In Industrial

Organization every industry has a distinct Structure or

organizational character. The traditional elements of Structure

are barriers to entry, the number and size distribution of

firms, product differentiation and price elasticity of demand

for its output. An industry may have barriers to new firms

entering in competition to existing firms. Such barriers

include economies of scale and of scope as well as exclusive

possession of critical inputs to the production process. This

may be physical or legal possession in the form of intellectual

property rights. The number and size of firms also varies

between industries. Some are competitive with many small firms,

a.k.a, perfectly competitive with respect to price.

Others are oligopolies with a few large firms dominating the

industry with a competitive fringe of smaller firms competing in

niche markets. Some are effective monopolies with only one firm

dominating the industry and a competitive fringe. Similarly

there are industries in which the output of each and every firm

is judged homogenous by consumers - final and/or intermediary.

In other industries output by different firms is seen as

distinct and different by consumers, e.g., through

branding.

2.1 Market

The market is the

basic structure of any industry. It is any arrangement that

enables buyers and sellers or consumers and producers to get

information and do business with each other. Put another way,

markets are where demand meets supply. Markets can be described

by reference to whether they are:

- geographic,

commodity or virtual, e.g., eBay;

- in or out

of equilibrium;

- sensitive

to change in prices and incomes (elasticity);

- influenced

by an individual or group of consumes or producer;

- tightly or

loosely regulated by government.

Market Demand & Supply Curves

First, however, we must aggregate the demand curves of all

consumers and the supply curves of all producers to generate the

market or industry supply curve. Market demand is calculated as

the horizontal summation of individual consumer

demand curves, i.e. how much each individual consumer is

willing to buy at each and every price. It is important to note

that the industry demand curve can thus be aggregated or

disaggregated into market segments or niches.

The Law of Demand also holds for the market demand curve:

the higher the price the lower the demand, the lower the price

the higher the demand, It is assumed that there are

constant prices for all other commodities as well as

constant consumer income and constant consumer

preference amongst alternative goods and services or

commodities.

Similarly, the market supply curve is calculated as the

horizontal summation of the supply curves of all firms. Market

supply is calculated as the horizontal summation of the supply

curves of individual firms, i.e. how much each

individual firm is willing to supply at each and every price.

It is important to note that the industry supply curve can also

be aggregated or disaggregated into market segments or niches.

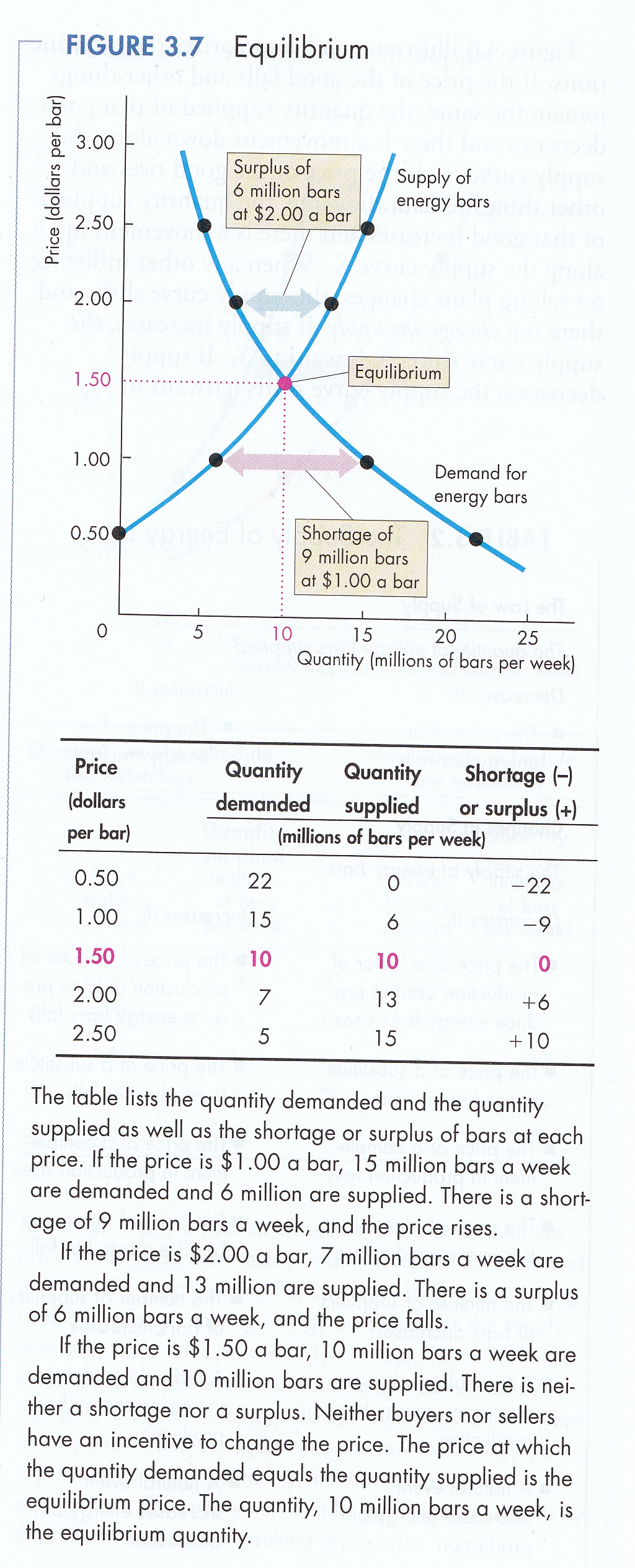

With Market Demand and Supply Curves we generate an ‘X’-shaped

graph

with Demand increasing as price goes down and Supply increasing

as price goes up. There will be a point where the two

intersect. That is called market equilibrium, the point at

which the willingness to buy and the willingness to sell are

equal. Ceteris paribus, this will be a stable

equilibrium, i.e., if all variables remain fixed,

e.g., technology, factor prices, consumer taste, income and

the price of all other goods & services, the price-quantity

equilibrium will be maintained.

Under such fixed conditions if the price

rises, for whatever reason, above equilibrium firms will be

willing to provide more than consumers are willing to buy. A

surplus is created. To eliminate the surplus firms lower price

returning eventually to equilibrium. Similarly, if price drops

below equilibrium consumer demand exceeds supply and a shortage

results. Consumers will then bid up the price until it returns

to equilibrium. These are called ‘market forces’ (P&B 4th Ed.

Fig. 4.8; 5th Ed.

Fig. 3.7;

7th Ed Fig. 3.7

R&L 13th Ed

Fig. 9-7).

The actual market outcome – price/quantity –

will, however, depend on the nature of the market. If there are

many, many sellers of identical goods and many, many buyers

there is ‘perfect competition’ and ‘X’ marks the spot. If not,

the outcome reflects the exercise of market power, i.e.,

the ability of one or more buyers or sellers to influence the

final price/quantity outcome.

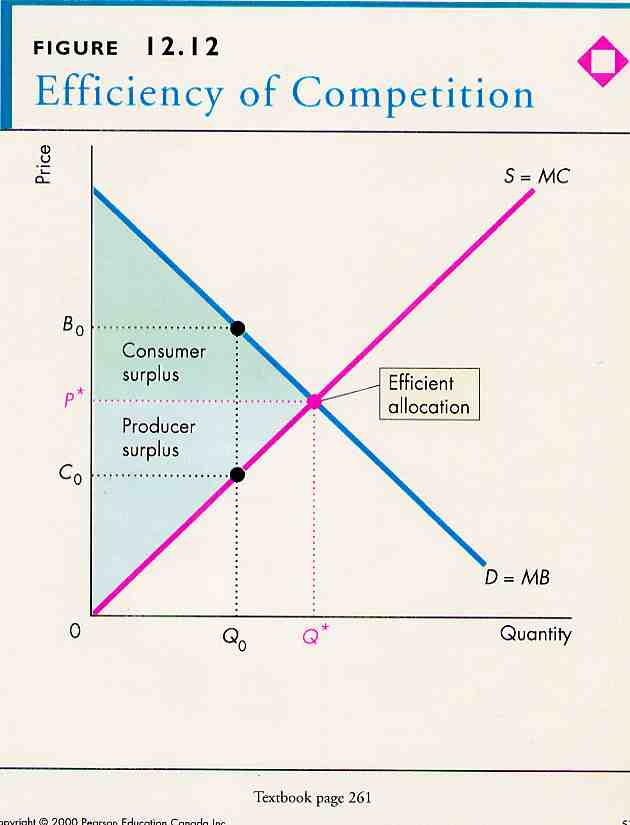

Economic Surplus

In a given market there will be gains

of exchange enjoyed by both consumer and producer. The total

measures the economic surplus.

Consumer

Gains to consumer are called

consumer surplus

(P&B 4th Ed.

Fig. 12.12; 7th Ed

Fig 12.12b; R&L

13th Ed

Fig. 12.4). It

measures the difference between what consumers would be willing

to pay for a given quantity and what they actually pay.

Consumer surplus is measured as the area from market price up to

the demand curve.

Producer

Gains to producers are called

producer surplus

(P&B 4th Ed.

Fig. 12.12; 7th Ed

Fig 12.12b; R&L

13th Ed

Fig. 12.4). It

measures the difference between what firms would be willing to

accept for a given quantity and what they actually receive.

Producer surplus is measured as the area from market price down

to the supply curve.

We now turn to the four major industrial structures: perfect

competition, monopolistic competition, monopoly/monopsony and

oligopoly/oligopsony. In this regard the concentration ratio

can be used as a measure of industrial structure to indicate the

form of competition in a given industry. It is the percentage

of total output supplied by a given number of the largest

firms. In the case of monopoly, for example, one firm supplies

100% of output. In perfect competition and monopolistic

competition the largest 100 firms might contribute just 10 or

20% of total output. In oligopoly/oligopsony the largest 5

firms might account for 50 to 60% or more of total output.

