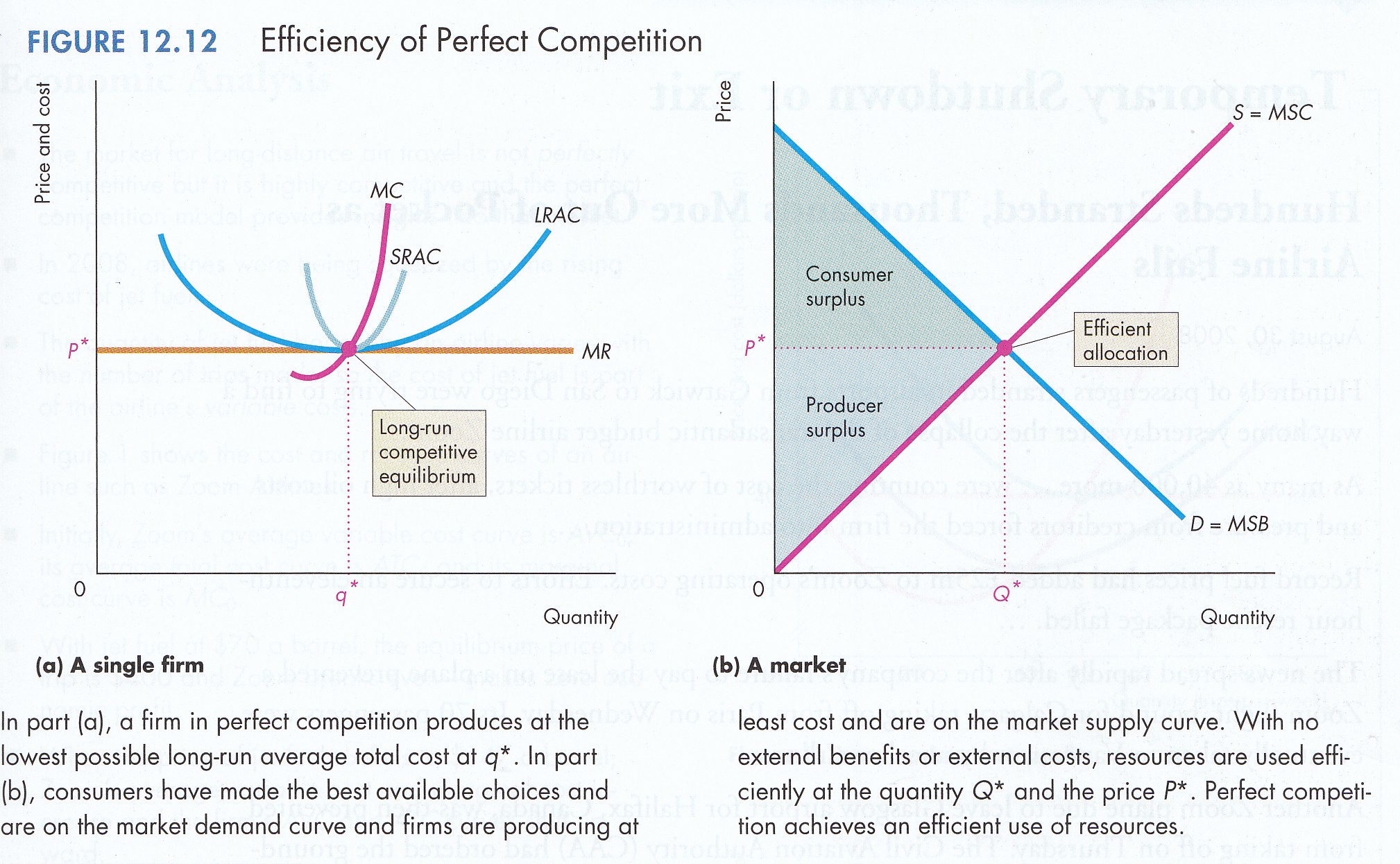

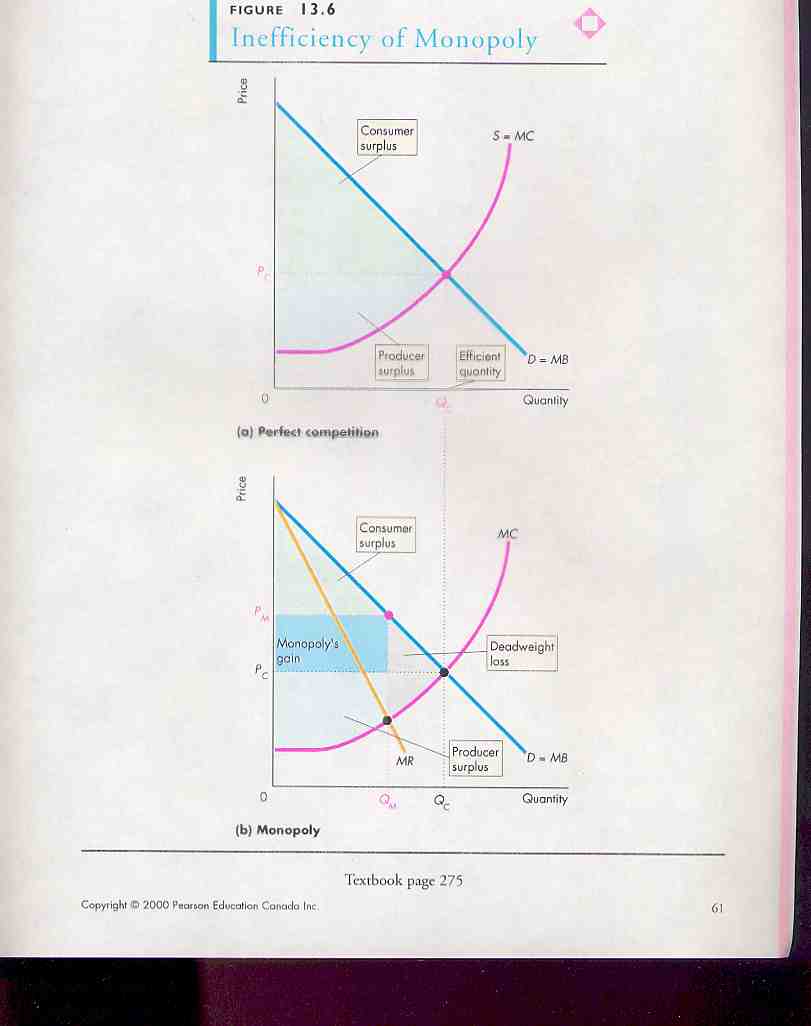

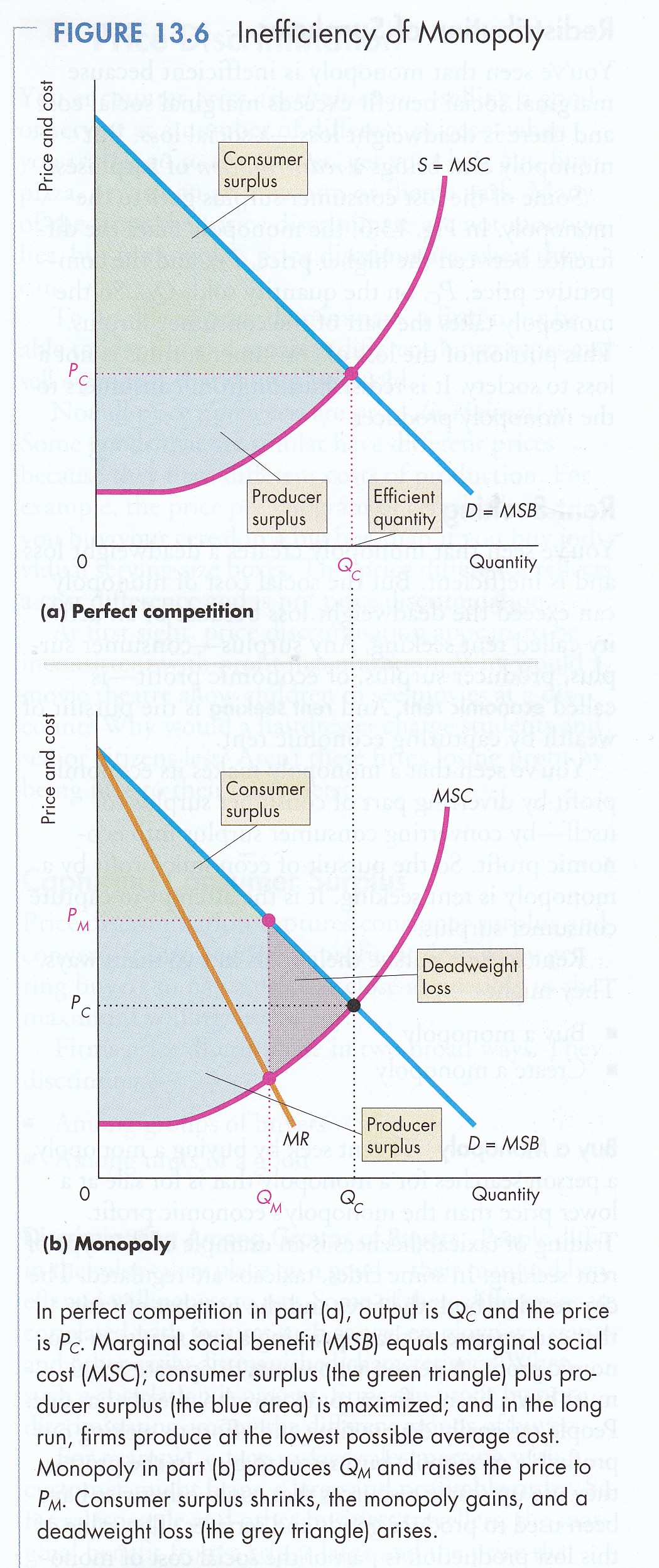

Perfect Competition vs.

Imperfect Competition

First, under perfect competition, each firm

operates at the point where long-run and short-run average costs

are at a minimum. Under all forms of imperfect competition,

however, the firm will operate at minimum average cost but not

at its long-run minimum.

Second, under perfect competition output

tends to larger and price lower (P = MC) than under imperfect

competition (MR = MC). This results in the ‘dead weight loss’

of imperfect competition which reflects the fact that the

consumer surplus is reduced but the gain to the firm is less

than the loss to consumers (P&B 4th Ed. Fig.’s

13.5 &

13.6; 5th Ed.

Fig.’s 12.5 & 12.6; 7th Ed

Fig. 13.5 &

Fig 13.6; R&L

13th Ed

Fig. 10-3).

4.2

Competitiveness/Fitness/Sustainability

There is no doubt

that competitiveness results from the division and

specialization of labour in a larger market. But

competitiveness as comparative advantage has its limits. In

sports, the preferred metaphor used in discussing

competitiveness, it is the opposing team that is the challenge.

The playing field, the environment itself, is generally fixed,

invariant and subsidiary to the consciousness of players at

play. In biology, however, natural selection involves not just

an opponent but also an ever changing environment or ‘fitness

landscape’.

Given an active

environment, autonomous agents, organisms or institutions,

constantly adapt, adjust and evolve or go extinct. They adapt

by experimenting with mutations called preadaptations or

exaptations. According to Kauffman, these come from the

adjacent possible - the realm where possibilities one step away

from being realized reside. Creativity, inventiveness and

imagination are required to see them and courage and confidence

to grasp them.

New products and

processes generated by R&D in the Natural & Engineering

Sciences; new methods emerging from the Humanities & Social

Sciences including management sciences; and, new aesthetics,

forms and designs thrown up by the Arts, this is creative

destruction. Biological systems expand or explore the adjacent

possible filling all possible niches as quickly as possible

