2.0

Introduction

This section is arguably the core of the course. In it the Standard

Model of Market Economics is established. This model describes

manufacturing or secondary industries. Ten primary economic

concepts used or implied throughout the required text are defined.

It is from variations from perfectly competitive norms of the

Standard Model that the impact of environmental costs and benefits

external to market price are assessed for both public and private

goods.

Public policy efforts to abate problems like pollution are intended

to establish the price/quantity relationship that should exist under

such normative conditions. The critical role of Law particularly

property rights in correcting environmental problems is also

examined including the so-called ‘Tragedy of the Commons’ – both

natural and artificial. Consideration is also given to the role of cost-benefit

analysis, present value and the precautionary principle in

determining appropriate public intervention in the marketplace for

both private and public goods .

2.12.1 Analytic Engine: 'X' Marks

the Spot

For nearly half a century the world lived with a 15 minute warning

threatening all of humanity with nuclear winter because of a

domestic dispute in economics. One branch broke off to form the First World of democratic market economies while the

second

coalesced into the Second World of communist command economies. The

dispute centred on the question of private versus public

property.

Origins

Unlike

Marxism

with its bible,

Das Kapital, the ideology of the market developed in two

historically disconnected stages, the first in the late 1770s and

the second in the 1870s. The first coincided with the Republican

Revolution. The American started in 1776, the same year Adam Smith

published his Wealth of Nations, generally considered the

beginning of modern economic thought. This was followed by the

French in 1789 and the Bolivarian Revolution in Latin America that

continued into the 1820s followed by the Chinese Republican

Revolution of 1910. These revolutions replaced an Ancient Regime of

subordination by birth by one in which each adult Natural Person

mark their ballot with an ‘X’ thereby determining their government –

popular democracy.

These revolutions gave birth to two critical political economic

ideas - laissez faire and laissez passer. The first–

laissez faire – means let private persons, not a monarch,

decide what to produce and how. Until this time the Sovereign made

grants of industrial privilege, i.e., economic monopolies –

foreign and domestic - to friends and supporters. In Britain, the

granting of domestic monopolies ended with the Statute of

Monopolies in 1624. Foreign trade monopolies, however, such as

the 1670 royal charter to the Company of Adventurers of the Hudson

Bay, continued to be arbitrarily granted for more than two

centuries.

The second term – laissez passer – means let workers move to

the work. Thus until 1814 when the British House of Commons

abrogated the Statute of Artificers (in force since the time

of Elizabeth I) workers were restricted to working in their place of

birth. Guilds controlled entry into and managed the trades

restricting members to their own city, town or region. In fact the

guilds provided popular education until displaced by compulsory mass

education in the late 1860s.

At the age of seven a young lad or lass would be apprenticed

(effectively sold) to a Master who would then employ them for seven

years generally as a gopher. If satisfied the Master might then

extend the apprenticeship for another seven years at which time the

apprentice might earn journeyman’s papers and eventually become a

Master in turn, It should be noted that the original duration of

patents of invention and copyrights was 14 years – the term of two

apprenticeships.

The second stage in the development of market ideology occurred in

the 1870s with the

Marginalist Revolution.

The decade began dramatically enough with the fall of Napoleon III

before an ascendant Prussia which shortly unified many Germanys into

one – the Second Reich. Napoleon III was replaced by the Third

French Republic reinvigorating republican ideology on the Continent

and beyond. Yet the fall of the last Bonaparte also marked by the

rise of the first Communist State – the Paris Commune of 1871.

Marxism too was ascending.

Since before the time of Adam Smith economics had concerned itself

primarily with the growth and distribution of national wealth among

factors of production – land (natural resources in general) that

collected rent, labour that collected wages and capital that

collected interest or profits. It was Adam Smith and his

successors from Ricardo to John Stuart Mill (On Liberty and The

Subjugation of Women ) who make up the Classical School of

economics. Its vocabulary was of aggregates and of classes. In

this sense Marx was a ‘classical’ economist. It is ironic that

Marx himself named all those who came before him as the

‘Classical School’. It should also be recalled that Marx claimed

his theory rested on proofs derived from the science of political

economy.

The Marginalist Revolution changed the vocabulary. It split

political economics into Market and Marxist economics. In a very

real sense it allowed Market Economics to catch up with the politics

of the Republican Revolution. It shifted focus from class to the

individual ‘atomized’ consumer and producer. It shifted attention

from economic growth and distribution of national wealth to

allocative efficiency in consumption and production.