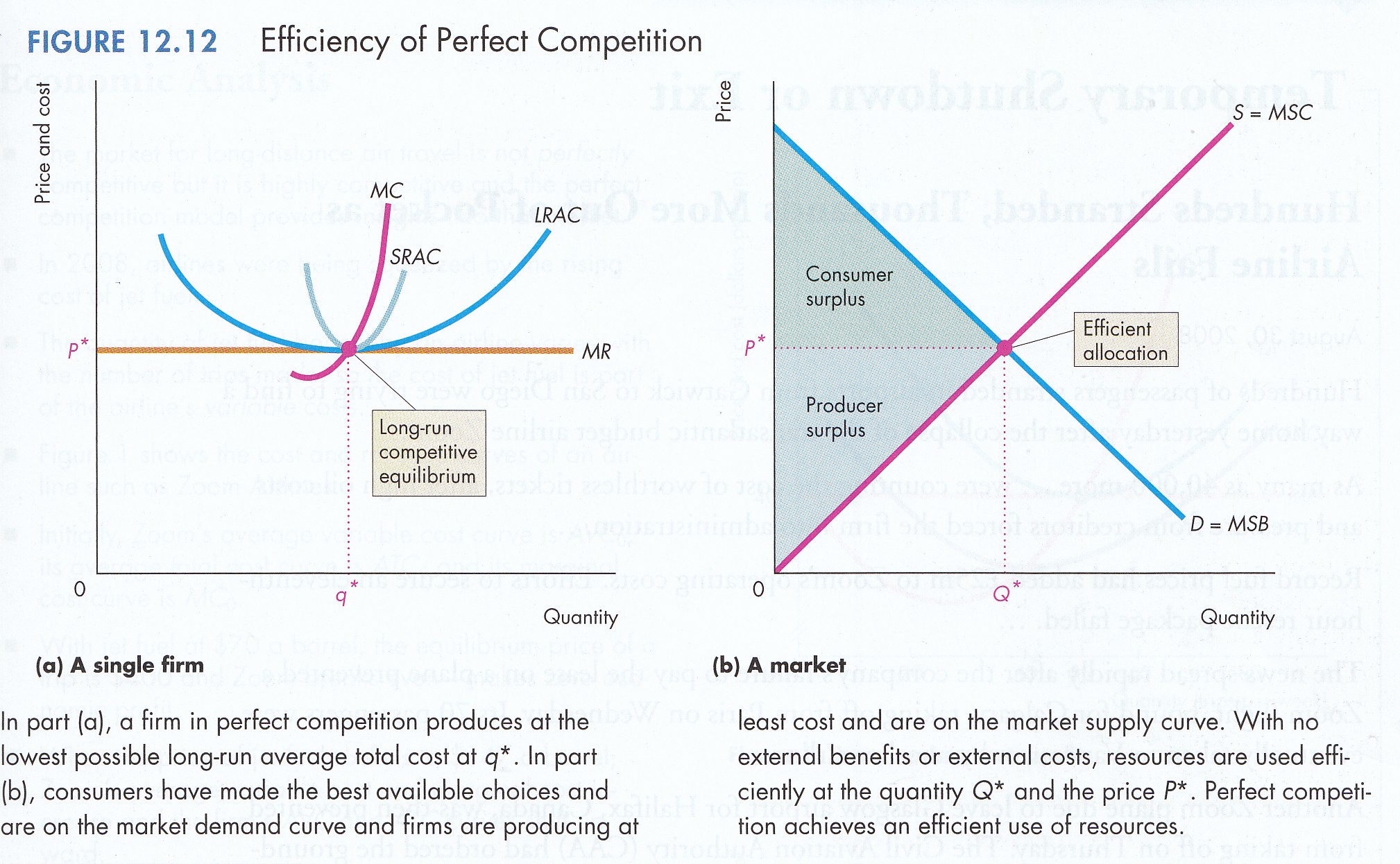

2.2 Perfect Competition

Perfect competition

satisfies four strict conditions:

Anonymity

Consumers are

indistinguishable to producers. Firms have no reason to favor

one consumer over another. The product of different firms is

indistinguishable, one from another, in terms of price, quality

and product differentiation. They are 'homogenous'. Consumers

have no reason to prefer the product of one firm over that of

another. Similarly, any one consumer represents a tiny portion

of market sales and producers have no reason to prefer one

customer over another.

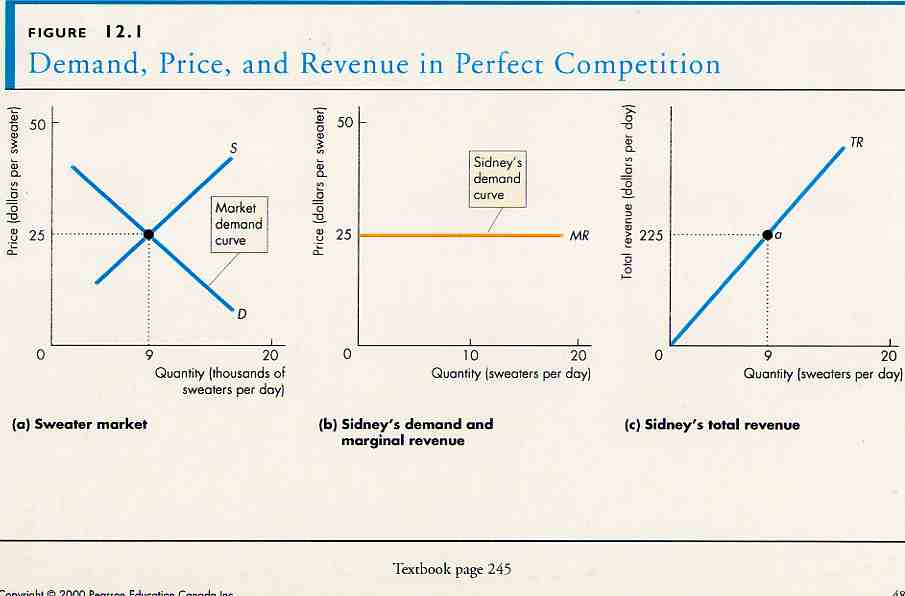

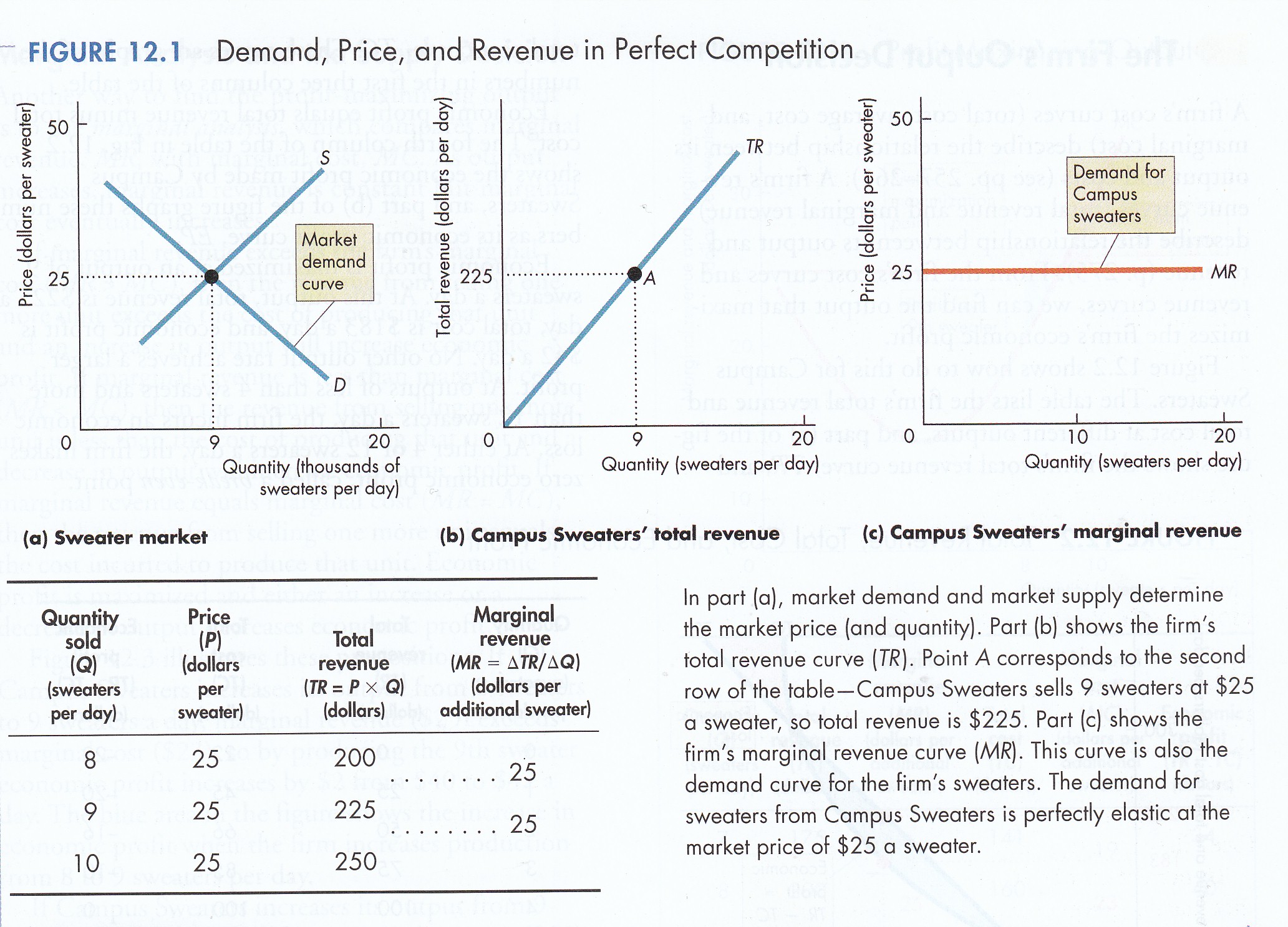

No Market Power

There is a large

number of both producers and consumers. Sales or purchases by

any buyer or seller are small relative to the total volume of

exchange. No buyer or seller can affect price or quality, i.e.,

no one exercises market power. All consumers and producers

respond and adjust only to price signals. The perfect

competitor does not in fact face the market demand curve but

rather market price. The firm is thus a price taker rather than

a price maker. It can sell as much as it wants at market price

but loses all business if it raises the price of its homogenous

output (P&B

4th Ed.

Fig 12.1;

5th Ed Fig. 11.1;

7th Ed

Fig. 12.1).

Perfect Knowledge

Consumers and

producers possess perfect knowledge about price and quality. No

firm can charge more, and no consumer can pay less than the

market equilibrium price.

Free Entry & Exit

Entry and exit from

the market is free for both consumers and producers. There is

an unimpeded flow of resources between alternative uses i.e.,

resources are mobile and move to the use with greatest

advantage in terms of opportunity costs. Firms exit if they

experience ‘economic’ loss. Thereby inefficient firms are

eliminated from the market. Firms enter the market if they

expect to earn economic short-run, and/or, normal

long run profits. On the demand side of the Marshallian

scissors, there are many close substitutes available to

consumers who can easily switch if price, preference and/or

income changes.

2.3 Monopolistic

Competition

Monopolistic competition

satisfies two conditions of perfect competition but fails to

satisfy two others.

Market Niche/Segment

As in perfect

competition there are a large number of sellers. The output of

firms is not, however, considered homogenous by consumers.

Rather they are differentiated. Consider the restaurant

industry. Hamburgers and hot dogs are not the same as pizza or

fried chicken. Some consumers prefer one or the other. In

effect, the market demand curve is disaggregated into distinct

market niches or segments.

Market Power

Within each niche a firm

faces a downward sloping demand curve for its product, i.e.,

they can sell more if they lower price and less if they raise

it. A seller therefore possesses market power, i.e., the

ability to influence the price/quantity outcome, depending on

the elasticity of demand.

Perfect Knowledge

As in perfect

competition, consumers and producers possess perfect knowledge

about price and quality including product differentiation.

Free Entry & Exit

As in perfect

competition, under monopolistic competition entry and exit from

the market is free for both consumers and producers. There are

no barriers to entry or exit. There is an unimpeded flow of

resources between alternative uses i.e., resources are

mobile and move to the use with greatest advantage in terms of

opportunity costs. Firms exit if they experience ‘economic’

loss. Thereby inefficient firms are eliminated from the

market. Firms enter the market if they expect to earn

economic short-run, and/or, normal long run

profits. On the demand side of the Marshallian Scissors,

there are many close substitutes available to consumers who can

easily switch if price, preference and/or income changes.

2.4 Monopoly/Monopsony

Monopoly and monopsony

satisfy one and fail to satisfy three conditions of perfect

competition.

One Seller/Buyer

There is, in the case of

monopoly, no distinction between the firm and the industry,

i.e. there is only one producer. In the case of monopsony,

there is no distinction between the single consumer and the

industry. An example of monopsony is the U.S. Air Force, the

only buyer of B2 bombers.