subject to timely selection of the fit and unfit, e.g.,

going out of business. Such timely selection is called ‘early

visibility’ and ‘fast failing’ in the innovation literature.

If selection takes

too long, then fitness may decline or simply melt away.

Arguably, this explains ‘de-industrialization’ of Anglosphere

Nation-States. They maintained existing plant and equipment,

e.g., in steel production, until fully depreciated through

voluntary (and sometimes involuntary) quotas on imports from

developing Asian producers who invested in the best new

technologies emerging from the adjacent possible. The fitness of

the West fell, at least in terms of the traditional

manufacturing-based economy. A balance must be struck between

fitness defined as the ability to adapt to a changing

environment and competitiveness defined as optimal adaptation to

the current environment. This balance includes conserving and

preserving the best of the Past. More dramatically it means

maintaining some minimum domestic capacity in case of

interruption to international trade, e.g., caused by a

deadly world flu pandemic. For 3 to 6 months international

shipping may stop. Competitiveness means being the best in the

current environment. Fitness means surviving environmental

change. Sustainability means staying fit through time.

‘Sustainability’

is a term with many meanings to many people. It can mean

sustaining our current life style and/or standard of living into

the future. This is analogous to the long-run outcome of

perfect competition in economics - the steady state. It is an

equilibrium end state. It can mean curtailing our current

standard of living to ensure future generations have resources

available to sustain their needs into their future. It can

mean curtailing our current standards in order to sustain the

remaining ‘natural’ environment and other species. Such

curtailment, to be effective, would, however, require what

futurists of the 1970 called ‘the spontaneous dawning of

awareness’ by virtually the entire human population. It can

also, as suggested in the

Bruntland Report,

simply mean

meeting the needs of the present without compromising the

future. This last definition sounds like Bain’s definition of

economic conservation - wise use (See

4.3

Conservation & Present Value).