This was made possible by the marriage of Newton’s calculus of

motion and

Jeremy Bentham’s calculus of

human happiness or

felicitous calculus. The result was a model and a method that

satisfied the requirements of a true science according to Rene

Descartes, one of the 17th century founders of the Scientific

Revolution. It is based on a set of simple assumptions from which

mathematically provable and geometrically demonstrable deductions

may be drawn. Thus Thomas Kuhn in his seminal work The

Structures of Scientific Revolutions places economics as the

closest of the social sciences to ‘normal science’.

Bentham

is arguably the most

important public policy figure in Anglosphere history. His

influence is still felt in criminal justice, education and public

assistance systems throughout the English-speaking world. He is

also considered the successor of Adam Smith even though a lawyer,

not an economist. Like his contemporaries Bentham longed to find

the social equivalent to Newton’s physical laws and calculus of

motion. He found an answer, however, not in Aristotle or Plato like

most social theorists of his day but in the ideas of their ancient

Greek contemporary, Epicurus. Epicurus, however, was an atheist

unlike Aristotle and Plato both of whom objected to the Epicurean

pleasure ideal as did the Christian church

Bentham’s epistemology is based on the atomic materialism of

Epicurus (341-271 B.C.E.). He acquired it from the De Rerum

Natura (On the Nature of Things) written by the Roman

Epicurean poet Lucretius (99-55 B.C.E.), whose work, unlike that of

Epicurus himself, survived the fall of the Roman Empire and the

censorial fires of the Church.

Like Epicurus, Bentham believed that physical sensation was the

foundation of all knowledge. Knowledge, including preconceptions

such as ‘body,’ ‘person,’ ‘usefulness,’ and ‘truth’, form in the

material brain as the result of repeated sense-experience of similar

objects. Ideas are formed by analogy between or compounding such

basic concepts. For Bentham such sense experiences involved a unit

measure of pleasure and pain called the ‘utile’ from which Bentham’s

brand of Utilitarianism - Ethical Hedonism - emerged. Utiles would,

according to Bentham, eventually be subject to physical measurement

and he proposed a formal ‘felicitous calculus’ of human happiness.

The expression “the greatest good for the greatest number” reflects

this vision. His materialism matches the definition of an ideology

as secular theology – an explanation of how the world works without

reference to a divinity.

For my purposes, three assumptions of this calculus are relevant.

First it is assumed consumers and producers have perfect knowledge.

This has profound implications for any knowledge-based economy which

I will not explore at this time. Second, it is assumed human beings

practice calculatory rationalism, i.e., they are

constantly calculating and weighing the relative probability and

magnitude of present and future pleasure against present and future

pain. Third, while utiles cannot be physically measured it is

assumed they can be reified, i.e., an abstraction made

concrete, in this case of happiness made money. The presence of

money brings pleasure; its absence pain. The willingness to pay in

monetary terms is taken as the measure of the happiness a consumer

believes a good or service will deliver. It is ironic that the

standard model of market economics achieves what Plato, speaking of

Art, feared most in politics, that: “not law and the reason of

mankind, which by common consent have ever been deemed best, but

pleasure and pain will be the rulers in our State”. To quote

Bentham, however:

Nature has placed

mankind under the governance of two sovereign masters, pain and

pleasure. It is for them alone to point out what we ought to do, as

well as to determine what we shall do. On the one hand the standard

of right and wrong, on the other the chain of causes and effects,

are fastened to their throne.

In the hands of Francis Ysidro

Edgeworth

(1845-1926) Bentham’s felicitous calculus of human happiness was

successfully married to Newtonian calculus of motion and reduced to

geometric expression subject to mathematical proof in his 1881

Mathematical Psychics. His geometry and its related calculus

permitted erection of what became the standard model of market

economics – first in consumption and then in production theory.

The conceptual key is the term ‘marginal’, hence the name of the

revolution. In effect what in Newtonian calculus of motion is a

derivative – first order, the rate of change; second order, the rate

of change of the rate of change – defines decision-making at the

margin in economics. Hence ‘marginal utility’ is the additional

satisfaction of an added unit in consumption while ‘marginal

product’ is the additional output of an added unit input in

production. The outcomes of such actions can be demonstrated in

mathematics, geometry and words – the three languages of economics.

There is, however, also great disquiet around the world about an

ideology that reduces human choice to atomistic calculation of

profit and loss, not just in the marketplace, but in all human

activities ranging from marriage and child rearing to art, education

and culture. It is, as we will see, an ideology framed by the ‘X’

of intersecting market supply and demand curves marking the spot

where maximum human happiness and private profit is to be found.