Market Power

In monopoly, one

producer faces the market demand curve and can accordingly sell

more if it lowers its price and sell less if it raises it. In

monopsony, one buyer faces the market supply curve and can buy

more if it pays a higher price and less if it pays a lower one.

The monopolist is able

to choose the price-quantity combination to maximize its

profits, i.e., it is a price maker. Monopoly power is

mitigated only by competition from substitutes. The closer the

substitutes the less market power is available to the

monopolist. Similarly, the monopsonist can choose which

price/quantity outcome will minimize its cost.

There are, however, two

types of monopoly, i.e., a single price and

discriminating monopolist. The single price monopolist sells

output at the same price to all consumers. The discriminating

monopolist, on the other hand, disaggregates the market demand

curve into individual consumer demand curves. It can then

charge a different price to each individual consumer extracting

the maximum of consumer surplus from each individual consumer.

In effect the discriminating monopolist is able to play on the

willingness of consumers to pay a higher price for a smaller

quantity due to diminishing marginal utility.

Perfect Knowledge

As in perfect competition, consumers and the

monopolist both possess perfect knowledge about price

and quality including substitutes.

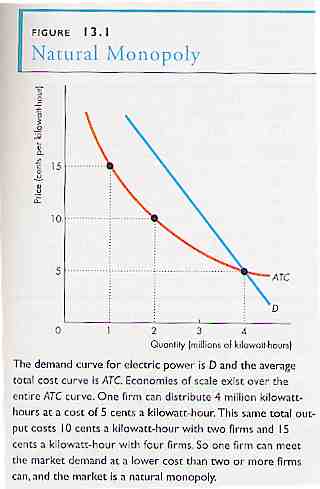

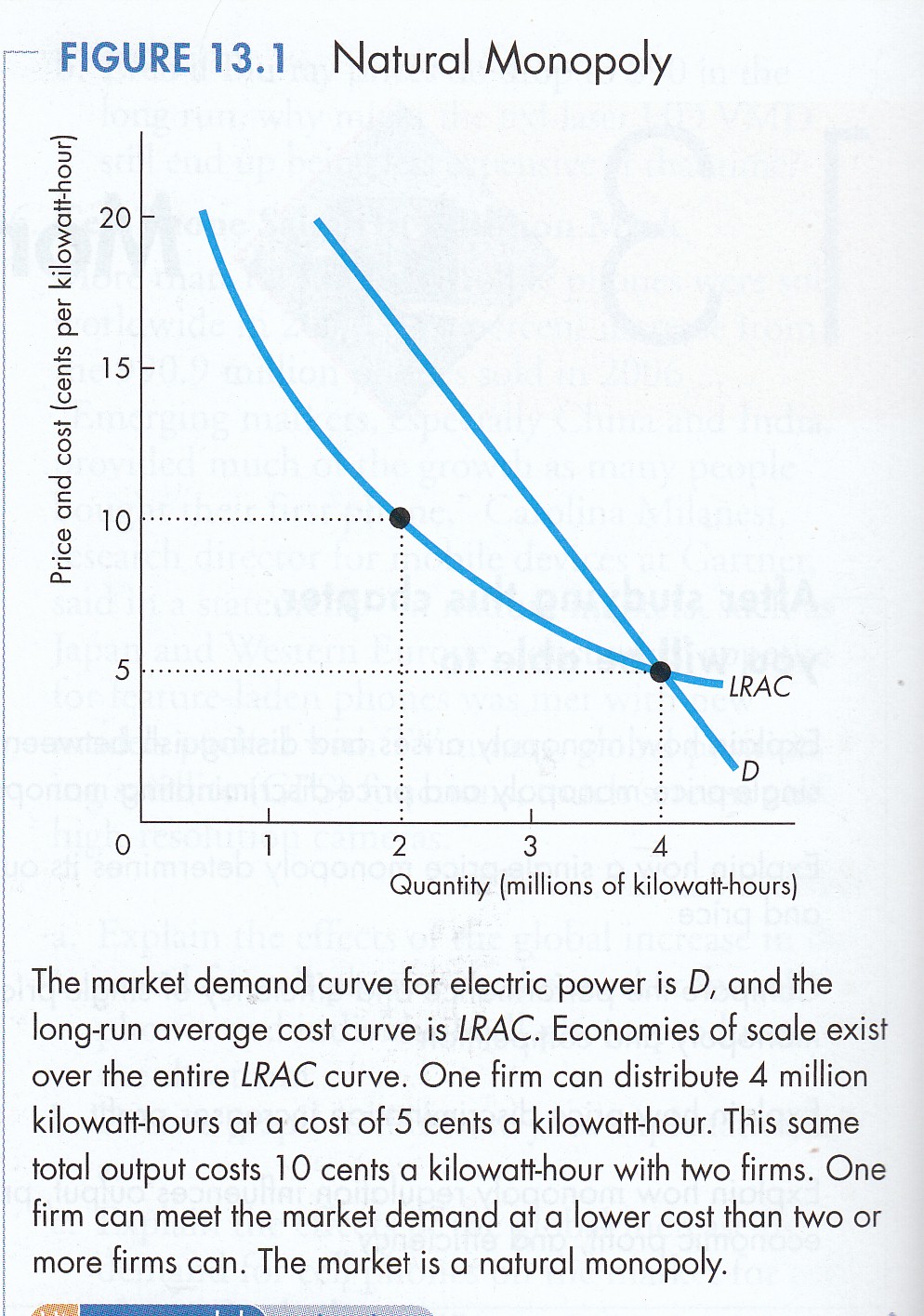

Barriers to Entry

Monopoly exists for one, or more, of four

reasons. First, a firm may become a monopolist because

economies of scale allow the monopolist reach an output level

sufficient to supply the entire market at minimum average cost

per unit. This is a natural monopoly (P&B 4th Ed

Fig. 13.1; 5th Ed. Fig. 12.1;

7th Ed Fig. 13.1; R&L 13th Ed not displayed).

Second, one firm may control the entire supply of a basic

input. An example would be a mineral critical to production of

the good in question and the monopolist owns the only mine

producing that input. Third, a firm may acquire control

over a product due to an intellectual property right -

copyright, patent, registered industrial design or trademark -

granted by the State. Fourth, a firm may become a

monopolist because government awards an exclusive market

franchise, e.g. electric power, water supply, etc.

A monopolist is not, however, entirely

insulated from the economy as a whole. All commodities are

rivals for the consumer’s limited income. The closer are

substitutes, the greater the moderating influence on a

monopolist. The threat of entry by outsiders interested in

gaining some of the monopolist’s excess profits also serves to

moderate pricing behavior, e.g. the threat that cable

companies could offer telephone service will limit the pricing

of a telephone monopolist.

2.5 Oligopoly/Oligopsony

Oligopoly/oligopsony

satisfies none of the conditions of perfect competition.

Few Large Sellers/

Buyers

In the case of

oligopoly, there is a small number of large firms that dominate

the industry. Often these majors are surrounded by a

competitive fringe of smaller firms usually operating in

distinct market niches or segments. The action of a major

producer is perceptible to rivals, i.e. there is

interdependency of sellers whereby an action by one results in

reaction of others. Furthermore, the output of producers is not

seen as homogenous by consumers. This is often the result of

successful branding. Thus each major enjoys a certain market

share based on product differentiation.

In the case of

oligopsony, there is a small number of large buyers that

dominate the industry. Often these majors are surrounded by a

competitive fringe of smaller buyers, again usually operating in

distinct market niches or segments. The action of a major

buyer is perceptible to rivals, i.e. there is

interdependency of sellers whereby an action by one results in

reaction of others. An example of an oligopsony are the ‘big

box stores’ like Walmart, Target, Safeway, etc. Due to the

scale of there purchases they can influence the price/quantity

outcome at which they buy from suppliers.

Market Power

Due to economies of

scale, product differentiation like

branding as well as process/product innovation, oligopolists

exercise market power in determining the equilibrium

price/quantity relationship in a market.

Imperfect & Asymmetrical Knowledge

Unlike perfect competition, consumers as well

as oligopolists and oligopsonists do not possess perfect

knowledge. Specifically, they do not know how or when other

players will react to the actions of a major. For example, if

Ford Motor Company offers zero percent APR (above prime rate)

financing will Toyota respond the same way or choose an

alternative strategy like a long warranty? This opens up

the question of asymmetrical information including issues such

as insider trading.

Barriers to Entry

Oligopoly/Oligopsony also exhibit barriers to

the entry of new firms. Economies of scale can thus inhibit

entry. Product differentiation through branding can also make

it difficult for a new firm to enter the industry. And, as will

be seen under 4. Performance, the excess or economic profits

earned by oligopolists allow them to invest in advertising –

branding – as well as product and process innovation. A lean,

mean, perfectly competitive firm can afford neither.

2.6

Integration/Conglomerateness

In Microeconomic

theory we are dealing with a single product, profit maximizing

firm. In Industrial Organization we are dealing with real world

industrial structures which include vertical, horizontal and

conglomerate integration.

Vertical integration

unites under one owner a number of plants engaged in successive

processes or stages of production. An example is a vertically

integrated oil company co-temporally engaged in exploration,

production, refining and retailing. Horizontal integration

unites under one owner a number of plants engaged in the same

processes or stage of production. An example is a multi-plant

firm engaged in metal fabrication. Output becomes an input to

other industries which combine them with yet other inputs in

their own production process.

Conglomerateness, on

the other hand, involves diversification beyond the boundaries

of any given industry. Conglomerate mergers were the rage in

the United States during the 1960s because anti-trust policies

inhibited significant concentration due to either vertical or

horizontal mergers. With fat profits in their corporate pockets

many firms argued that ‘management’ was the ultimate economic

resource. If one could manage steel then one could manage

airlines, chocolate bars or any other business. In effect,

local knowledge was considered less important than management in

building a business success. With the notable exception of

General Electric most conglomerate mergers of the ‘60s failed.

2.7 Government Intervention

Government

intervention is a pervasive structural characteristic of all

industries and markets. The form and nature of that

intervention takes varying forms. Bankruptcy, environmental,

financial, health & safety, incorporation, labour and protection

of persons & property are just some of the areas in which

government plays an active role in every industry. I will first

argue that equity provides both the legal and economic rationale

for governmental intervention. I will then highlight non-market

forces unleashed by certain forms of governmental intervention,

specifically price setting.

Anti-Trust & Combines in a Global

Economy

from 50s to Globalization

Equity & Regulation

Courts of Common Law are one of the great

contributions of the Anglosphere. Formally beginning in the

reign of Henry II in the 12th century, Common Law, unlike

Statutory and Regulatory Law, originates in the Anglosphere.

Two things make Common Law different. First, judges may

“make” Law by setting precedents. The body of precedent is

called “common law”. If a similar case was resolved in the

past, a current court is bound to follow the reasoning of that

prior decision on the principle of stare decisis. The

process is called casuistry or case-based reasoning. If

a current case is different, however, then a judge may set a

precedent binding future courts in similar cases. Casuistry

must begin again, however, if changes or amendments to Statutory

or Regulatory Law negate the precedent.