4.3 Conservation, Present Value & the Precautionary Principle

As benefits and costs extend out into

the future they become ever more uncertain. One calculates their

current worth – their present value - using a discount rate. The

higher the rate, the lower the present value of future benefits

or costs. Determining the appropriate discount rate is critical

to properly valuing future costs and benefits. There is,

however, also plain ignorance (lack of knowledge) concerning

many future values as explain by

Keynes.

With respect to public intervention

or production of public goods there is, however, an added

dimension to present value – politics. While future benefits or

costs may be significant they are politically discounted to

maximize election and re-election of politicians and

governments. Three examples demonstrate. First, with an

aging electorate politicians are more concerned with present

older voters than with future generations. Quite simply future

generations are not politically relevant unless the current

generation says so at the ballot box.

Second,

there is the political ‘edifice complex’. A new $100 million

bridge or building bearing a politician’s name is much more

valuable politically than an annual $20,000 paint job required

to preserve and maintain an existing structure for 100 years.

Arguably the much reported deterioration of public

infrastructure in the United States and Canada reflects this

political discount rate.

Third,

no matter political intentions about the future the reality is

we simply cannot know for certain what future generations will

want, need or desire from us today. This is especially important

when considering questions of sustainability. The concept of

sustainability is roughly analogous to the economic concept of a

‘steady state’ where the existing pattern of economic activity

continues through time. In the view of some economists resources

are highly substitutable or fungible. Technological change will,

in this view, provide a substitute for any resource that is

depleted through current use. Whether or not it is appropriate

to preserve a current resource for future generations thus

becomes a question of substitutability.

A related question is preservation

(non-use) versus conservation (wise use) of a natural resource.

Economist Joe Bain in his classic Industrial Organization

lays out the question:

For any of a group of industries

whose operations involve extraction of natural resources

(mining, petroleum production, agricultural cultivation,

lumbering, commercial fisheries) a significant dimension of the

market performance of the firms engaged involves how well they

do in the matter of “conservation” of resources. To paraphrase

the popular literature on this matter, conservation in an

economic sense of course does not mean non-use or simple

deferment of use, but “wise use” of the resources being

exploited. In technical terms, good conservation requires a

choice of technique of exploitation, time pattern of production,

and time pattern of investments and other costs, which together

yield an optimal net social benefit relative to costs over all

future time periods in which society is interested. In

determining this optimum, distant future benefits and costs

should be appropriately discounted by whatever rate of “time

preference” society wishes to assign in assessing the relative

importance of current as opposed to future benefits and

sacrifices. And conservation performance is poor to the extent

that enterprises deviate from this abstract ideal.

An adequate operational definition of ideal

conservation performance is extremely complex and next to

impossible to apply fully in the evaluation of actual

performance. Using the definition just given as a guide,

however, it is possible to identify certain types of gross

departure from good conservation which would have to be censured

under any acceptable criterion. These include:

1.

Exploitation of resources by a technique that raises both

present and future costs above the obtainable minimum while

reducing or not increasing the amount of resources ultimately

recovered, or the amount of use obtained from resources over

time.

2.

Unduly rapid or intensive current use of resources which has the

result of impairing (or eliminating) future use of the resources

to a degree not compensated by current additions to output.

3.

Pinching on current costs or investments in the use and

development of resources in a way that curtails future use or

raises future costs of use to a disproportionate degree.

What of the actual performance of industries

in regard to conservation? Of course, only a minor proportion of

all industries are sufficiently involved in extraction to make

conservation an issue, and for these we do not have highly

organized, systematic information on which to base an overall

appraisal. However, a broad scattering of evidence on individual

cases suggests that, among extractive industries, conservation

performance is or has very frequently been poor.

Thus we observe in petroleum production in

the United States a history of gross elevation of recovery costs

coupled with a substantial reduction of ultimate recovery of

available petroleum, attributable largely to the selection of

techniques in the context of competitive exploitation of

individual oil pools by antagonistic interests. In both

lumbering and commercial fisheries, and in some agriculture, we

find that a serious long-run depletion of resource productivity

has resulted from overintensive immediate rates of extraction or

exploitation of the available resources. In much of agriculture,

a history of pinching on current costs for or investments in the

preservation of the land (against erosion or reduction in

fertility) has resulted in long-run losses in soil productivity.

These deviations from reasonably good

conservation performance seem in large part attributable to four

things: (1) antagonistic exploitation of resource deposits by

competing interests, in which a competitive race to capture the

resource or its output before others do results in a disregard

of long-run yield considerations; (2) an inherent

“short-sightedness” of firms engaged in exploiting resources -

firms that attach much less importance to distant future

production than society would, or than they do to immediate

profits; (3) competitive conditions which bring about such low

returns to firms in some extractive industries that they cannot

afford to invest in the long-run maintenance of resource yields;

and (4) stupidity. Whatever the cause, poor market performance

in the matter of conservation has evidently been chargeable

against firms in many extractive industries. It is encouraging,

in the light of this, that in the past twenty or thirty years

there has been a rapidly increasing body of governmental

regulations designed to encourage or require better conservation

performance on the part of these industries.

Bain 1968, 425-427

Cost-benefit analysis involves

calculation of the probability and magnitude of costs and

benefits associated with a new technology, public intervention

in the market place or production of public goods and services.

If probable benefits outweigh probable costs it is approved; if

not it is rejected.

Applying the ‘precautionary

principle’, however, means that if a new initiative has any

chance of generating irreversible harm, no matter its short-term

benefits, it is rejected in spite of any positive cost-benefit

ratio. In fact, the precautionary principle is both an economic

and moral criterion. It invokes a social responsibility to

protect the public from harm if scientific investigation finds a

plausible risk. In the Rio Convention and in the European

Union, the precautionary principle has been made into a

statutory requirement. Its application is most apparent with

respect to genetically modified foods. In the Anglosphere

cost-benefit analysis has consistently found them to be a good

investment. In most cases natural and genetically modified crops

and animals are treated as equally safe. In the European Union,

however, the remote possibility of irreversible harm to human

health or the environment has led to significant restrictions on

the use of genetically modified foods including labeling of all

products. Some observers argue that this ‘plant protection

racket’ is fuelled by a Veblen Effect, named after economist

Thorstein

Veblen

who introduced the concept of ‘conspicuous consumption’.

Please see: my

Environmental, Natural Resource & Ecological Economics -

non-testable.