Before the Republican Revolution, the economy was embedded in

society through guilds and a class structure of subordination by

birth. Today, some fear that human society itself is being embedded

into a global economy in which everything is for sale – hearts,

kidneys, lungs as well as the entire natural and human built

environment – much as Karl Polanyi suggested in his 1944 The

Great Transformation: The Political and Economic Origins of Our Time.

Such lingering concerns may be the genetic fragments of a not quite

dead Marxism or remembrances of forgotten republican roots –

equality, fraternity and liberty. In a way, the Republican

Revolution sought political freedom for the individual and in the

process spawned the free self-regulating market as its economic

corollary. The Communist Revolution, on the other hand, sought

economic freedom for the individual (each according to one’s need)

through a centrally controlled command economy and spawned the

one-party Leninist state as its political corollary. Arguably both

freedoms – political and economic - are required to realize full

human potential.

It was not, and is not, however, just the far Left that has concerns

about Bentham’s felicitous calculus and the standard model of market

economics. Joseph

Schumpeter of ‘creative

destruction’ fame called it “the shallowest of all conceivable

philosophies of life that stands indeed in a position of

irreconcilable antagonism to the rest of them”. John Maynard Keynes

went further identifying its dangerous ideological flaws:

I do now regard that as the worm which has been gnawing at the

insides of modern civilization and is responsible for its present

moral decay. We used to regard the Christians as the enemy, because

they appeared as the representatives of tradition, convention and

hocus-pocus. In truth, it was the Benthamite calculus, based on an

over-valuation of the economic criterion, which was destroying the

quality of the popular Ideal. Moreover, it was this escape from

Bentham… which has served to protect the whole lot of us from the

final reductio ad absurdum of Benthamism known as Marxism.

In fact, each generation of economist since his time has tried to

escape Bentham’s thrall. Nonetheless, Benthamite felicitous

calculus survives. Like a vampire it won’t die! There are at least

four reasons.

First, it is elegant - meaning simple and effective.

Second, it is flexible. Even altruism can be accommodated. How

much money you are willing to give to the Save the Whatever Fund is

the measure of utiles you get in return. There are no selfless

deeds.

Third, it is, in a sense, politically correct. Concepts like

consumer sovereignty and dollar democracy resonate with

our political roots. And economic growth defined as more money in

one’s pocket is a unifying principle in a multicultural world where

most people do not agree about many things, e.g., language

and religion.

Fourth, it is exportable. As we will see the concept of constrained

maximization has been transported into Law, Sociology, Social Work

and many other disciplines and practices.

The ‘X’

Economics, among other things, is about choice. More specifically

microeconomics is about the constrained maximization of consumer

happiness and producer profit in a marketplace where goods &

services can be freely bought and sold, in other words, where Supply

meets Demand.

Demand – Consumer Theory

On

the one hand, the consumer strives to maximize happiness through the

consumption of goods & services. On the other, the consumer is

subject to a

budget constraint. If there were no constraint then

the consumer could ascend to one’s bliss point, a technical

term in welfare economics corresponding to metaphysical concepts

such as satori in Zen or epiphany in Christianity.

In

symbolic logic, and restricted to a two-commodity economy, this

process begins with the consumer maximizing:

U = f (X, Y) where:

‘U’ stands for consumer happiness defined as utility measured as

the sum total of all pleasure ‘utiles’ acquired;

‘f’ stands for some function reflecting the taste of the

consumer; and,

‘X’ & ‘Y’ stand for goods and services

The consumer, however, is subject to a

budget constraint,

expressed as:

I = PXX + PYY where:

‘I’ stands for income earned through work considered ‘disutility’

or pain;

‘P’ stands for price; and,

‘I’ must be exhausted on some combination of X & Y, i.e.,

happiness is obtained only through the consumption of goods &

services that have associated monetary prices.

Assuming that the

price of only one commodity changes

while all other variables remain fixed or ceteris paribus,

i.e., the price of other goods, income and consumer taste remain

the same, we can derive the

consumer demand curve

for a product.

The demand curve shows how much a consumer is willing to pay

for a given quantity to maximize happiness subject to the budget

constraint. It will usually be downward sloping reflecting the Law

of Demand: the lower the price, the greater the demand; the higher

the price, the lower the demand. By horizontally summing up how

much each consumer is willing to buy at each specific price we

generate the market demand curve.

Supply –

Producer Theory

On

the other side of the economic equation, the producer or firm wants

to maximize output.