Second,

Common Law is rooted in trial by jury, i.e., one’s

peers. This is a fundamental civil right in the Anglosphere in

criminal law. By contrast, the European Civil Code tradition is

based on trial by judge/prosecutor, i.e., the police and

judicial functions merge in one office. On the other hand, the

impresciptible

moral rights of authors are recognized

under Civil Code but not Common Law. Similarly there is the

treatment of torts, i.e., non-contractual rights and

obligations. Under Common Law they are treated by precedent and

trial ‘attorneys’ in the U.S.A. enjoy a large practice. Under

Civil Code such questions are answered by principle, somewhat

like equity in the Anglsophere.

However, at the same time the Common Law

arose during the resign of Henry II another unique Anglosphere

juridical institution emerged – Equity. It was not guilt or

innocence but fairness of punishment before the King. This is

the root of Equity – a separate and distinct strand of

jurisprudence parallel to the Common Law of precedent.

Over time responsibility for hearing calls

for mercy was transferred to the King’s Lord Chancellor and a

court of his own – the Court of Equity also known as the Court

of Conscience or of Morality. In fact until Sir Thomas More (a

lawyer) became Chancellor in 1529, all had been men of the

cloth. Two aspects of Equity played a critical role in the

Sovereign’s ability to control his vassals. These were trusts

and tenant-landlord disputes. Trusts (from which modern

charities and financial trusts evolved) generally concerned

widows and orphans left to the mercy of a local lord. The most

famous is Lady Marion of the Robin Hood legend who was an orphan

and ward of the King. With respect to tenant-landlord disputes,

Equity balanced the feudal local lords by judiciously connecting

the King to his subjects. This was called the ‘rent bargain’ by

J.R. Commons (1924). It stabilized the social system of

post-Conquest England.

While Magna Carta (1215) and

subsequent developments increasingly limited the King, Equity

and Common Law continued to develop as parallel systems of

courts with precedence given to Equity. It was not until 1873

in the United Kingdom that the two systems of courts merged,

i.e., cases at Equity could be heard by the same courts that

ruled under Common Law. Nonetheless the two strands of

Anglosphere jurisprudence continue to this day in all Common Law

countries with Equity retaining precedence.

The economic concept of Equity arguably

derives from legal Equity. In fact the Chancellor of the

Exchequer exercised a concurrent jurisdiction in Equity with the

Lord Chancellor’s Court. There are three economic definitions

of Equity, each reflecting its historical roots. First,

there is Equity as the capital of a firm which, after deducting

liabilities to outsiders, belongs to the shareholders. Hence

shares in a limited liability corporation are also known as

equities. This links back to the historical treatment of trusts

under Equity.

Second,

there is Equity as ‘fairness’. While often used with reference

to taxation it is a general economic concept. With respect to

taxation Equity has three dimensions: horizontal, vertical and

overall burden. Horizontal Equity refers to ‘like treatment of

like’. Vertical Equity refers to ‘unlike treatment of unlike’.

Overall Equity refers to the accumulated impact of all forms of

taxation. Crudely, it is the difference between earned and

disposable income after all taxes – income, excise, sales, et

al.

Equity thus provides the legal and economic

rational for government intervention in the economy. Such

interventions include, of course, the Corporations Act and

Bankruptcy Act. It also justifies anti-trust and anti-combines

legislation to counter the exercise of market power.

Non-Market Forces

We have seen that if a competitive

market is allowed to operate an equilibrium price/quantity

outcome will result from the interplay of market force. If

price is too high, Supply exceeds Demand and a surplus is

created. To get rid of the surplus producers must lower their

price, eventually to equilibrium. Similarly, if price is below

equilibrium then Demand exceeds Supply and a shortage is

created. Consumers wanting the good bid up its price back to

equilibrium.

What happens, however, if government

intervenes and does not allow market forces to function? I will

now consider such price setting intervention in agriculture,

housing, labour, prohibited goods and taxation.

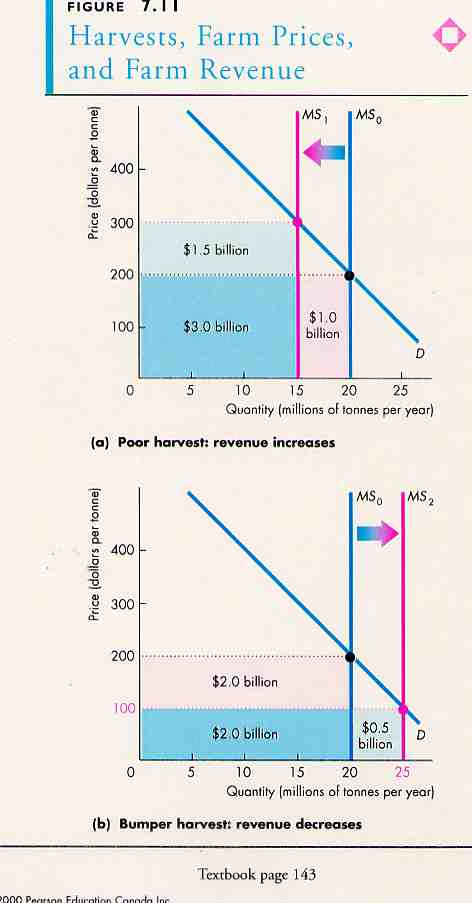

Agriculture

Agriculture is subject to significant

fluctuations in supply yet a relatively inelastic demand, people

have to eat. We begin by assuming only domestic production is

involved. In any given year, the supply is fixed and perfectly

inelastic, a harvest is the harvest is the harvest. In an

unregulated market (P&B 4th Ed.

Fig. 7.11; 5th Ed. Fig. 6.11; 7th

Ed not displayed;.

R&L 13th Ed not displayed), a bad harvest shifts supply

to the left. This raises prices and will actually increase

revenue to the farmer. A bumper crop, on the other hand, will

shift supply to the right, lower prices and reduce farm income.

Many agricultural commodities can be

stored, that is placed in inventory. Inventories serve to

stabilize prices between growing seasons. Without inventories

the above situation applies, that is a good harvest lowers

prices, a bad harvest raises prices. Inventories reduce these

price fluctuations (P&B 4th Ed.

Fig. 7.12; 5th Ed. Fig. 6.12; 7th

Ed not displayed;.

R&L 13th Ed not displayed). A good harvest can be used to

increase inventories, that is, not all output goes to market and

price decreases are moderated. In the case of a bad harvest,

inventories are sold, thereby increasing supply and reducing

price increases.

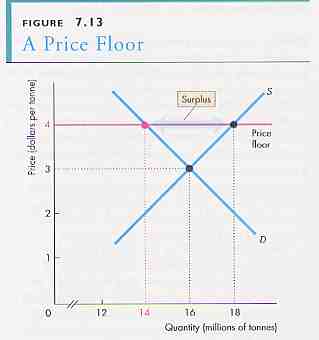

A price floor acts like a minimum

wage. If the floor is less than market equilibrium, it has no

effect. If it is greater than equilibrium price it will create a

demand gap between the larger amount suppliers are willing to

provide at the floor price, and the quantity consumers are

willing to buy (P&B 4th Ed.

Fig. 7.13; 5th Ed. Fig. 6.13; 7th

Ed not displayed;.

R&L 13th

5-2).

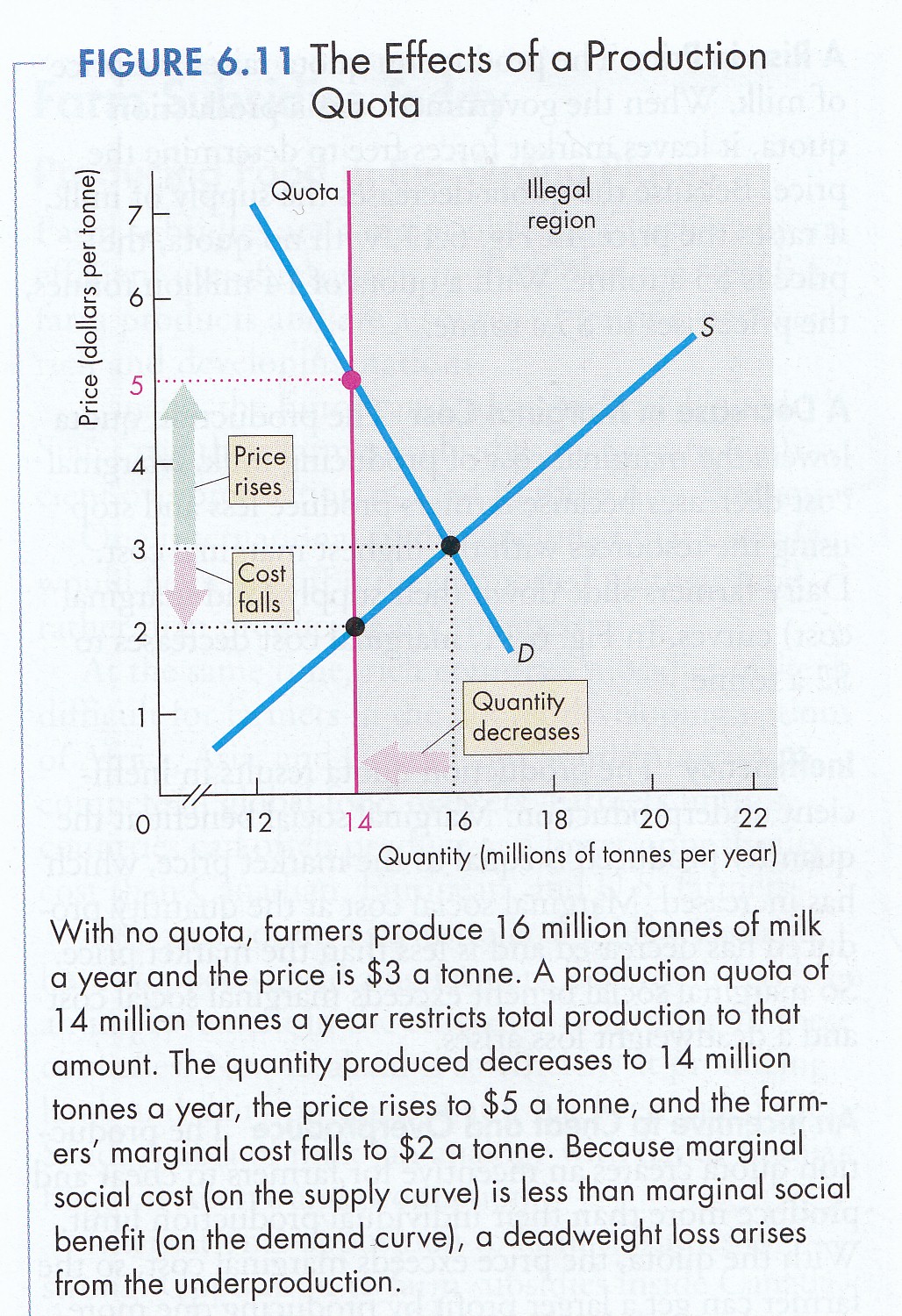

Quotas (on eggs, grain, beef, etc.)

act like a perfectly inelastic supply curve (P&B 4th Ed.

Fig 7.14; 5th Ed. Fig. 6.14; P&B

7th Ed Fig. 6.11;.

R&L 13th

5-8).