4.4

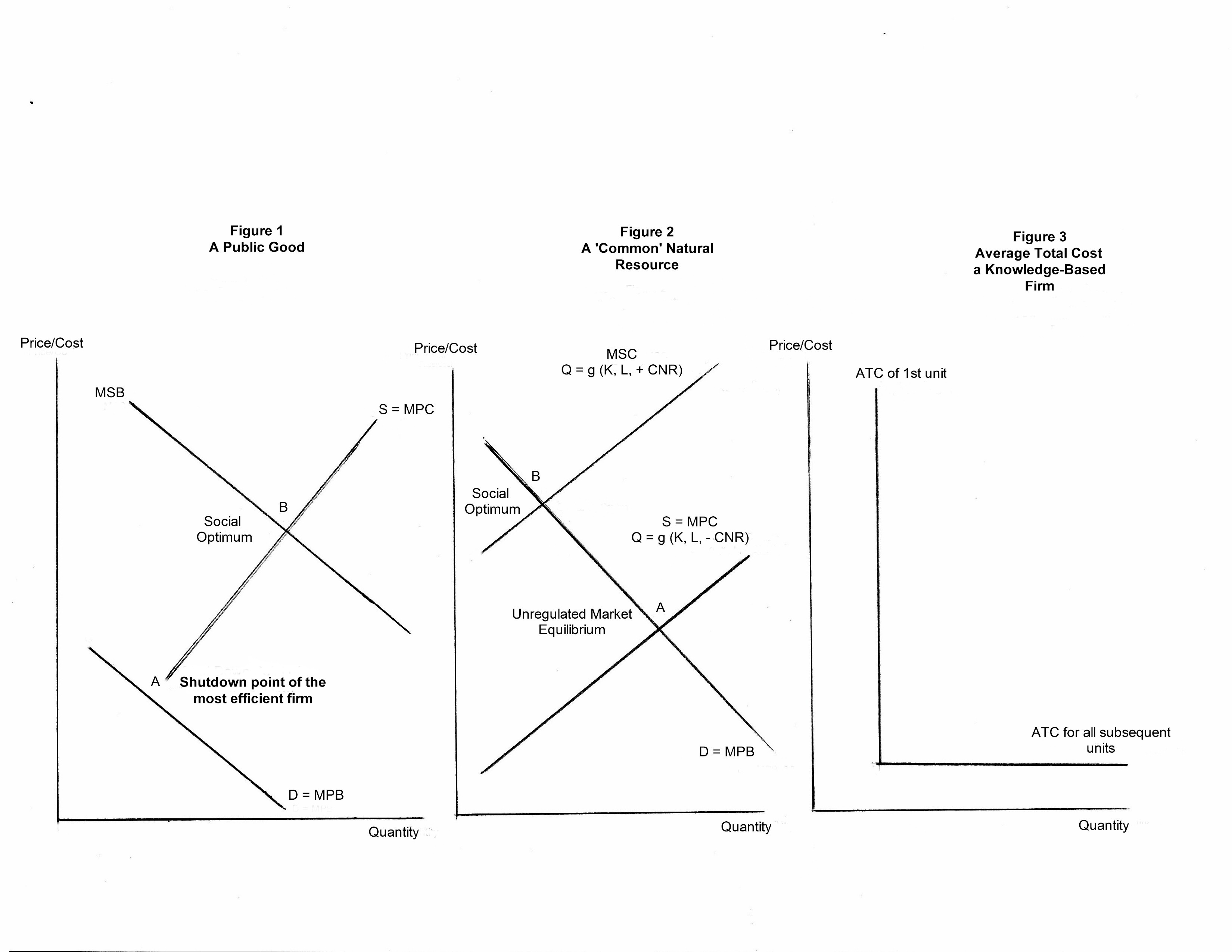

Externalities & Public Goods

Until now we have assumed that

market price includes or ‘internalizes’ all relevant costs and

benefits. This means the consumer captures all benefits and the

producer pays all the costs. An externality refers to costs and

benefits that are not captured by market price for whatever

reasons, i.e., they are external to market price.