The

production function

of a firm in symbolic logic is expressed as:

Q = g (K, L, N) where:

‘Q’ stands for output;

‘g’ stands for some function reflecting the technology or

‘know-how’ available to combine factors of production (K, L, N) to

produce ‘Q’’;

‘K’ stands for capital as physical plant and equipment, the value

of which can be expressed in financial terms;

‘L’ stands for labour including productive (shop floor), managerial

and entrepreneurial talent; and,

‘N’ stands for natural resources that can be enframed and enabled

to serve human purpose.

If

the firm cannot increase Q without increasing inputs, i.e.,

K, L and/or N, it is ‘technically efficient’. The producer,

however, is subject to a cost constraint which, assuming a

two-factor economy, is expressed as:

C = PKK + PLL where:

‘C’ stands for cost;

‘P’ stands for price;

‘K’ stands for quantity of capital; and,

‘L’ stands for quantity of labour.

Thus for a

given ‘Q’ there is an associated ‘C’ determined by the sum of the

quantity times the price of each factor employed. How much Q will

actually be produced is dependent, however, on

market price,

i.e., how much consumers are willing to pay for a given

quantity. So long as that price maximizes profit (or minimizes loss

at or above the firm’s ‘shutdown’ point) it will provide a

corresponding Q.

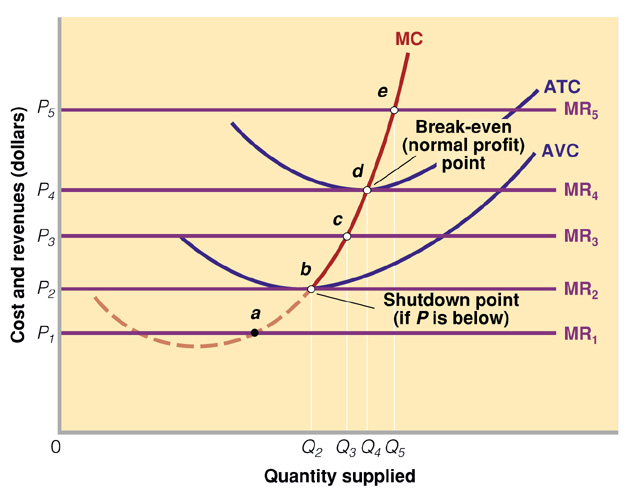

From the resulting cost function we can determine

the supply curve of the firm,

i.e., how much it is willing to produce at each

price. The supply curve is the marginal cost curve of the firm

above the shut-down point. If the firm cannot earn enough to cover

all its variable costs, it shuts down. The curve will in the

short-run be upward sloping reflecting the Law of Supply: the higher

the price, the greater the supply; the lower the price the smaller

the supply. By horizontally summing up how much each firm is

willing to provide at each price above its shut-down point we

generate the market supply curve.

Market Theory

Markets are any arrangement that

enables buyers and sellers or consumers and producers to get

information and do business with each other. Put another way,

markets are where demand meets supply. Markets can be described by

reference to whether they are:

- geographic or commodity-based;

- in or out of equilibrium;

- sensitive to change in prices and

incomes (elasticity); or,

- influenced by any individual or group

- consumer, producer or government.

With Market Demand and Supply Curves we

generate an ‘X’-shaped

graph with Demand increasing as price

goes down and Supply increasing as price goes up. The point where

they intersect is called market equilibrium, the point at which the

willingness to buy and the willingness to sell are

equal. Ceteris paribus, this will be a stable equilibrium,

i.e., if all variables remain fixed, e.g., technology,

factor prices, consumer taste, income and the price of all other

goods & services, the price-quantity equilibrium will be maintained.

Under such fixed conditions if the price rises above equilibrium,

for whatever reason, firms will be willing to provide more than

consumers are willing to buy. A surplus is created. To eliminate

the surplus firms lower price returning eventually to equilibrium.

Similarly, if price drops below equilibrium demand exceeds supply

and a shortage results. Consumers will then bid up the price until

it returns to equilibrium. These constitute so-called ‘market

forces’.

Choice in microeconomics, however, is made ‘at the margin’. In the

case of the consumer, consumption of ‘X’ will increase until, dollar

for dollar, the additional satisfaction (marginal utility or MU)

from the last unit consumed equals the satisfaction, dollar for

dollar, of the next unit of good ‘Y’. In symbolic logic this is

expressed as:

MUx/Px = MUy/Py where:

‘MU’ stands for the additional or marginal utility to the consumer

from the next unit consumed; and,

‘P’ stands for the price.