If the quota output is less than equilibrium output the price

will be higher and the supply lower. This creates a supply gap

where producers have an incentive to exceed their quota. This

can lead to increased

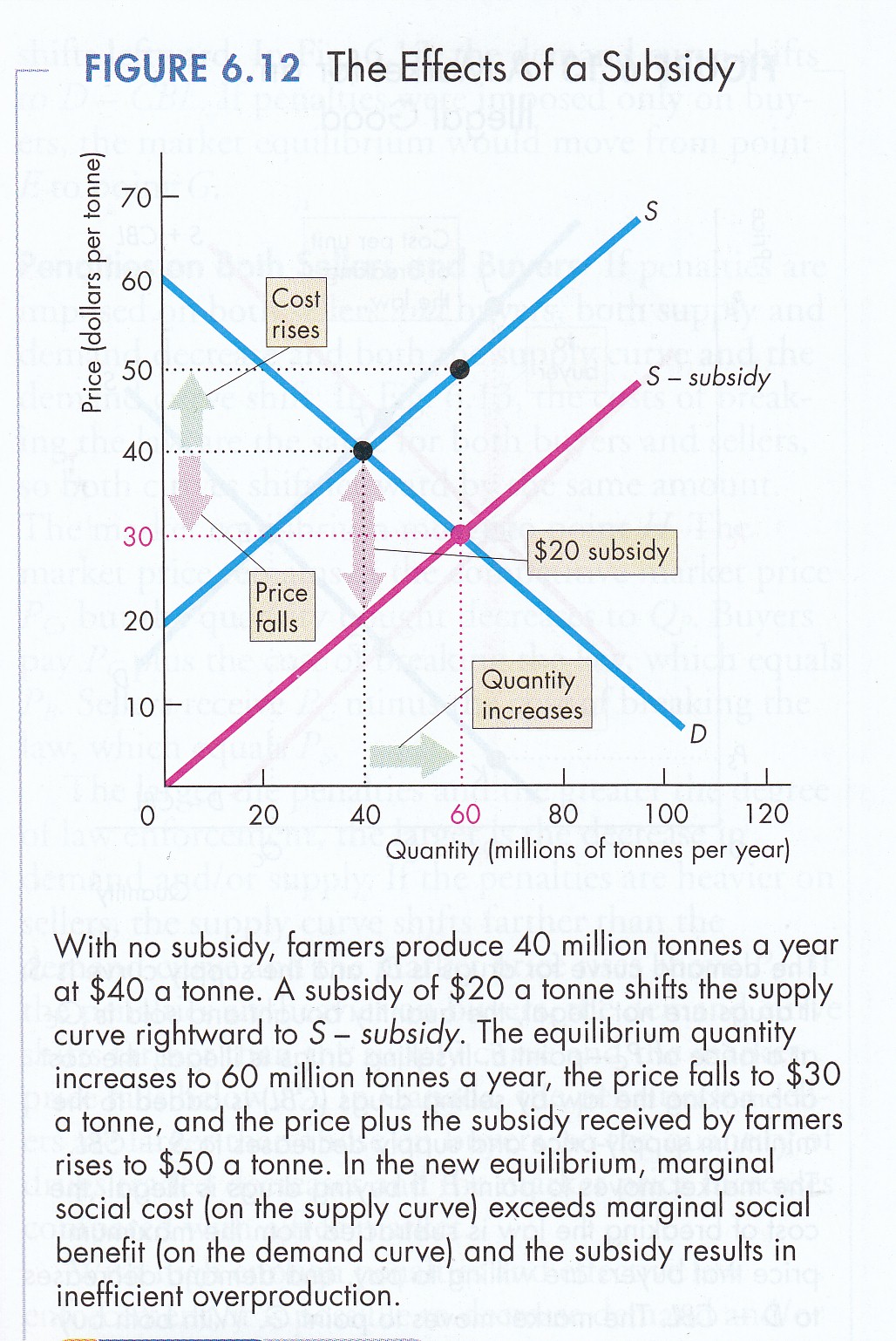

Subsidies act like a reverse tax (P&B

4th Ed.

Fig. 7.15;

5th Ed. Fig. 6.15; P&B

7th Ed Fig. 6.12;

R&L 13th Ed not displayed). The tend to shift the supply

curve to the right. Output increases and prices fall. Such

'supply-side' subsidies financially reward increased production

by offering subsidies per bushel of output or per acre planted.

This approach has led to a frightening subsidy spiral. In

effect, production subsidies reduce the final price of farm

output below the cost of production. This, in turn, means that

even efficient farmers cannot earn enough to maintain

operations. This, in turn, leads to more subsidies that lower

prices further. And, so on and so on and so on...

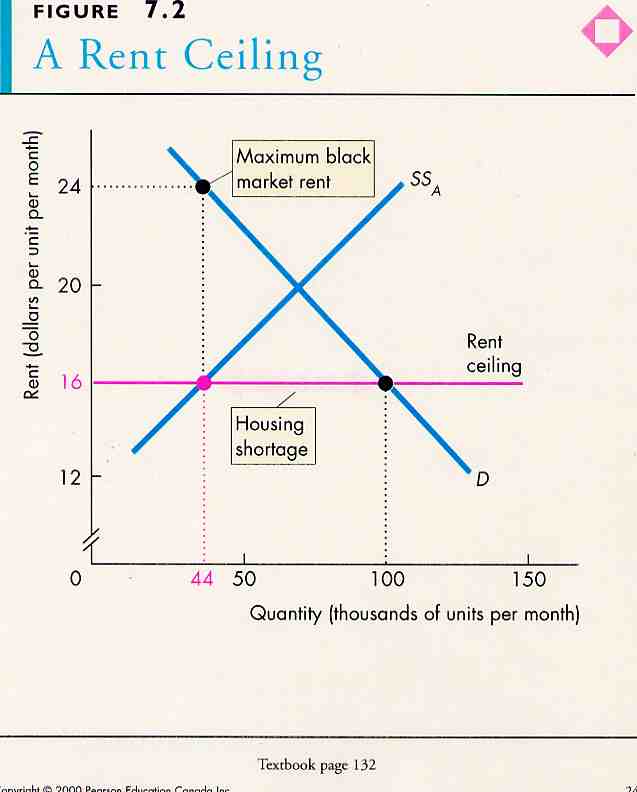

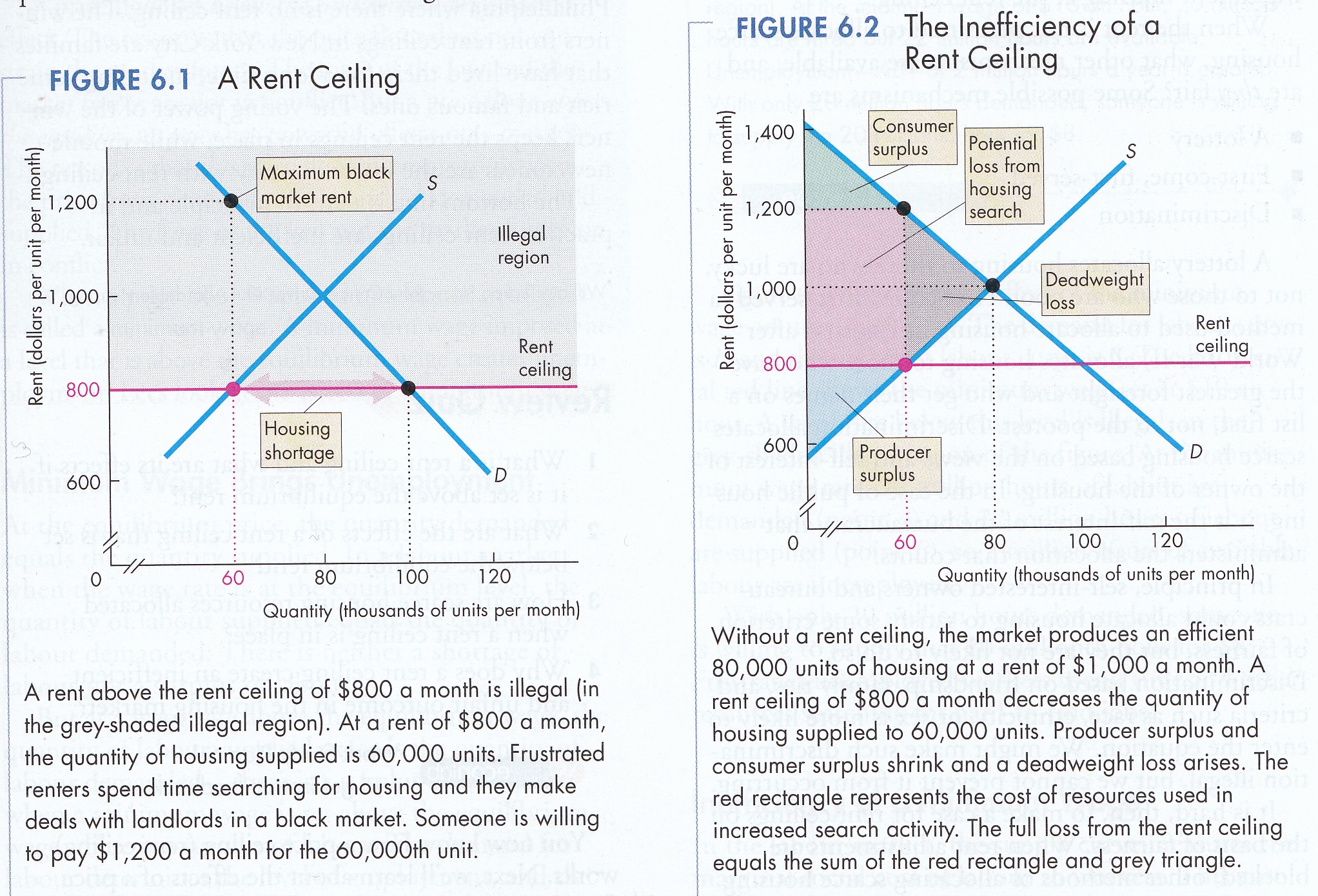

Housing

Part of the short-run adjustment

process involves price, that is, if demand exceeds supply,

prices will tend to rise. In the case of rental property, which

tends to be the type of housing available to the poorer members

of a community, a price rise takes the form of rent increases.

If government decides for reasons of vertical equity (unlike

treatment of persons in unlike situations) that the poor need to

be protected from rent increases (or for political reasons,

there are more poor voters than landowners) then it may impose

rent controls in the form of a rent ceiling (P&B 4th Ed.

Fig. 7.2;

5th Ed. Fig. 6.2; 7th Ed

Fig. 6.1 & Fig. 6.2;.

R&L 13th

5-3 &

5-4).

In effect, rent control imposes a

price which is less than that determined by the market. This

means that demand (the willingness of consumers to pay) exceeds

the supply (the willingness of producer to supply). This results

in a housing shortage. Because demand exceeds supply yet price

can not increase other forms of behaviour take the place of a

price increase. For example, given a shortage:

i - consumers must search harder and

harder to find supply when it does become available. Search

activity is costly; and/or,

ii - consumers will 'bribe' supplier,

for example, by paying more 'on the side'; by accepting little

or no maintenance or support services; by accepting 'run down

conditions'.

The effect of rent control is to

reduce the return to suppliers. If they cannot cut back

production directly they may do so indirectly. First, new rental

accommodation will not be built which, if population continues

to grow, accentuates the shortage. Second, existing rental

property will be allowed to 'run down', eventually into 'slum

condition'. With excess demand and a fixed price, the supplier

can recoup his or her opportunity cost by running the building

down until it is uninhabitable, then tear it down and build

private homes or condos for sale on an open and competitive

market without price controls. This again accentuates the

housing shortage.