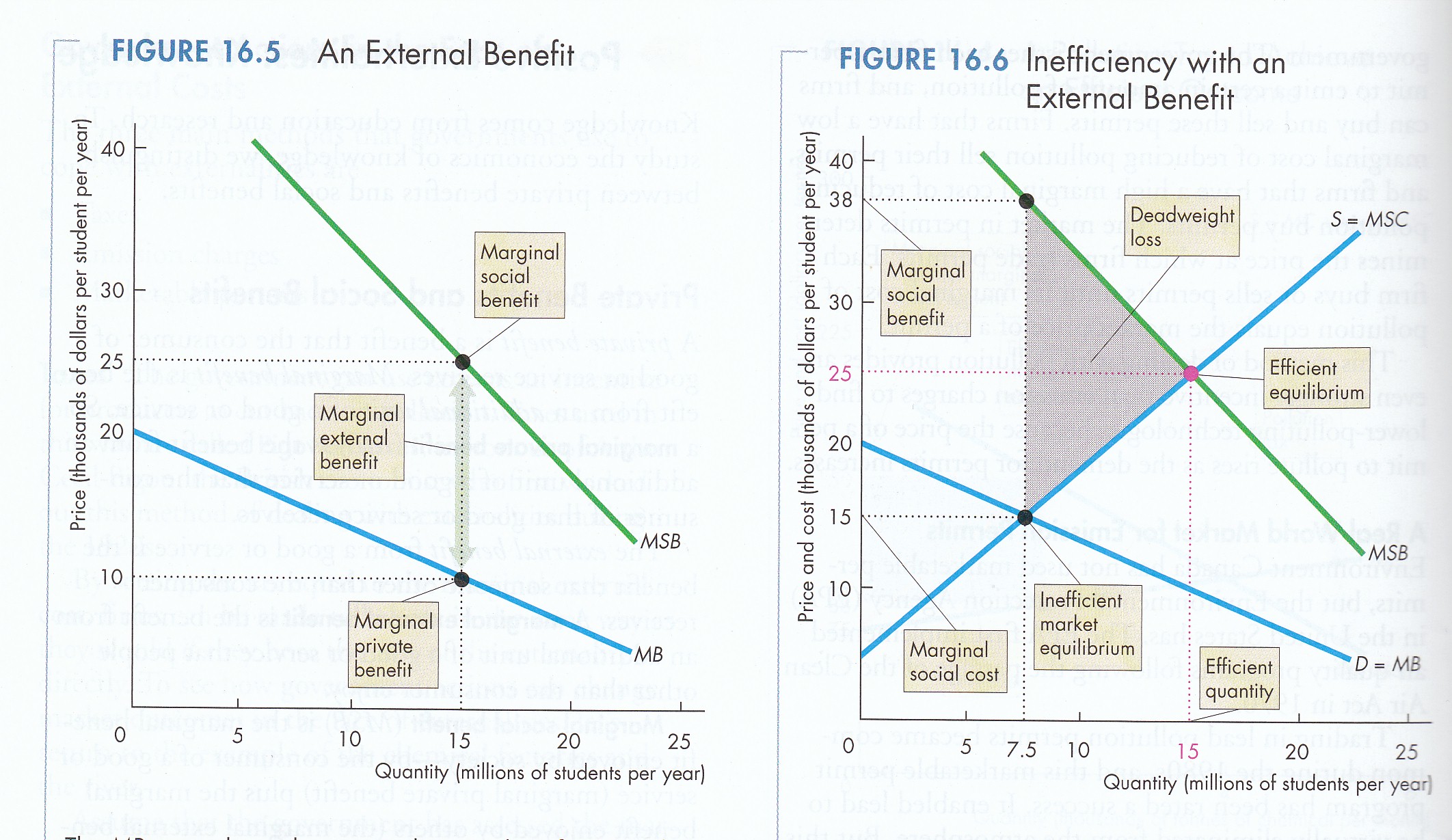

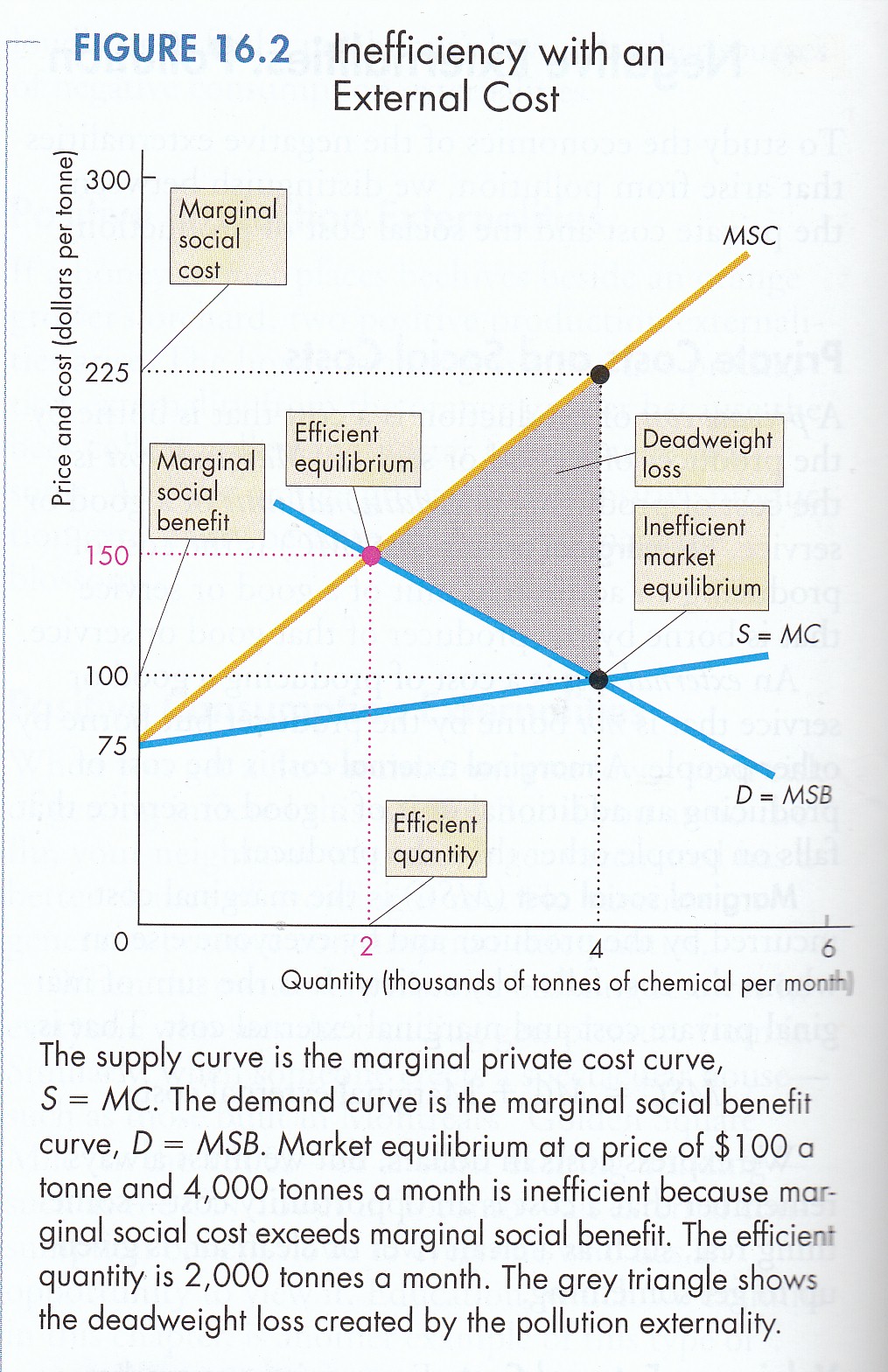

In effect, the market demand

curve reflects only

marginal private benefits

(MPB) (R&L 13th

16-1) of consumers but not the external benefits accruing to

society. When such external benefits are added, vertically, we

derive the

marginal social benefit curve

(MSB) inclusive of both private and public benefits.