Similarly, the firm will increase output until the additional or

marginal cost of the last unit produced equals the additional or

marginal revenue earned from its sale. All previous units cost less

than revenue earned and profit is maximized when, in symbolic logic:

MC = MR where:

‘MC’ stands for marginal cost

‘MR’ stands for marginal revenue

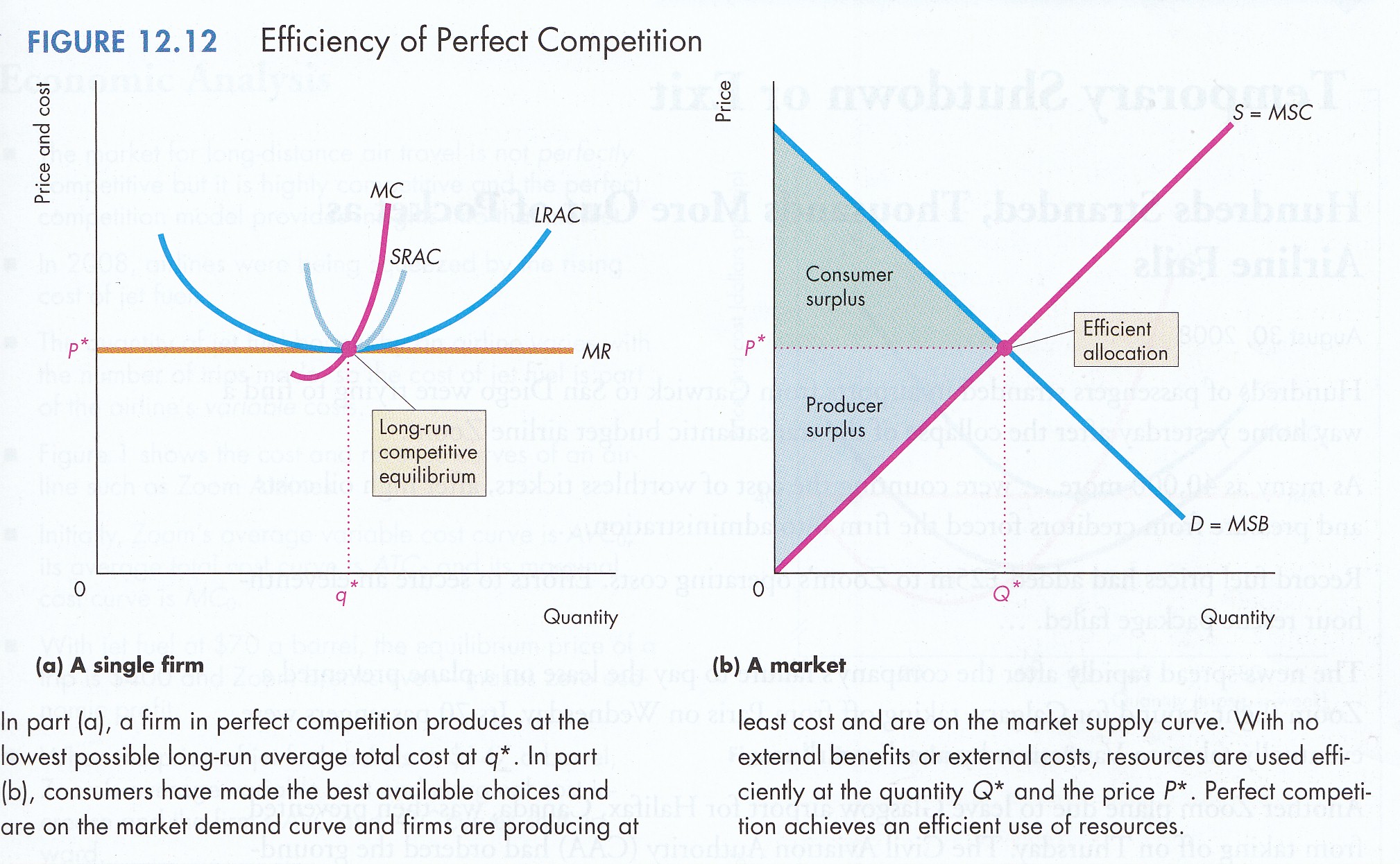

The actual market equilibrium – price/quantity – will depend on the

nature of the market. If there are many, many sellers of identical

goods and many, many buyers there is ‘perfect

competition’

and ‘X’ marks the spot. If not, the outcome reflects the exercise

of market power by either consumers or producers.