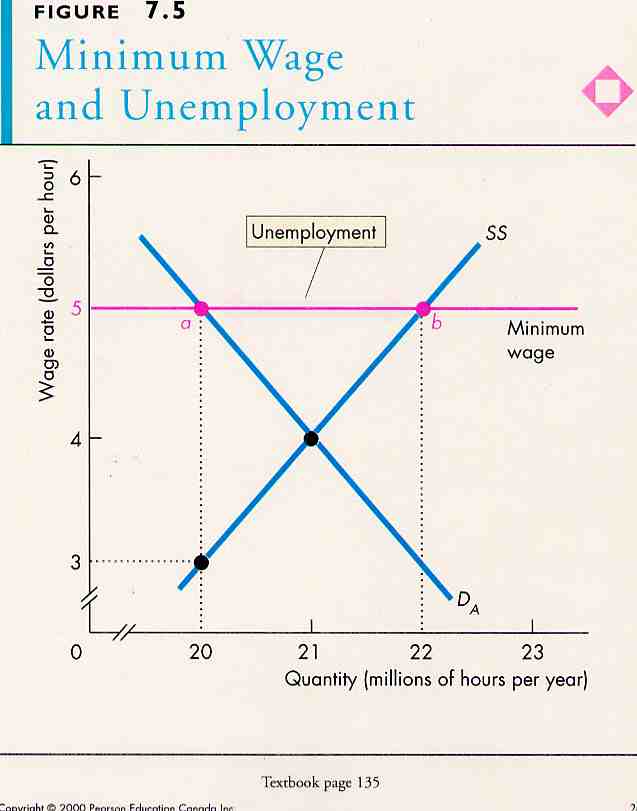

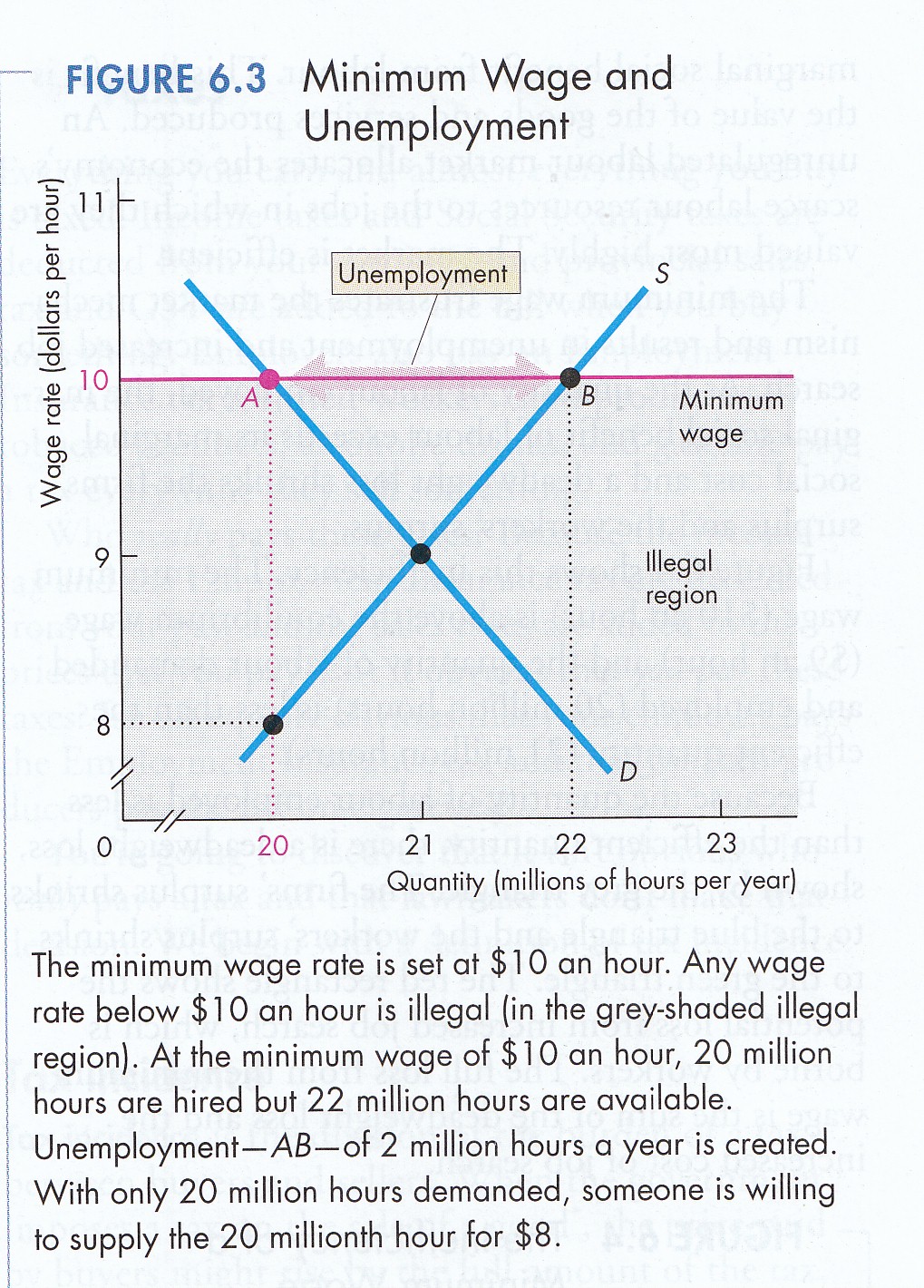

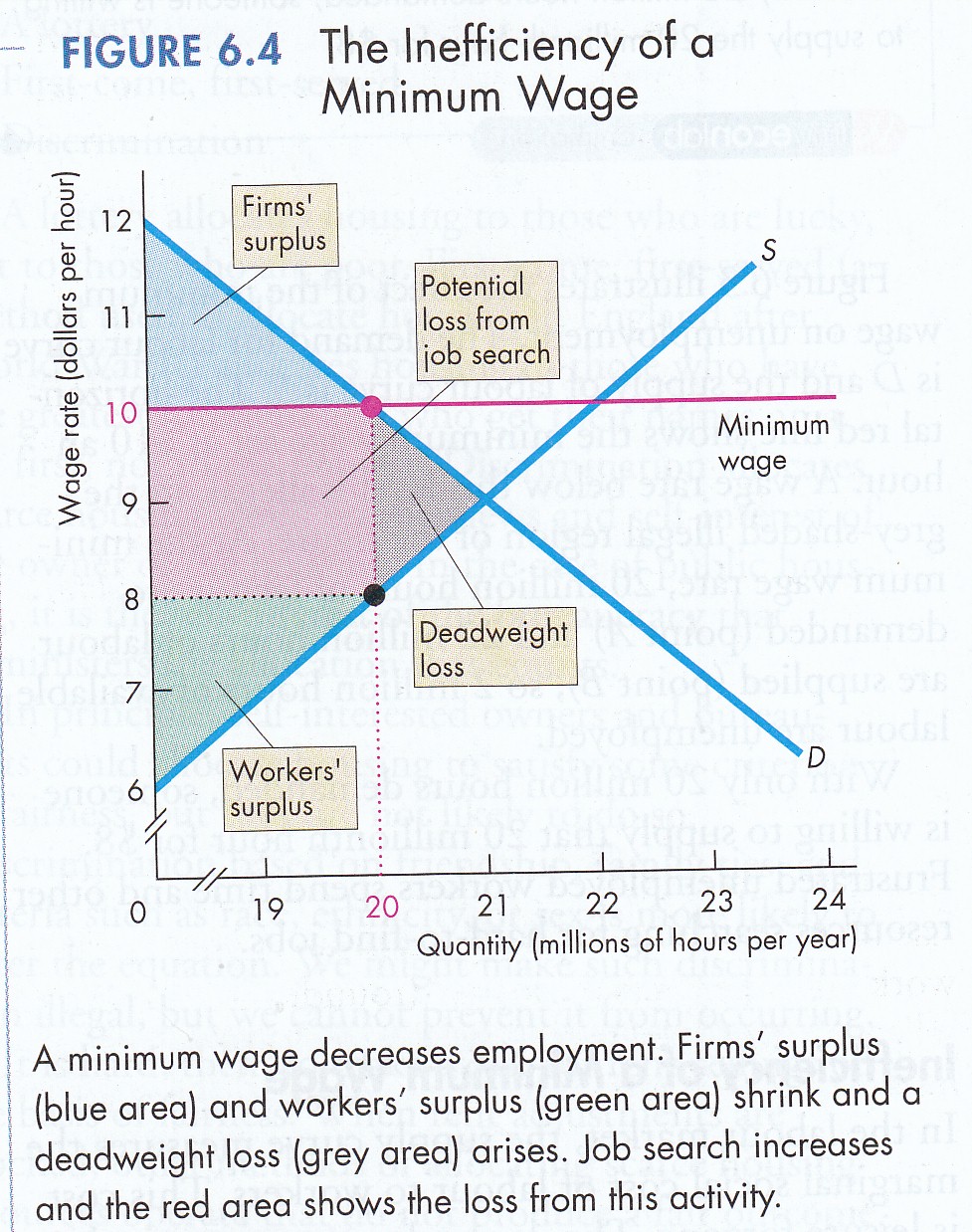

Labour

Low wages for unskilled labour may

create a question of vertical equity (or political reasons).

Government may decide that with such low wages unskilled workers

cannot support themselves, their children and/or other

dependents above the 'poverty line'. Accordingly government may

intervene by establishing a 'minimum wage rate'.

If this rate is below market

equilibrium rate such a minimum has no real effect. If, however,

it is above the market equilibrium price (P&B 4th Ed.

Fig. 7.5;

5th Ed. Fig. 6.5; 7th Ed

Fig. 6.3

&

Fig. 6.4;.

R&L 13th p. 103, no JPEG available) the supply of willing workers

exceeds the demand of producers. As in the case of rent

controls, if the price cannot adjust, other forms of behaviour

will evolve. For example, some workers will offer to work some

hours 'off the books'.