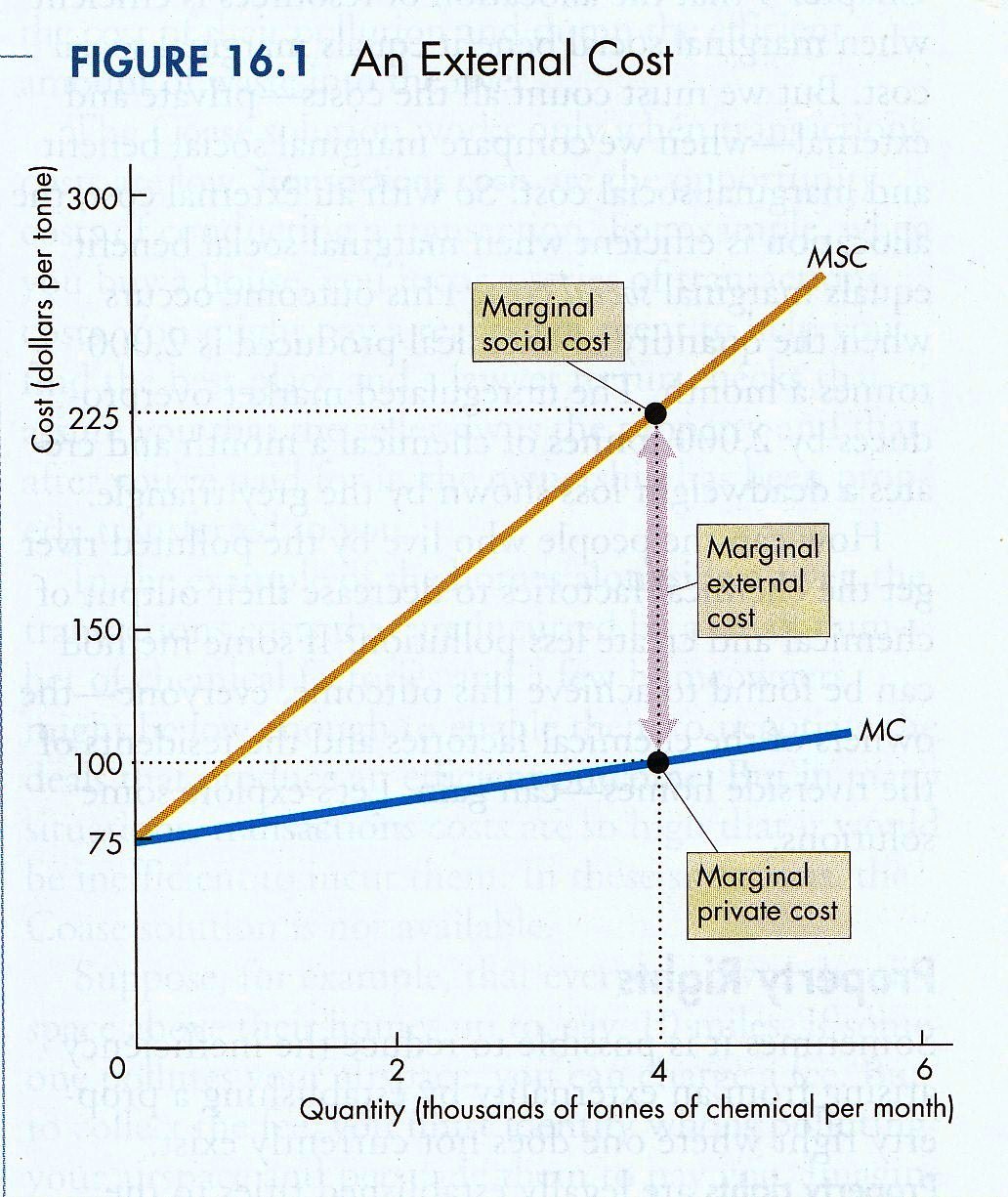

Similarly, the market supply

curve reflects only

marginal private costs

(MPC) but not costs external to the firm’s accounting, e.g.,

pollution that society must pay. When social costs are added,

vertically, to the supply curve we derive the

marginal social cost

(MSC) curve inclusive of both private and public costs.

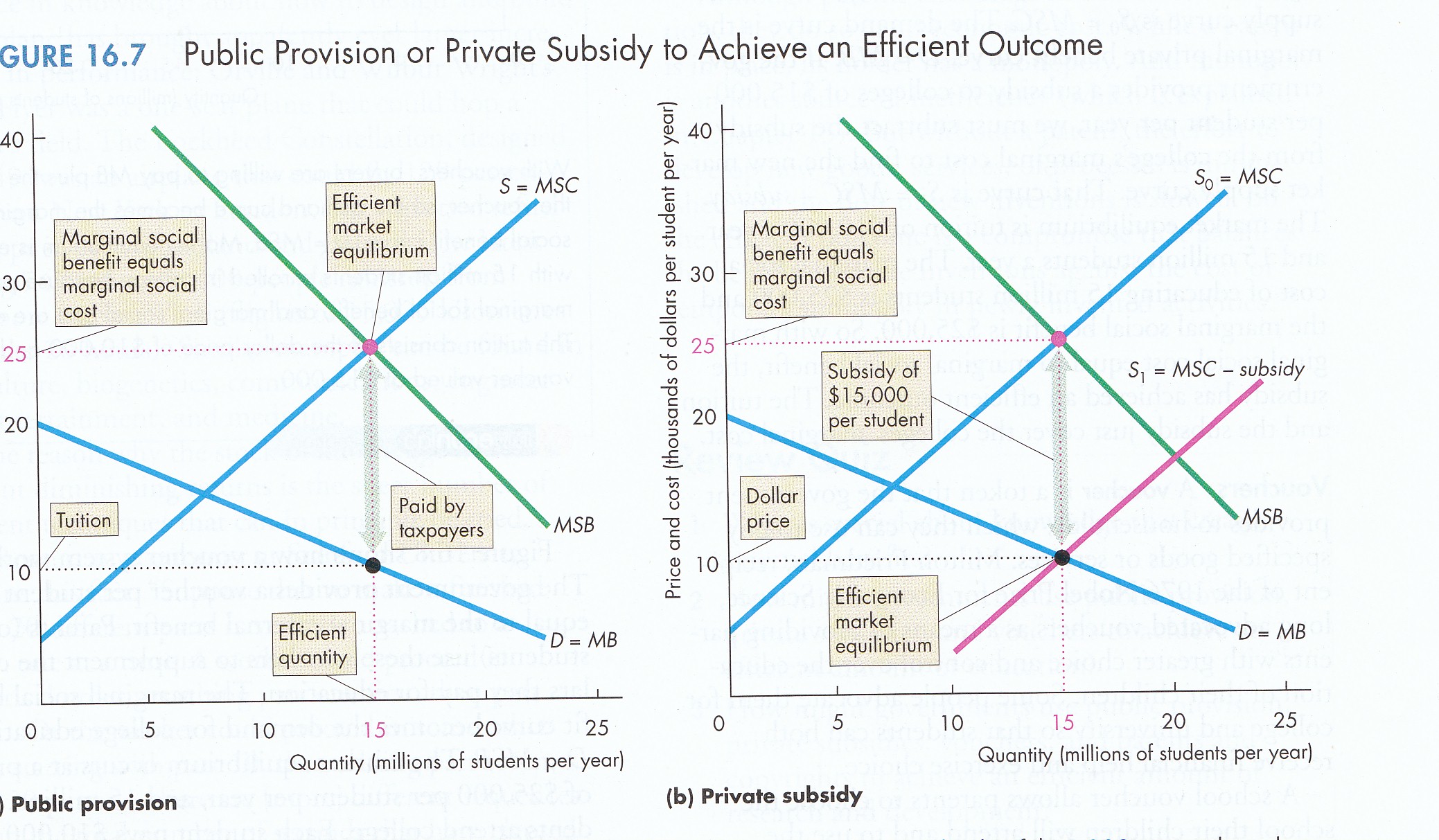

The standard model of market

economics is thus based on the assumption that all relevant

costs and benefits are internalized in market price, i.e.,

there are no externalities. If this assumption holds then ‘X’

marks the spot. If, however, there are externalities then market

equilibrium must be adjusted (R&L

17-1,

17-2,

17-3,

17-4,

17-5,

17-6,

17-7). External or social costs and

benefits must be added to private costs and benefits reflected

in the market supply and/or demand curves. The point is that

such external costs must be paid and external benefits accounted

for if the appropriate price/quantity equilibrium is to be

established. The agency to do so is not the market but rather

government. Put another way, the market ‘X’ solution is

superseded by a social ‘X” marking the spot and it is up to

government to correct the miscalculation of private agents to

generate

a new socially optimal equilibrium.