This constitutes the standard model of market economics developed

during the last quarter of the 19th and first quarter of the 20th

centuries especially in the hands of

Alfred Marshall

(1842-1924)

of Cambridge University. It is alternatively known as the

Marshallian, Neoclassical or Perfect Competition model

While Marshall contributed its iconic centerpiece - the ‘X’ - which

is often called the ‘Marshallian scissors’, Marshall himself held a

much more subtle, complex and biological view of the economy. As

with the work of many great economists, however, including Adam

Smith, some of Marshall’s work became part of the canon while other

parts were simply forgotten. One thing should not be forgotten:

one of Marshall’s Cambridge students went on to create the

standard model of macroeconomics and arguably the current world

economic order –

John Maynard

Keynes.

The Nine E’s of Economics

Coincidentally, perhaps, economics engages a number of concepts

beginning with the letter ‘e’. I now consider seven and connect

them to the ‘X’.

I - Efficiency

Efficiency plays many roles in economics. Consider. First,

allocative efficiency implies that all factors in production and all

commodities in consumption are in their best use and receive their

opportunity cost.

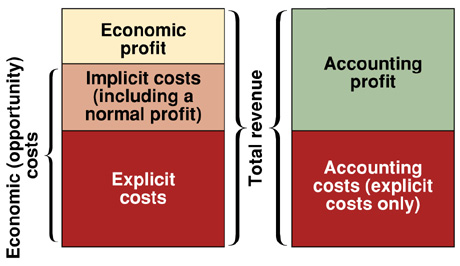

Economic choice involves how to satisfy infinite human wants, needs

and desires subject to scarce resources. It requires a choice

between alternatives, e.g., a pensioner choosing food or

medicine. The choice of the best alternative, however, implies that

the next best alternative is not chosen. Put another way, the cost

of choosing one possibility is the next best alternative foregone.

This is called 'opportunity cost'. All economic costs are

opportunity costs even those not expressed by market prices. This

distinguishes economic from accounting or business cost.

For allocative efficiency to exist three conditions must hold:

(i)

Consumer Efficiency: when consumers cannot increase utility

by reallocating their budgets;

(ii)

Producer Efficiency: when firm cannot reduce cost by shifting

the input mix;

(iii)

Exchange Efficiency: when all gains from trade have been

exhausted. Gains to consumer is called

consumer surplus

which measures the difference between what consumers are willing to

pay and what they actually pay for a given quantity of a good or

service. Gains to producers are called

producer surplus

which measures the difference between what they are willing to

accept and what they actually receive for a given quantity of a good

or service.

Second, in production efficiency refers to the ratio of outputs to

inputs. To measure efficiency one must therefore be able to

calculate both inputs and outputs. This is most easily done in the

production of goods rather than services, especially in

manufacturing, e.g. cars produced per worker.

Technical efficiency is achieved when it is not possible to increase

output without increasing inputs. Economic efficiency occurs when

the cost of production for a given output is as low as possible. A

secondary consideration is that such output is sold at a price

sufficient to compensate all factors of production at their

opportunity cost, i.e., no excess or economic profit or rent

is earned. Thus all economically efficient solutions are

technically efficient but not all technically efficient solutions

are economically efficient, that is, something may be technically

efficient but uneconomic. It cannot pay its own way, e.g.,

space exploration and the military.

It is also important to distinguish between technical and functional

obsolescence. Equipment becomes technically obsolete when newer

equipment can do the job more efficiently, e.g. the Pentium

CPU made the 486 and 386 technically obsolete but they can still do

the job for which they were intended. Functional obsolescence

occurs when old equipment cannot do the job.

II - Effectiveness

In some goods and most services especially those produced by

government, neither inputs nor outputs can be readily calculated and

hence efficiency cannot be determined. Accordingly, a less stringent

test - cost effectiveness - is applied. Surrogates or proxy

indicators of inputs and outputs are used. For example, the

“recidivism rate” per parole officer (percentage of repeat

offenders) can be used as an imperfect proxy for output rather than

the more difficult to measure concept of “rehabilitation” measured

in human, social, and/or economic terms. Similarly, average salary

per parole officer can be used as a crude surrogate for inputs

rather than the more difficult to measure opportunity cost of

relevant financial, human, information, and physical resources in

alternative applications, e.g., early education rather than

later incarceration.