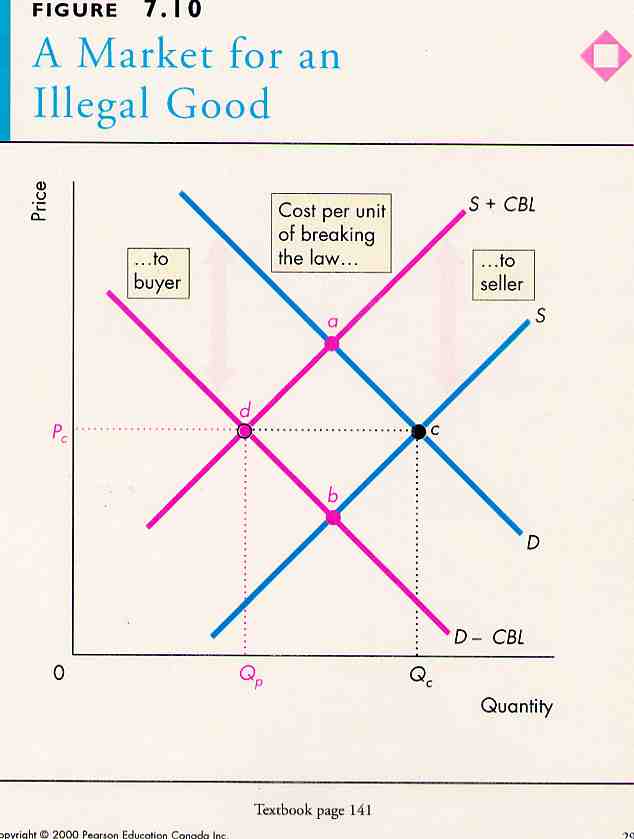

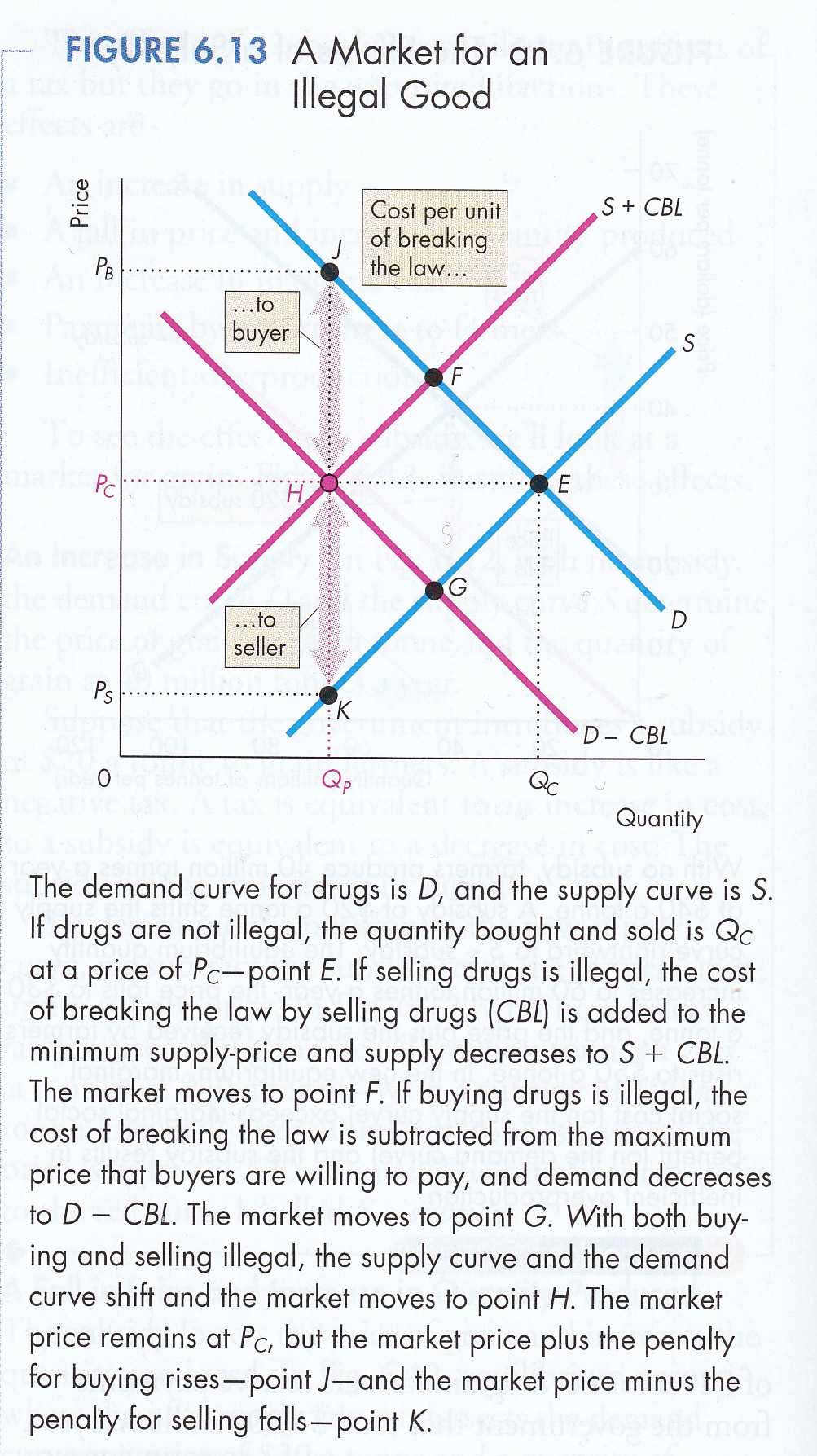

Prohibited Goods

While some goods like recreational

drugs are illegal and hence prohibited, a market exist. To

understand the effect of prohibition, we begin with market

equilibrium assuming no prohibition (P&B 4th Ed.

Fig. 7.10;

5th Ed. Fig. 6.10; P&B

7th Ed

Fig. 6.13;

R&L 13th 5-3). A prohibition affect both

demand and supply. It imposes penalties, that is costs, on both.

The effect is to shift the supply curve up to the left and shift

the demand curve down to the left.

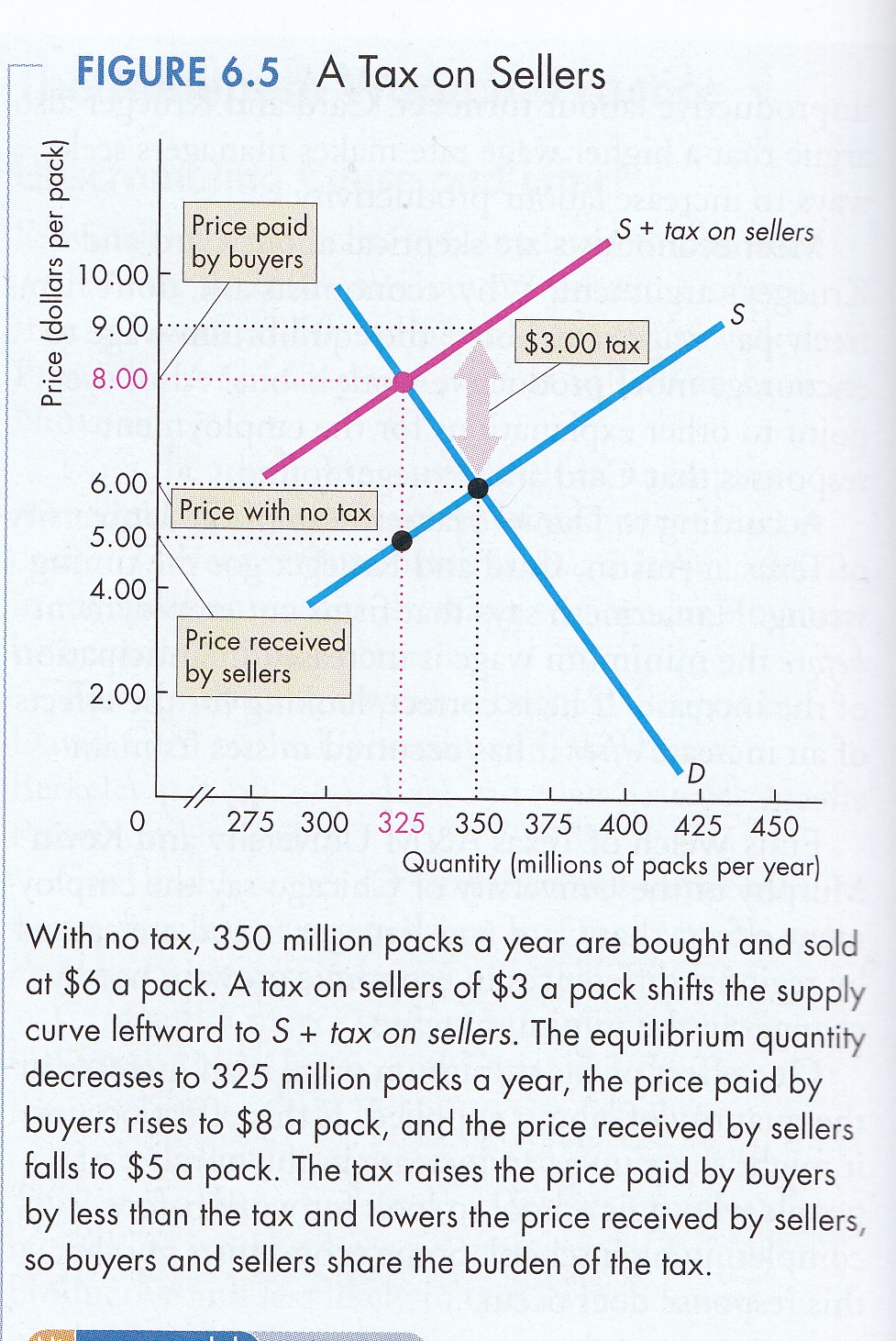

Taxation

To finance public spending (a

pleasure), government must raise revenue through taxes (a pain).

This pleasure/pain of public finance is described in the

Introduction: The Pleasure & Pain of Public Finance to my paper

"A

Radical Analysis of 'Personal' Taxation."

An increasingly important source of tax revenue is sales tax,

for example, the GST and provincial sales tax. The question

arises: who pays Is it the consumer or the producer or both?

Consumer demand does not change if a

sales tax is imposed. The demand curve reflects the quantity of

a good or service consumers are willing to buy at a given price.

If the price goes up, one slides up the demand curve; if the

price goes down, one slides down the demand curve - all things

being equal. Accordingly, to the consumer the real price of a

good is its retail price plus any associated taxes.

A sales tax does, however, shift the

supply curve up to the left. Producers are willing to supply a

certain quantity of goods or services if the receive a given

price. With sales tax, such goods and services are offered for

sale at a higher price (P&B 4th Ed.

Fig. 7.6;

5th Ed. Fig. 6.6;

7th Ed Fig. 6.5;

R&L 13th Ed Fig.

4-8

&

4-9).

The supply curve shifts and a new equilibrium is established at

a higher price and a lower quantity than before the tax.