This is a controversial view. It is expressed in the tradition

of both welfare economics (a sub-discipline) and the Keynesian

view.

On the other side are those arguably

including the Austrian school of economics - von Hayek and von

Mises being leading protagonists - who argue: Let the market do

it! If consumers are willing to pay then providers will be

willing to supply. If a sufficient number are not willing to

pay, for example, because of the ‘free rider’ problem associated

with public goods, to make it profitable to suppliers then there

will be no provision, no market and people will get what they

paid for.

Excludability and

rivalrousness distinguish private from public goods. If I buy a

car I can exclude others from using it by lock and key. I alone

extract its utility. Similarly, if I am driving no one else

can, i.e., driving is rivalrous. Public goods, on the

other hand, are non-rivalrous in consumption, i.e. my

consumption does not reduce the amount available to you. If I

watch a fireworks display it does not reduce the amount

available to you. Similarly, public goods are non-excludable,

i.e. a user cannot be easily prevented from consuming a

public good. This creates the ‘free-rider’ problem. Extending

the fireworks example, while not willing to pay to enter the

stadium I can still watch the display from the balcony of my

apartment at no charge.

Allowing for

externalities (discussed above) there is in fact a spectrum of

goods ranging from pure private to pure public in nature. The

more public a good the less likely it is that private producers

will be willing to supply a socially optimal output and the more

likely that only government will be willing to do so, e.g.,

national defense, the Census or inoculation against infectious

diseases.

The response of the

government to problems presented by public goods varies

according to the nature of the good. Non-market benefits and

costs may be considered sufficiently important to justify public

action. In the case of benefits, such goods are called “merit

goods”. In the case of costs, they are called “demerit” goods.

There are thus times and situations in which a democratic

government decides that the free market is not producing

socially or politically acceptable outcomes and chooses to

override the marketplace.

The modern environmental

movement was born with publication of

Silent Spring

by Rachel Carson in 1962. The 1960s & 1970s were a pre-revolutionary period

characterized by radical new ideas on campus and a general stirring up of

society’s status quo. A materially satisfied and educated middle class,

specifically its younger generation, awoke to a new spectrum of needs.

It appeared to some that material success was paid

for with environmental degradation plus international, racial and gender

inequity. Cities burned; riots and protests plagued campus; presidents fell;

civil, environmental and gender rights became slogans of mass movements. And

into the headlines were propelled pacifism, a.k.a., hippies, Woodstock

and the anti-war/anti-draft movement, as well as extremist groups, e.g.,

the Yippies, Weathermen, Black Panthers, et al.

It was in this context that economics met ecology

with publication in 1967 and 1968 (the year of the Democratic Convention in

Chicago and the down fall of President Johnson together with his dream of a

‘Great Society’) of two very different yet related texts.

In December 1968, Garrett Hardin, a biologist, published

“The

Tragedy of the Commons”. The article was

based on his presidential address to the Pacific Division of the American

Association for the Advancement of Science in June 1968. Hardin demonstrated

that unfettered competition for natural resources within and between countries

was destroying the natural commons, a.k.a., the environment or biosphere

including the air, water, land and biodiversity living therein. Given such

resources belong to everyone yet to no one, i.e., they are ‘public

goods’, competitive self-interest dictates getting for oneself as much as

possible as quickly as possible with no consideration for others – past, present

or future. This is “The

Tragedy of the Commons”. Unfortunately,

a variation on this theme also plagued Second World or communist command

economies resulting in even greater environmental damage, debilitation and

destruction.

If a public good belongs to everyone but to no one then one way to solve

the problem is to assign ownership to someone. That someone will then have a

vested interest to ‘conserve’ the resource. This is the approach taken in the

Conventions on the Law of the Seas and on Biodiversity (CBD) and the Kyoto

Accord. In the case of the Law of the Seas and CBD ownership is vested in the

Nation-State. In the case of Kyoto it is similarly vested in the Nation-State

but some have transferred ownership to private agents – both natural and legal

persons, e.g., using

carbon auctions and even

personal carbon credits.

Public Goods, ;'Common' Natural Resources, Knowledge-Based Industries

4.5 Equity,

Ethics & Moral Sentiments

With respect to Equity in Law we have seen it

is justifies market interventions by government, e.g.,

agriculture, minimum wage and rent control. Arguably it also

applies in cases of market failure where consumer surplus is

appropriated by producers. In the Standard Model of Market

Economics such intervention to approximate the outcome under

perfect competition is also accepted.

With respect to Ethics #8 of the Ten

Humorous Reasons for studying economics reads: Although ethics

teaches that virtue is its own reward, in economics we get

taught that reward is its own virtue

JokEc.

In the Benthamite tradition, however, maximizing pleasure was

restrained by the tenets of Ethical Hedonism, a very Protestant

Ethic. This ethic, beyond concern with the moral value of work,

also involved social inhibitions against conspicuous consumption

(Veblen 1899). Such ethical or moral restrictions were

reinforced by the lingering effects of feudal sumptuary

legislation which made “status forgeries illegal and created the

disincentive of trial and punishment” (McCracken 1988: 33).

However when the Protestant ethic collapsed during the

Industrial Revolution, only hedonism remained -- in all its

unrestrained, irrational incarnations (Bell 1976: 20-22).

Without a generally accepted moral code, the law became the

accepted social institution to moderate individual

pleasure-seeking. Benthamite traditions concerning crime and

punishment in fact continue to guide both the law and economic

research, e.g. Bentham's famous and seemingly plausible

dictum `the more deficient in certainty a punishment is, the

severer it should be' (Becker 1968).

While self-interest or ‘Me-ism’ lays at the heart of the

Standard Model Economics itself is in fact qualified by moral

considerations. Thus while Adam Smith is remembered as the

founder of modern economics with the 1776 publication of his

Inquiry into

the Wealth of Nations some 17 years

earlier in 1759 he published

The Theory of Moral

Sentiments

(1759) providing the

ethical,

philosophical,

psychological,

and

methodological

underpinnings to all his later works. Today such concerns are

summed up in expressions such as ‘market sentiments’. Such

sentiments include, among other things, trust. Overtime buyers

and sellers, producers and suppliers, employers and employees

develop trust reducing what are called transactions costs.

Without such trust every exchange must be carefully and

expensively scrutinized to insure all terms of a contract are

fulfilled by both parties. In times of severe recession, such

as now, relations tend to break down with producers and/or their

suppliers going out of business, employees laid off, etc.

Like a rug or woven sweater relations unravel and if this last

long enough new supplier or new employees must be engaged who,

at the beginning of the relationship, are subject to uncertainty

and a lack of trust raising transaction costs.