III - Elasticity

Elasticity refers to the sensitivity of one variable to a one

percentage change in another. Economic theory recognizes three

principal types:

i -

income elasticity of demand

- with all prices constant refers to the percentage change in the

quantity of a commodity demanded compared to a one percent change in

income;

ii - price elasticity of

demand

or

supply

- refers to the percentage change in the quantity of a commodity

demanded or supplied compared to a one percentage change in its

price. The amount demanded or supplied can increase:

a) more than proportionately, i.e. elasticity is greater than

one - at the extreme a horizontal demand or supply curve is

perfectly elastic - a small increase in price results in a large

change in the quantity demanded or supplied;

b) proportionately, i.e. elasticity is equal to one (unitary

elasticity); or,

c) less than proportionately. i.e. elasticity is less than

one (inelastic) - at the extreme, a vertical demand or supply curve

is perfectly inelastic - any change in price results in no change in

the amount of the commodity demanded or supplied; and,

ii - elasticity of substitution or

cross-elasticity

in production refers to the percentage change in the amount of an

input substituted for another in response to a change in their

relative prices. Similarly, the cross-elasticity in consumption of

one commodity substituted for another by a consumer in response to a

change in their relative prices can be calculated.

IV - Employment

While popular discussion focuses on employment with respect to

labour in fact all factors of production are subject to employment,

underemployment and unemployment. In manufacturing the concept of

capacity utilization captures employment of physical plant

and equipment, i.e., what percentage of potential output –

24/7 - is actually produced. Similarly ‘undeveloped’ refers to

natural resources not yet employed in the production process.

In the case of labour there is the concept of the labour force

defined as all persons aged between 15 and 65. Then there is the

related concept of the participation rate, i.e., what

percentage of the labour force has or is actively seeking

employment. There is season unemployment, e.g., in the ski

industry; cyclical unemployment which follows the business cycle;

and, structural unemployment often reflecting the effects of

technological change such as afflicted the Maritime provinces of

Canada with the shift from sail to steam powered vessels late in the

19th century.

There is also the concept of the ‘natural rate’ of unemployment

which varies between countries due to structural and policy factors

such as the generosity of unemployment insurance programs. Thus

traditionally the

Canadian

natural rate of unemployment has been higher than the

U.S.A.

V - Equilibrium

Equilibrium is a condition which once achieved will continue

indefinitely

unless one of the variables is altered. In the case of markets, the

equilibrium price 'clears' the market, that is the quantity

demanded by consumers equals the quantity supplied by producers.

More generally, economic theory recognizes four types of

equilibrium:

i - general equilibrium: which refers to a condition when the entire

economy is under perfect competition. It is a static state where

all prices are at their long run equilibrium, individuals are

spending income to yield maximum satisfaction, and the demand and

supply factors of production are equated throughout the economy;

ii - stable equilibrium: which refers to a condition which once

achieved continues indefinitely unless there is a change in some

underlying conditions. Changes in economic conditions will be

followed by reestablishment of the original equilibrium. Example: a

ball resting at the bottom of a cup; shake it and the ball moves;

stop shaking and it returns to the bottom of the cup; and,

iii - unstable equilibrium: which refers to a condition which once

achieved will continue indefinitely unless one of the variables

changes and then the system will not return to the original

equilibrium. Example: a ball resting on the top of an overturned cup

- shake it and the ball falls off never to return to the same place;

and,

iv - multiple equilibria: which refers to the condition in which

more than one equilibrium exists. This is particularly true in

developmental economics where a developing country may find itself

in a stable equilibrium but one that is not optimal for its economic

growth and development. The unaided market cannot move the economy

to the preferred outcome.

VI - Equity

The economic concept of equity evolved out of English legal

history. At the same time that the Common Law began another unique

Anglosphere legal institution emerged – Equity. With the Norman

Conquest of 1066 all rights and privileges of the previous regime

were abrogated by right of conquest. In effect William the Conqueror

had carte blanche to shape a kingdom without accounting for

pre-existing feudal rights and obligations. Unlike other European

kingdoms, it was his exclusive unqualified and personal domain. He

was absolute Sovereign. Nonetheless, what he conquered was a

patchwork of Angle, Saxon, Jute, Danish, Viking and Celtic

settlements, regions, laws and languages. The new King divided up

his new Property, after accepting fealty, to a new Anglo-Norman

aristocracy. The new local rulers, while subject to the King, also,

in effect, inherited rights and privileges acceded to traditional

rulers under local legal systems. Some were honoured and survived to

become incorporated into Common Law.

William’s new subjects, however, soon brought to his attention (and

that of his successors) inequities in a supposedly unified kingdom.

At the extreme, in one jurisdiction theft of a loaf of bread cost a

hand; in another, two days in the stocks hit by rotten vegetable and

insults thrown by one’s neighbours. It was not guilt or innocence

they cried but fairness of punishment before the King. This is

arguably the root of Equity – a separate and distinct strand of

jurisprudence parallel to the Common Law of precedent.