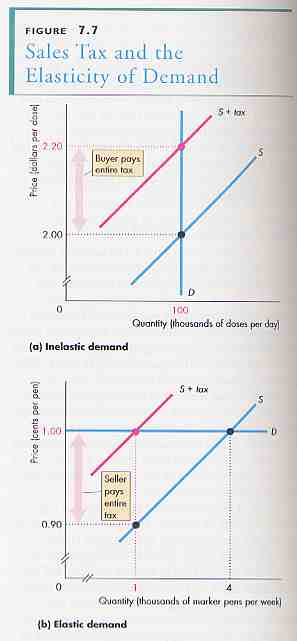

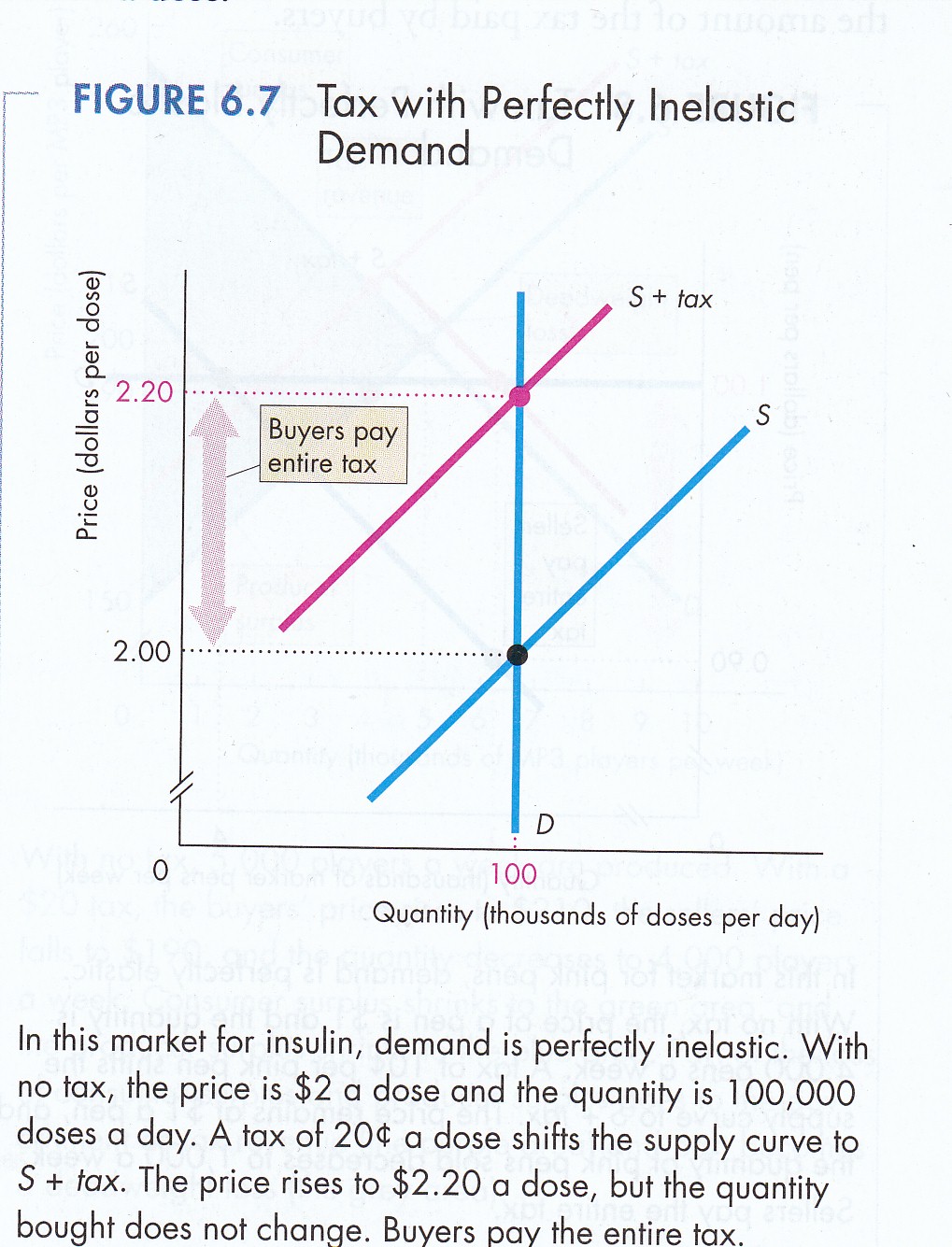

As to who pays the tax, the answer

depends on the elasticity of supply and demand. If there is

perfectly inelastic demand, for example for a 'necessity', the

demand curve is vertical (P&B 4th Ed.

Fig. 7.7a;

5th Ed. Fig. 6.7;

7th Ed Fig. 6.7)

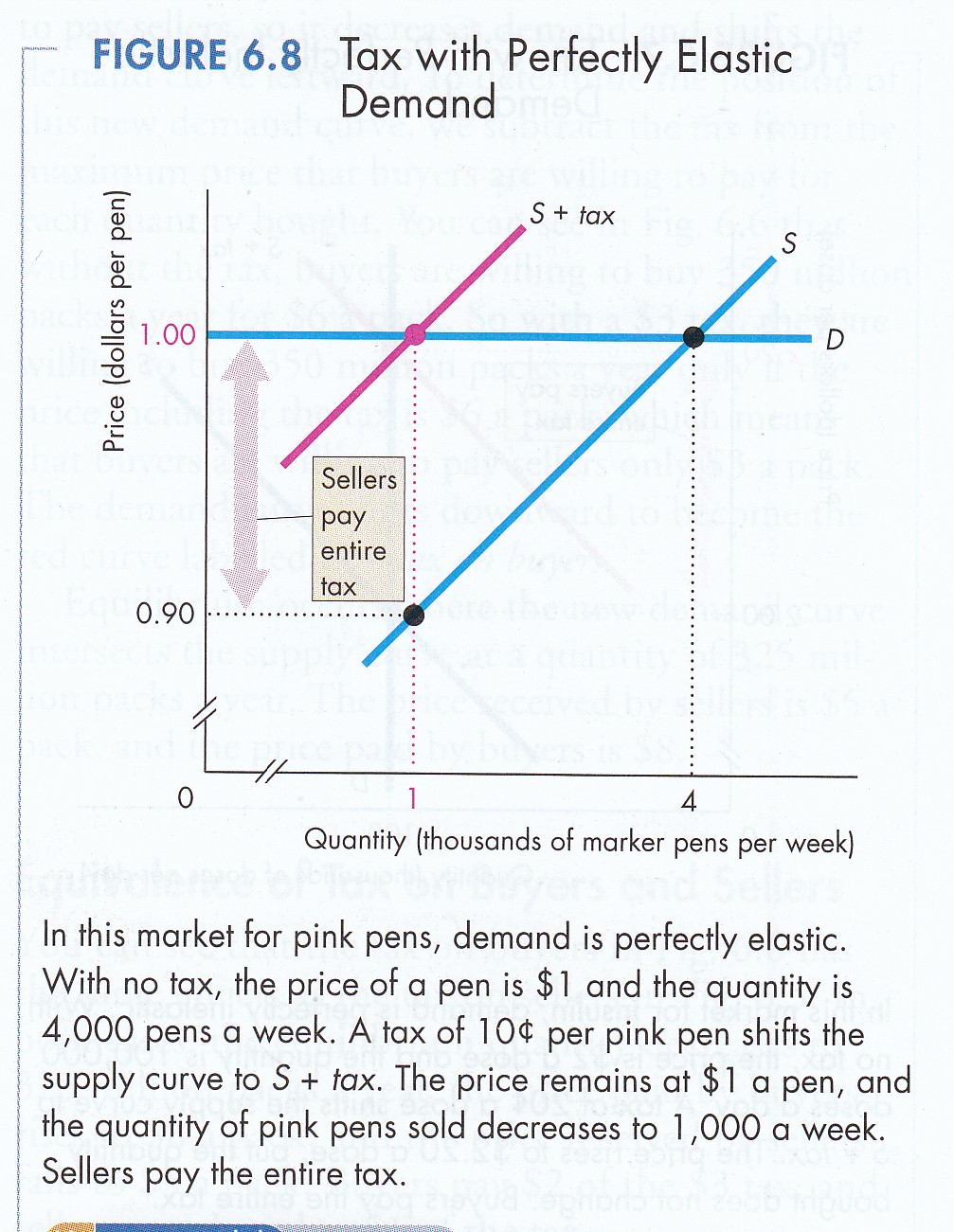

In this case the consumer pays the full tax. If, on the other

hand, demand is perfectly elastic ((P&B 4th Ed.

Fig. 7.7b;

5th Ed. Fig. 6.7;

7th Ed Fig. 6.8;

R&L 13th Ed Fig.

4-8

&

4-9),

then the producer pays the whole tax.

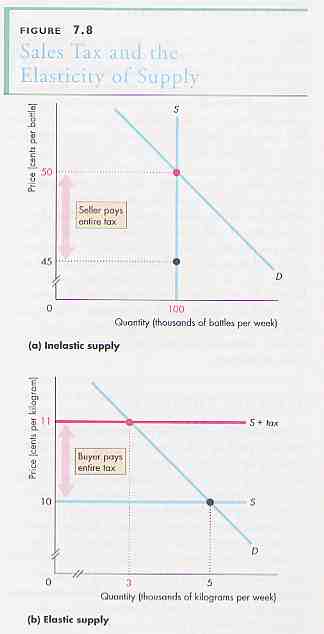

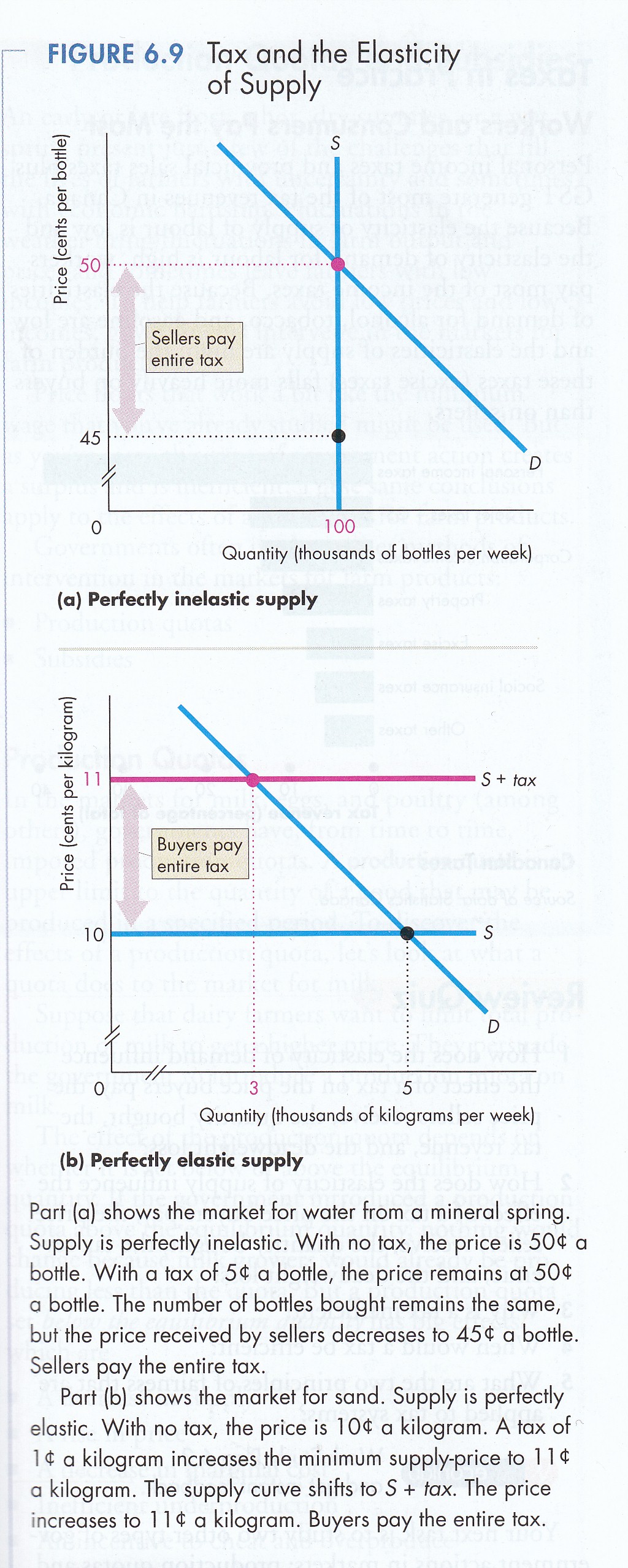

In the case of supply elasticity, the

situation is reversed (P&B 4th Ed.

Fig. 7.8;

5th Ed. Fig. 6.8;

7th Ed Fig. 6.9).

If supply is totally inelastic, that is the supply curve is

vertical, then the supplier bares the full tax. If supply is

perfectly elastic, however, the consumer will pay the tax

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}