The

Benthamite tradition also places limits on what phenomena are

considered legitimate subjects of economic investigation. It

continues to blind mainstream economists to the cultural context

of economic behaviour. Daniel Bell, quoting the author of the

most widely read economics textbook in history observed:

Paul

Samuelson has noted that many economists would “separate

economics from sociology on the basis of rational or irrational

behavior, where these terms are defined in the penumbra of

utility theory.” Utility is defined as egoism, or

self-interest, and rationality is defined as consistency - that

is, preferences are transitive ....

Yet the

crucial question is whether the obverse of the rational is the

irrational rather than the non-rational, and whether or not

non-rational motivations can provide a valid assumption for an

understanding of economic behaviour, i.e. to behavior

which seeks to enhance the wealth and welfare of mankind (Bell

1981: 70-72).

Put

another way, can non-rational motivations provide the foundation

of an inclusive or

catholic

economics to balance the

materialistic, protestant, exclusionary rationality of

contemporary economics? In this regard, Tibor Scitovsky (1972,

1976, 1989) has gone further than anyone in re-tooling economics

to account for `irrational' behaviour, e.g. cultural

activities including the arts. Where Bentham used the

associationist psychology of his, day to define pleasure and

pain as the ultimate principles of behaviour, Scitovsky, after

investigating contemporary clinical psychology, substitutes

`comfort and stimulus'. Among other things he uses this

distinction to differentiate consumption in the United States

(comfort) from what is now the European Union (stimulus). His

model, however, still uses marginal utility (Scitovsky 1989).

His work is in the tradition of welfare economics

From a welfare

economist's perspective, there are two types of social

behavior. The first are onerous activities not performed for

inherent satisfaction but for what they yield, i.e.

work. Thus the disutility of work is theoretically to be

compensated by a pay check. Second, there are activities that

are the opposite of work. They give satisfaction to those

performing them. In turn there are two types of such

activities. The first are antisocial activities that give

pleasure by inflicting pain or suffering on others. Social

costs usually outweigh benefits because benefits are transitory

while suffering is often long lasting or permanent. Third,

there are 'social' activities that impose no physical burden or

harm on anyone yet can give satisfaction or pleasure to all.

They include the most benign and valuable of human activities

such as love, learning and the Arts (Scitovsky 1989).

Yet another attempt to grasp the

ethical and moral dimensions of economic behaviour is developing

in two new sub-discipline: behavioural and experimental

economics. While providing meaningful insights into economic

behaviour they do not, at least yet, offer any basis for

modelling of the economy as a whole.

4.6 National Innovation System

Phillips and Khachatourians (2001), quoting

Metcalfe, define the national system of innovation (NSI) as

“that set of distinct institutions which jointly and

individually contribute to the development and diffusion of new

technology and which provides the framework within which

governments form and implement policies to influence the

innovation process. As such it is a system of interconnected

institutions to create, store and transfer the knowledge, skills

and artifacts which define new technologies.” The OECD

formalized the concept the knowledge-based economy in

1996 and then a blue print

for its members called National Innovation Systems (OECD 1997).

Governments around the world are now

consciously designing NIS’s in an effort to enhance their

competitiveness (Pagan 1999). Intellectual property rights

regimes can arguably be considered a critical part of the NIS.

The biotech sector is one of the chief objects of such NSI.

However, the role of multinational corporations is generating

stresses and strains on its successful operation in many

countries (Patel and Pavitt 1998).

For my purposes, the NIS can be defined a

nonprofit academic institutions partnering with government and

private for-profit actors to create networks of specialized

research centres in priority knowledge domains, disciplines,

sub-disciplines and specialties. Such centres are intended to

facilitate commercial exploitation of new knowledge and enhance

the competitiveness of the nation. In the process, three

important structural changes are taking place.

First, the

mandate of the university is changing. The medieval university

was focused on interpretation of old knowledge. This mandate

changed little following the Scientific Revolution of the 17th

century. With religious wars waging, the university –

Protestant and Catholic – were busy defending religious

doctrines and resisted the new experimental philosophy. In

effect, the university remained a training ground for elites in

traditional and proper ways of knowing. It was not until 1809

that the first research university was founded in Berlin

transforming the mandate of the university - traditional and

conservative heartland of Western knowledge - from

interpretation of old to the generation of new knowledge. Today,

the mandate of the university is arguably being enfolded within

the NIS transforming it to generation and commercial

exploitation of new knowledge (Nagy Nov. 3, 2005). As

predicted, this has produced a significant clash of cultures

within the university itself (Chartrand

1989). In turn this clash is causing the birth of the

third age of the university - from interpretation to generation

to commercialization of knowledge - including the teaching

function (Chartrand

2008). Biotech has been a major change agent in this

process producing a new breed - the entrepreneurial scientist.

The process itself, however, began in the USA with a change of

government policy concerning the use of federally funded

research. Until 1980 (the year of the first biotech patent),

the federal government held all rights to to results of such

research; after with passage of the Bayh-Dole Act, the

university and its employees - the professoriate - retained such

rights.

Second, as

patron of the national knowledge-base, Government fosters and

promotes production of knowledge through arm’s length

institutions. Such institutions generally direct funding

according to peer evaluation. In Canada, for example, during

the last decade the federal government has endowed a number of

quasi-public foundations to support knowledge production,

e.g., “Canada Health Infoway Inc., received $500 million

from the federal government; others have received multiple

payments amounting to, for example, $300 million to Genome

Canada and $250 million for the Green Municipal Funds” (Auditor-General

of Canada Status Report, April 2002, 1.9). In the

past foundations, endowments or grant-giving councils were

involved in the production of knowledge for knowledge sake.

Today, however, as part of the national innovation strategy

these new foundations are concerned with ‘knowledge for

profit’. This means that commercial confidentiality veils many

of their activities from public scrutiny. This, in turn, raises

serious questions about the accountability of private interests

serving the public purpose, i.e.,

Government by Moonlight:

The Hybrid Parts of the State (Birkinshaw, Harden

and Lewis 1990) [Also see

my book review].

Third, to

date, the NIS has been restricted to the natural & engineering

sciences. There is, however, no reason why it cannot be

extended to other knowledge domains and practices. For example,

national cultural policy corresponds to NIS in the Sciences.

The practices, with the notable exceptions of medicine and

related engineering, have not, however, been the subject of

NIS. Accounting and legal praxis are applied to develop NIS.

They have not themselves, however, been subjected to comparative

advantage analysis, nor networked into NIS nor held accountable

for their contributions – positive and negative – to

competitiveness. I suspect they will, formally or informally,

shortly be enfolded within the NIS framework. Arguably, heated

political debate in the United States concerning tort and

product liability represents the opening move towards seeing

national legal systems from a competitiveness perspective.

Similarly, the accounting profession in the United States is,

under the terms of the Sarbanes-Oxley Act of 2002, now subject

to oversight unknown before the Enron scandal and the collapse

of Arthur Anderson & Co. This too may be but a first step in

enfolding accountancy within the NIS web.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}