Over time responsibility for hearing calls for mercy was transferred

to the King’s Lord Chancellor and a court of his own – the Court of

Equity also known as the Court of Conscience or of Morality. In fact

until Sir Thomas More (a lawyer) became Chancellor in 1529, all had

been men of the cloth. Two aspects of Equity played a critical role

in the Sovereign’s ability to control his vassals. These were trusts

and tenant-landlord disputes. Trusts (from which modern charities

and financial trusts evolved) generally concerned widows and orphans

left to the mercy of a local lord. The most famous is Lady Marion of

the Robin Hood legend who was an orphan and ward of the King. With

respect to tenant-landlord disputes, Equity balanced the feudal

local lords by judiciously connecting the King to his subjects. This

was called the ‘rent bargain’ by

John R.

Commons.

It stabilized the social system of post-Conquest England.

While Magna Carta (1215) and subsequent developments

increasingly limited the King, Equity and Common Law continued to

develop as parallel systems of courts with precedence given to

Equity. It was not until 1873 in the United Kingdom that the two

systems of courts merged. Nonetheless the two strands of Anglosphere

jurisprudence continue to this day in all Common Law countries with

Equity retaining precedence.

The economic concept of Equity arguably derives from legal Equity.

In fact the Chancellor of the Exchequer (who in Canada we call 'the

Minister of Finance') exercised a concurrent jurisdiction in Equity

with the Lord Chancellor’s Court. There are two economic definitions

of Equity, each reflecting its historical roots.

First, there is Equity as the capital of a firm which, after

deducting liabilities to outsiders, belongs to the shareholders.

Hence shares in a limited liability corporation are also known as

equities. This links back to the historical treatment of trusts

under Equity.

Second, there is Equity as ‘fairness’. While often used with

reference to taxation it is a general economic concept. With respect

to taxation Equity has three dimensions: horizontal, vertical and

overall burden. Horizontal Equity refers to ‘like treatment of

like’. Vertical Equity refers to ‘unlike treatment of unlike’.

Overall Equity refers to the accumulated impact of all forms of

taxation. Crudely, it is the difference between earned and

disposable income after all taxes – income, excise, sales, et al.

Equity is also applied in a number of market interventions by

government, e.g., minimum wage and rent control. Examples of

government intervention for reasons of equity will be discussed in

the next lecture in this series.

VII - Excludability

Excludability and rivalrousness are characteristics of a private

good. If I buy a car I can exclude others from using it by lock and

key. I alone extract its utility. Similarly, if I am driving no

one else can, i.e., driving is rivalrous in

consumption/production.

On the other hand, public goods are non-rivalrous in consumption,

i.e. my consumption does not reduce the amount available to

you. If I watch a fireworks display it does not reduce the amount

available to you. Similarly, public goods are non-excludable,

i.e. a user cannot be easily prevented from consuming a public

good. This creates the ‘free-rider’ problem. Extending the

fireworks example, while I may not be willing to pay to enter the

stadium but I can still watch the display from the balcony of my

apartment at no charge.

Allowing for externalities (discussed below) there is in fact a

spectrum of goods ranging from pure private to pure public in

nature.

VIII - Expectations

Time plays a critical role in economic analysis. In fact there are

two distinct forms of analysis based on time: static and dynamic.

Static analysis involves an economic variable or phenomena in a

specific fixed moment in time. Dynamic analysis involves analysis

through time, that is from the past to the present, or from the

present into the future.

Three great economists enhanced our economic understanding of Time.

John Maynard Keynes introduced the concept of 'expectations'. Over

time people's changing expectations of what tomorrow will bring

causes their actions to change today.

Friedrich August von

Hayek

stressed ‘foresight’. Similarly,

John R. Commons introduced the

concept of 'futurity' meaning people live in the future but act in

the present. The difference between what we plan to do tomorrow and

what we actually do today in expectation of tomorrow introduces a

constantly changing dynamic to economic analysis, especially

macroeconomic analysis. For example, if we expect interest rates

will fall tomorrow, we hold off borrowing money today. But when

tomorrow comes and interest rates do not fall our plans must be

changed.

IX - Externalities

See

2.2 Externalities below.

The Big‘O’ in

Economics – Opportunity Cost

The choice of the best alternative implies that the next best

alternative is not chosen. Put another way, the cost of choosing

one alternative possibility is the next best alternative foregone.

This is called 'opportunity cost'. All economic costs are

opportunity costs serving to

distinguish economics from accounting or business costs.

And with respect to the economics of the environment this is a

critical difference. As noted in the title of this site: Elemental

Economics – Not Accounting, Not Business, Not Commerce, Not

Mathematics - Economics!

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}